Been busy looking at various securities (trying to pick the entrails of the crash earlier this February), but still haven’t found anything too compelling. I will especially note on the fixed income side of things there appears to be a lot of traps hiding (similar to Toys R Us unsecured debt last year went from 90 cents on the dollar to 20 cents in about a week). Want another value trap? Here is another.

I’m going to warn readers that things may be quite boring for the next little while. Investing right now seems to be a matter of forcing money to work and that is a recipe for losing it. So I’m continuing to wait.

One last observation:

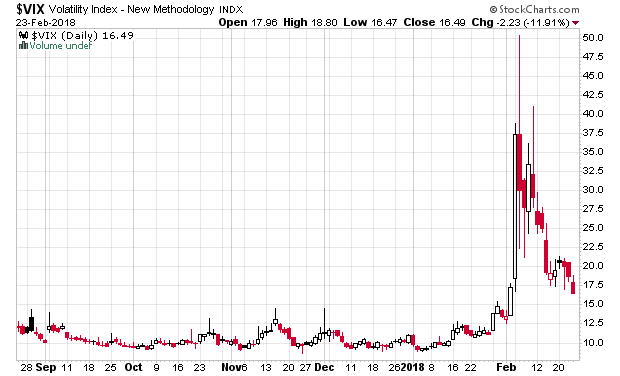

Do you think this is the market trying to lull people into a false sense of security? Convincing people that the mini-crash we had in early February 2018 was just some sort of aberration due to the overwhelming amount of money betting against volatility?

Instead, people should be paying attention to this chart:

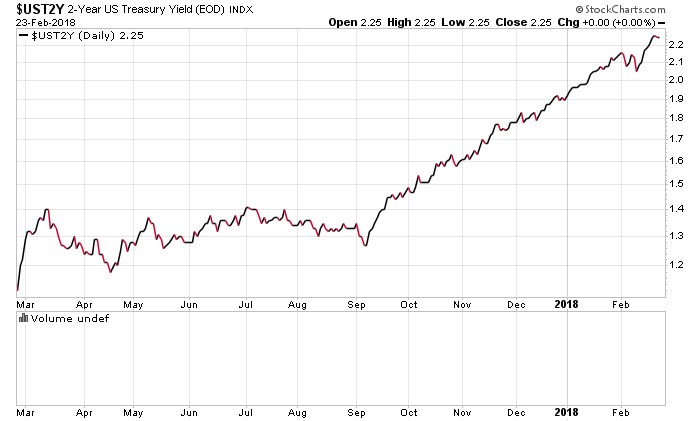

The trajectory here, if the last six months is repeated in the next six months, should frighten people. Coupled with the reverse of quantitative easing eating away at the general liquidity of the marketplace (move the slider on the bottom of the chart to show 2017-01 and beyond), is a recipe for asset price compression. Almost everybody of my generation has only seen rock-bottom interest rates and loose monetary policy during their adult lives. Adjusting to a culture where interest rates are not zero may take some getting used to.

With any luck, SVXY will continue its meander up and allow those of us who buy LEAP puts in it to rebuild the position sold in the recent meltdown. It is a quite likely doomed product. Options are for suckers, but I do think those in some of the leveraged products–especially those where the underlying may have liquidity issues–offer interesting upside in both sharp market breaks and gradual balloon-losing-air scenarios.

I think both another market panic and price compression (the 1st may become the 2nd if it continues into a “new normal”) seem likely over the next few years, and very likely–at least on the panic–much sooner.

Wouldn’t higher interest rates and inflation be bullish for the stock market? If not then what asset classes would act as hedges against inflation?

Hi Sacha, your cash call was spot-on. There’s crazy stuff going on, but if you step outside anything that’s part of the ETF/index-trackers/momentum trade then there are plenty of boats that still haven’t risen by the tide, nor are they leaky.

I hold, for example, a very large position in Texhong (2678:HK). 5 P/E, US$ 1.3 bn cap, owner-operator compounder (founded 1997, CEO 49 yrs old, holds 52.5%, very shrewd capital allocator in the higher ROIC core-spun yarn niche), trades just above tangible book with 28% 5y avg ROE, misunderstood as cyclicality is mostly just mean-reverting cotton-price inventory effect, and now going upstream by yet again buying depressed assets to gain a foothold and initial customer base. Yes it’s leveraged to a degree, but never had a losing year since listing in 2004. Payout rate is 33%. Should be absolutely fine longer term. Just plain uncanny to look at all these weed, crypto, and other pie-in-the-sky 40x sales stocks and then compare it with this.

On another fixed income note, I was looking at Yamana Gold’s “earnings” the other day. Just awful, terrible. It’s a total POS promotional company, losing money on every ounce they mine, with the CEO lining his pockets with $ 10s of millions over the years. Still, it issued $ 300M in 10y’s last Dec at 4.625%. Absolutely mental. Who in their right mind buys this stuff?

It’s difficult to lose money in companies that can sustainable trade at a P/E of 5 and not blow up due to financing problems.

Also with respect to gold mining, if you gave me a billion dollars I’m sure I can dredge up some gold in my backyard without doing any exploratory drilling. Doesn’t mean it’s economical to do so! I just like how these companies try to hide capital expenditures as if they didn’t exist or weren’t relevant to the business.