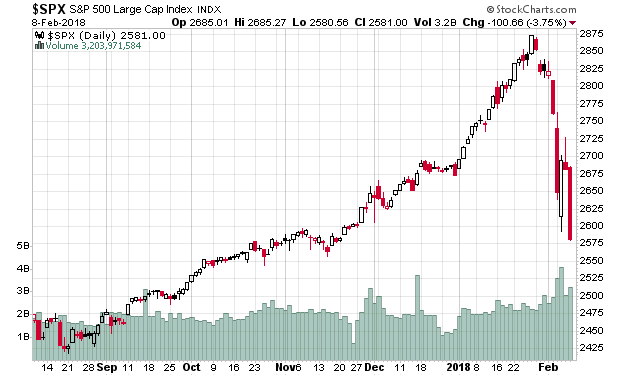

The S&P 500 is now down 3.5% year-to-date, while just last week I was writing about how it was up 7.4%. This, my friends, is over a 10% drop in the market in just 9 trading days. Incredible.

There will be a bit more vomiting but things will stabilize once all of the volatility-linked financial instruments continue their algorithmic unwinding. There has been a surprising lack of candidates out there that appear to me to be obvious victims of margin liquidations (unless if you so happened to own XIV!).

Yield-based financial instruments (prefereds, corporate debt) appear to be doing just fine. REITs have shown weakness, but probably due to markets pricing in the increasing rate environment. The Canadian markets haven’t been disproportionately affected – probably because the Canadian markets were never up that big to begin with. I’ve only seen significant damage in fossil fuel companies, but for obvious reasons (the federal and provincial governments are trying everything possible to kill the sector).

One of my talents that sets me apart from most others is my ability to side-step market crashes. I’ve done it in my very early years of investing in 2000, I did so in 2007-2008, 2016, and this week. I’ve had a few false alarms (I am financially paranoid), so I am not claiming perfection. Normally when circumstances become so obvious to invest (like it was in the first quarter of 2016), I do so, and go on margin. Right now, I’m roughly at 30% cash.

I’ve been trying to figure out how to deploy cash. One would think that a 10% market crash in two weeks would unearth some opportunities. If I find things exceptionally cheap, I have no problems dipping 10, 15 or even 20% in margin depending on the valuation parameters. But it’s nowhere close to doing this.

Something I’ve found very frustrating is there’s still nothing on the radar that has really attracted my visceral instincts.

I’d appreciate some suggestions.

I second that. I’ve been excited about possible bargains, but 10% off overpriced doesn’t mean cheap.

Looked at & bought some Eagle Energy: interesting to me because though it’s Canada-listed it’s increasingly US-focused, is highly-leveraged without pressing maturities and looks to generate a lot of cash at current energy prices for deleveraging, more aggressive drilling, or potential reinstatement of shareholder payouts. Management has not been madly dilutive and its shareholder base rotated/orphaned it, since it stopped paying a dividend (at the time they left the door open to reinstatement). However, most of the above factors could also be strikes against it, and I really don’t think it’s your thing.

ITG rhymes in my mind with KCG; I have been trying to get a better understanding of their operations so that I can buy more with confidence. Have you ever looked at them?

VRTV is of interest, especially after a ~20% selloff in the last week. I am reading up on them.

I always spend time looking in the US OTC market because there’s at least a possibility of mispricing; redoubled my efforts after the announcement that HRZCB, a holding for a few years, was being acquired. But it’s largely apparently-fairly-priced to moderately-overpriced banks, questionable industrials, and frauds. ACMT/ACMTA is one I bought a bit of recently: quite illiquid but trades at around .55 book , has been fairly consistently profitable, has bought back an enormous amount of stock in an acceptably-accretive way. Publishes its annuals and quarterlies, though not required to. Am trying to get comfort level with surety industry (including lingering asbestos risk) and with family control/incentives. I suspect it may be a quality company.

I am fascinated by PHH because as of last update they expected to generate and return to shareholders more in “excess cash” from business rationalization than their current equity value, and to have an adequately-capitalized stub generating positive cash flow remaining. But handicapping the odds of this are beyond me.

You are likely already familiar with ORM and RSO.

Some shipping, a few liquidations and similar, but I know those aren’t your thing. Some tiny US banks (BRBW, ASRV, TFSL if you net out the “phantom” MHC shares, others), but even profitable and at at under tangible book a buyout or restructuring is the most logical path to good returns in these highly-leveraged entities, so you have to subscribe to greater-foolism…

That’s both a lot and not a lot, and nothing seems like a can’t-miss. Have been somewhat amazed that the annual-lows list hasn’t yielded more.

Oh, and WAIR. It is a turnaround and so problematic but the specialized distributor model is one with some resilience and they are not wildly overleveraged or facing more than modest pressure on sales volume.

Few stocks ideas. I like a couple US hotel REITs – SOHO and HT (which I own). On the defensive side I am quite partial to Special Opportunities Fund (SPE) and also National Western Life Insurance (NWLI) – i own them both. NWLI has rock solid finances, trades at 0.62 of book value. Has a controlling shareholder who could be doing a better job of supporting shareholders but eventually that will change. He is old and will eventually have to pass over the reins or go the way of all men.

Please keep these coming. You’re giving me some good homework assignments.

I’ll quickly comment on ITG – they are very KCG-like, except financially lesser-performing in my opinion. In their domain, “lesser performing” is akin to me getting into a chess match with Bobby Fischer and expecting to me to last 15 moves. VIRT is definitely the top dog in this market (and up huge with their last quarterly report). VIRT’s publicly trading entity is about half of the “real” company, akin to IBKR being about 17% of the “real” company, which is why I don’t really take much interest in either of them. ITG’s financials speak for themselves as well.

Bit of a different beast, but the talk of VIRT and of complicated ownership structures made me think of BGCP. There are many things to dislike about them, but also many to like, and I would not bet against Howard Lutnick. I did think the price he hoped to get for Newmark at its IPO was too aggressive (the market agreed), and that’s been a drag on them even as Newmark appreciates incrementally.

Philbert and Sacha,

Along the lines of National Western Life, I’ll put forth E-L Financial (ELF). Trades at 62% of my estimated book value after Q4 is announced, 65% of book value today. The insurance arm seems to be well run now, and would make an attractive acquisition for any of the big players. Overlooked for multiple reasons: high share price, relatively small, high inside ownership, somewhat byzantine structure (holds minority interest in a closed end fund off which ELF is the majority of the portfolio, and the CEF is also at a discount). But consistently grows book value so I don’t think the almost 40% discount is warranted.

ELF preferreds are also trading at over 5% yields.

Take a look at NASDAQ:UNIT. It yields ~17%.

UNIT owns fiber and wireless towers and was spun-off from Windstream. Most revenue comes from the Master Lease with Windstream. But Windstream itself is currently distressed due to: (i) Ton of debt along with subscriber losses and (ii) Litigation by a vulture fund (Aurelius Capital).

Aurelius Capital basically acquired a big stake in Windstream’s bonds then filed a suit alleging that the UNIT spinoff of Windstream violated the bond covenants – and this is currently being litigated. FWIW: Neither the bond trustee, nor WIN’s lawyers, nor any other bondholders believe that a default has occurred.

The bull thesis here is that due to mission critical nature of UNIT’s assets, Windstream’s master lease with UNIT is actually senior to all other outstanding debt because Windstream needs UNIT’s fiber to survive. It’s similar to CORR’s situation in early 2016 when CORR’s two clients (EXXI & UPL) filed for CH-11 but accepted their leases. Without UNIT’s fiber, Windstream’s equity & bonds are zero. Ergo, even in Ch-11, Windstream will not default on its master lease with UNIT. See: https://seekingalpha.com/instablog/19055721-jz10/5047089-analysis-effects-possible-windstream-bankruptcy-uniti

The bear thesis here is that once Windstream hits Ch-11, vulture funds will drive negotiations during CH-11 and force UNIT to take a haircut and renegotiate the master lease with WIN.

Huh. WAIR moved a bit more quickly than I’d thought. Still worth a look.

I’ve looked into everything mentioned here, some with a finer tuned comb than others. Haven’t found anything meeting my thresholds. Of note, I found PHH to be one of the most confusing entities I’ve ever researched. Perhaps this explains why even their own accountants couldn’t figure out how to treat certain items of their balance sheet in the third quarter of 2017. Despite valid for accounting, I also find it somewhat disturbing they round all of their numbers to the nearest million.

I have prior knowledge of NWLI and ELF (TSX) – if I were to apply the “you had to invest 100% of your networth in one company” test, I’d pick either of those two compared to the rest. That said, NWLI and ELF are relatively unremarkable controlled entities that just so happen to trade deeply under book due to the fact that their controlling shareholders have zero incentive to give it up. I’d regard ELF especially as BRK-style. That said, I’m not really interested in either, but valuation-wise if somebody were to purchase them, they can do far, far, far worse.

PHH is amazing, isn’t it? And the current entity is less complicated than it used to be.

My holy grail (in both desirability and elusiveness) is another company like Boyd Group: a medium-quality but relatively noncyclical business where scale and density of service become an entrenching advantage and make their primary customers’ (insurance companies’) lives easier. Both Radnet and Crawford Companies might fit the bill, but it doesn’t take much looking to come up with plausible problems (I own both, but am by nature much more of a nibbler than you; after all, I purchased Taiga common!).

Any comments on Gran Colombia Gold latest news? Now that the stock trade above the conversion price, what’s the best way to play it? Convert to shares and cash out?

@Will: Tough to say until we see the “fine print”. This might be obvious, but I’m guessing what’s going on with trading is the market is anticipating less dilution.

Given how it hovers around the conversion price -was thinking about rolling some of my debts to the new debentures to at least get the warrant and get some premium – there’s a line about how existing holder can participate. Directed to email GMP Securities – no response. Very frustrating.

What about Sandstorm Gold?

@Philbert: Slick marketing, but betting half the bank on a mine in northeast Turkey seems to be the primary research focus. I treat them similar to other royalty companies (most of which have not had the greatest track records other than being very generous to management). Has been on the watchlist for awhile though.