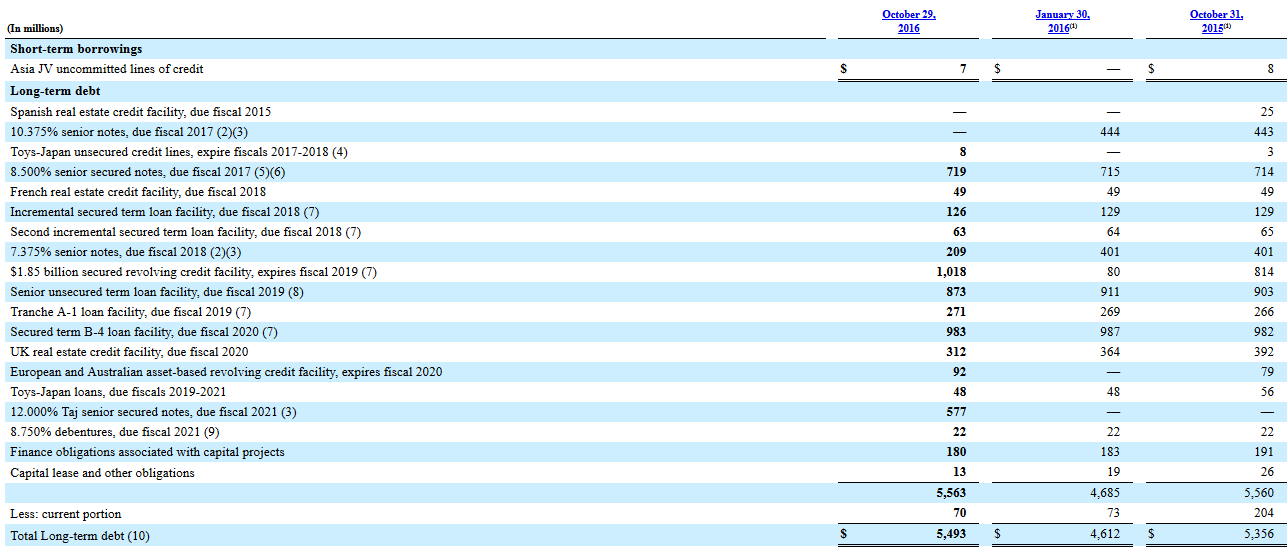

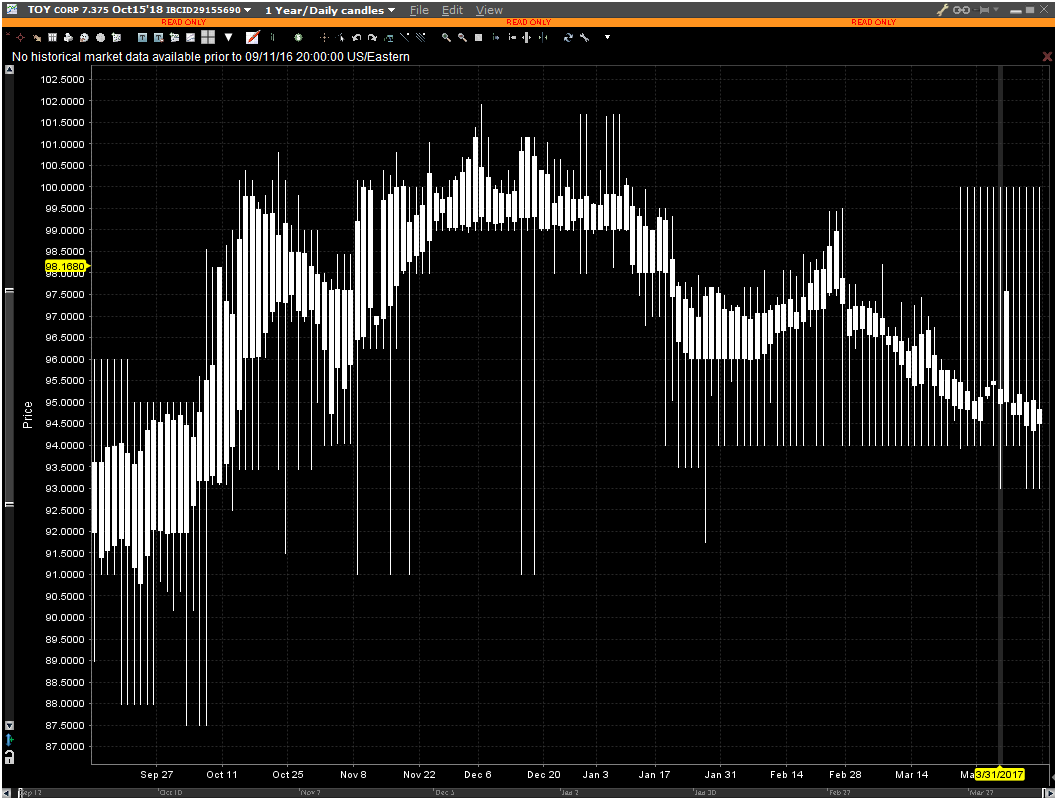

Earlier in April, I said I was going to avoid Toys R’ Us unsecured debt. It was trading around 97 cents on the dollar at that time.

I looked at my quote screen today for lesser-attention securities and noticed they (October 2018 unsecured debt) was trading at around 56 cents on the dollar on reports that on September 6th, they decided to engage a bankruptcy firm to explore options. The bonds went down from 97 cents to 78 cents in a day, and they’ve straight-lined to their present trading price (53 cents and dropping as I write this) a week later.

I ask myself from the perspective of credit analysis – is there any hope for unsecured holders? The easy answer here is going to be no – I count at least $3.5 billion that is either “secured” or asset/real estate based loans out of a total of $5.2 billion in debt. Although their credit facility is about half-tapped (i.e. they’ve got time to structure a restructuring), I find it unlikely that they’re going to wait around until October 2018 and pay off that particular unsecured issue. The advantage of going into Chapter 11 prematurely is simple – they can offer the unsecured creditors (lease landlords, etc.) an unfavourable “take it or leave it” type deal (see yesterday’s post on Seadrill), be able to shed their high-cost items (including conversion of their unsecured debt into a token amount of equity) and move on with life.

There is one reason, however, why this may not happen:

Although Toys R’ Us equity is not traded on an exchange, it is a publicly reporting entity. Bain Capital owns 32.5% of the corporation. Are they willing to give up this equity? I’m guessing their own private valuation of the entire firm is small in relation to the amount of debt that would have to be paid back (if Bain wishes to keep control).

Also if Bain controls most of the secured debt, their interests lie with Chapter 11 instead of keeping control of the firm (via their 32.5% equity stake).

I find this one difficult to judge, but I would weigh on the side of a restructuring that will involve a material impairment of value to unsecured bondholders. There’s just simply too much secured debt and I do not think they will hold Chapter 11 back a year and a month just to pay the US$208 million that’s due with this specific obligation (there are too many others that will be due as well). This is especially true considering the overall entity is not producing a lot of cash.

All in all, I’m glad I avoided this instead of reaching for yield and getting burnt (which would be the only explanation why somebody would have invested in Toys R’ Us unsecured debt in the first place).