The US Federal Reserve today announced they were going to raise the short term interest rate 0.5% and start their QT program on June 1st.

Because this was less drastic than the market was expecting, everything is rallying today because of continued easy monetary conditions, which will surely not help inflation expectations any.

My curiosity concerns the quantitative tightening, which proposes a $30 billion per month tapering starting June 1st, and then going to $60 billion per month on September 1st. This is on the treasury bond side, the mortgage backed security side has a different bucket of money to work with, but I will ignore mortgage backed securities in this post and just focus on treasury securities held by the federal reserve.

We look at what happened in 2017-2019 when the last attempt to do this occurred:

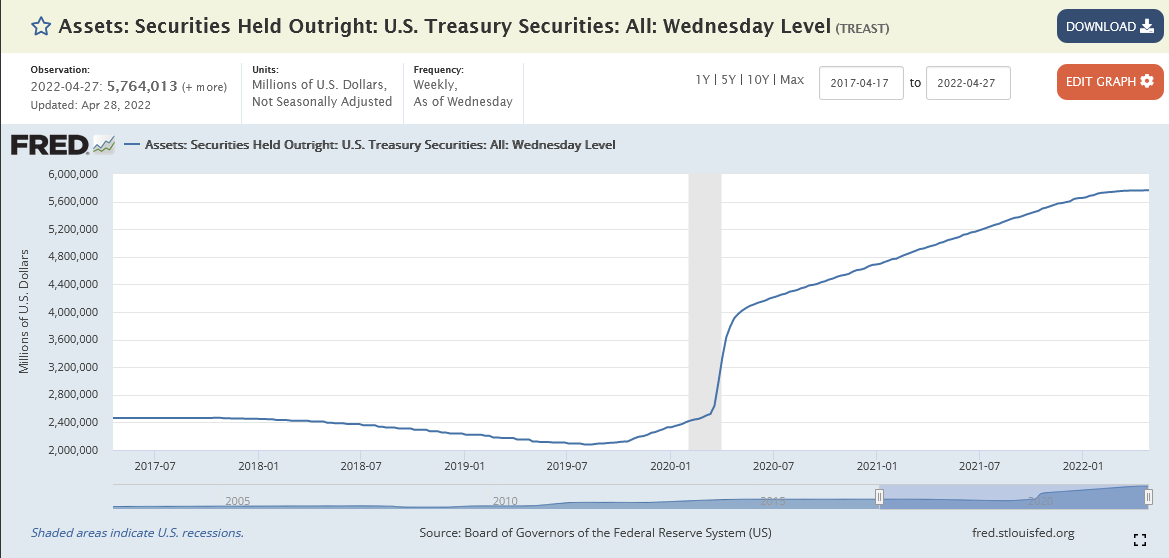

On January 3, 2018, the fed had $2.448 trillion in treasuries on the balance sheet. On January 2, 2019 they had $2.223 trillion, a taper rate of $18.75 billion per month.

The fed ended up crashing the stock market on the fourth quarter of 2018. It was a classic liquidity bust.

This upcoming taper will be faster ($30 billion a month), but it also comes from a much larger asset pool ($5.763 trillion). The taper doubles in September if they do not change things.

Compounding the problem is inflation. Back in 2018 the headline inflation was still very muted – talks of deflation were quite omnipresent. This time around, inflation is very much on the radar of everybody.

The federal reserve meets again on June 15 and July 27, where they have all but signaled rate increases (likely 50bps per meeting). This will still render the fed funds rate at a target of 1.75-2.00%, which by all historical standards is quite low, and especially considering the CPI at around 7%, still deeply negative.

My guess at present is that we are going to get a gigantic market rally in the next few months, especially in the stocks that have been taken out and shot over the past six months (looking at technology and software stocks in particular).

Shopify fans, you probably will be able to get some temporary revenge.

However, the will be temporary. While the rally in prices will be impressive, I do not think they will be sustained after the summer.

I am not a good enough trader to try this, but if I were to take a guess at where the speculative winds are blowing, I would long ARKK-type stocks for a couple months and then get rid of them sometime in August.