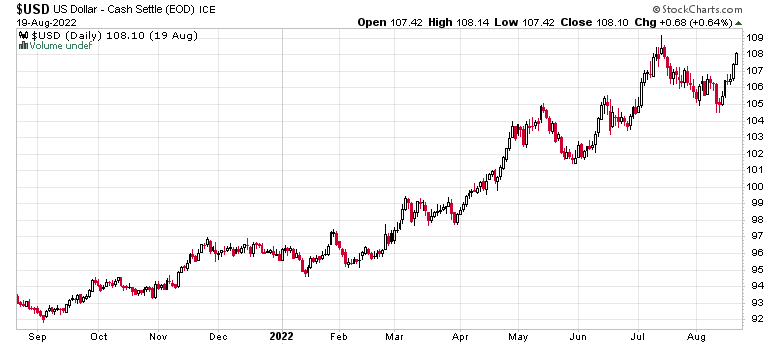

By far and away, the largest surprise for many has been the relative strength of the US currency to the exclusion of others:

Since most international trade is denominated in US currency, it means that for foreign countries engaging in commodity purchases and most other imports, the trade currency becomes that much more expensive to transact. This has an effect on their cost inputs (in addition to the core commodity prices themselves being relatively inflated). For example, when Europe wants to import LNG, not only do they have to pay an extremely bloated premium to doing so, but right now they are dealing with record lows of “99 Euro-pennies” being equal to one US dollar.

The US Federal Reserve as well is raising interest rates, so holding cash (or liquid short-term treasury notes) is no longer a zero-yield option: indeed, you can lend your money to the US government for a year and get 3.3% for it. Cash is once again becoming more valuable.

It was widely anticipated that with inflation and the US government printing massive deficits that the currency would sink like a stone – indeed, it has gone in the opposite direction as people are demanding US dollars, especially as asset markets depreciate, and credit stress becomes apparent.

The future course of action appears to be that there will be some sort of crescendo event where the US dollar will gain so much strength and then when things break somewhere, the US dollar will be sold off. I don’t know when this will be.

All I know is that being levered long in this environment is dangerous – especially as the existing consensus is that the fed will drop interest rates again in 2023 – what if they don’t because inflation is still running well above 2%?

Prices are formed on the basis of the sentiments of the marginal bidder and marginal seller. In the event that there is an instantaneous drop in demand and consistent supply, prices will drop and they will drop quickly. As interest rates rise and central banks continue to pull capital out of the bond markets, it is like taking oxygen out of the room. Initially, nobody notices. Then there is a point where people actually feel better, despite the fact that the oxygen level gets below where it can sustainably maintain your cognitive function. We’re probably at that point in the markets. Then finally, you start to lose your functionality entirely before losing consciousness.

I’ve used the market rally that began in July to pull out the weed-wacker and trim the portfolio a little bit and raise cash. If things rise from here, I’ve got plenty of skin in the game. However, the suffocating effect of rising interest rates is increasingly apparent. It will be very difficult to generate excess returns at present.