Aimia (specifically their preferred shares) were suggested to me a year ago as a reasonable risk/reward and a relatively high yield.

I declined. Today is the reason that I saw would likely happen.

Air Canada will be ending their business with them in 2020.

Everything in their capital structure is trading massively down – common shares are down over 50%, and preferred shares are down about 30%.

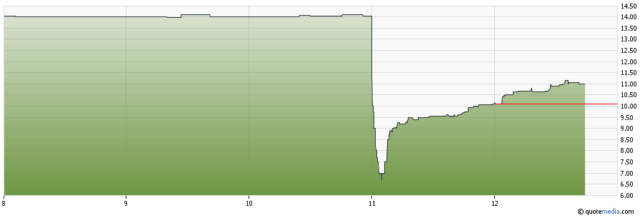

Good market timers could have bought when the margin calls were starting to flood in at around 10:00am Eastern time. The preferred shares at one point in time were down even more than the common shares.

(Update, I have included the chart of AIM.PR.A for illustration below)

{kind=link}

I have no idea what the business prospects of Aimia is (although this news about Air Canada is VERY negative) and thus I will still not touch them.

I will, however, be a little more diligent at liquidating the meager amount of Aeroplan points I still have remaining – companies like Aimia can decrease deferred revenue liabilities by simply increasing the cost of “rewards” that their customers have already pre-paid for (can you tell what I don’t like about their business?).

About 4 months ago I spent my last 250000 Aeroplan miles on a couple of business class flights….and cancelled my TD Aeroplan. Over the years I have had both good and bad experiences with them (about 50/50) The most frustrating thing about Aeroplan, is if you have a seat picked and they have a time/itinerary/plane change they re-issue you the ticket without your seat and you have to call back to Aeroplan or the airline to rebook your seat (if they still have it).

Good Riddance….lol

Prefs were a bargain yesterday. Understanding a complicated situation such as this can pay off when the uninformed need to sell at any price.

AIM.PR.A

AIMIA INC SER-1 PFD

– CA 3,000 $11.00 () $7.56 () $33,000.00 () $22,668.75 () +$10,331.25 +45.57%

Good trade Sculpin. Pays to be awake and looking at the quote monitors in these situations!

Thanks. Great blog you have here!

Just curious Sculpin, are you planning on exiting this trade at a particular price, or believe AIM.PR.x will continue to pay dividends indefinitely?

Will most likely exit most of this. I believe there is enough value in this Company for the preferreds to be made whole but am uncomfortable with the Board/management’s cash allocation to common dividends & buybacks under the current scenario. Cash should be used to pay down all debt, buy prefs at discount and position the Company for the post 2020 environment. Given the value destruction in the common equity & the questionable strategy of the BoD I would not be surprised to see hostile corporate action from hedge/PE looking to create value or maybe a strategic seeing long value potential here.

Marc – about your initial comment, any time a company has a 50/50 customer satisfaction rate, I would use that as a basis to never invest in terms of operational performance (there might be a financial reason to doing so, but definitely not on the business fundamentals). It is one of the reasons why my capital would never go near Aimia and I generally don’t feel much sympathy for those that get caught up in these Aeroplan miles / Air Miles schemes that have zero regulatory protection when they decide to dilute their currency (this is even assuming they make any product available).

I will never, however, under-estimate the innovation of marketing to get people to subscribe to these complex schemes in the name of “rewards”. It is quite a fascinating study in human psychology and it is a game we sadly all have to play whether we choose to or not (we all pay for it in increased costs, both monetary and mental). Same thing goes for maximizing credit transaction rewards.

That was me a year ago asking about Aimia prefs. I bought AIM.PR.A at $10.50 on July 15, 2016.

Unfortunately, I bought AIM.PR.B at $13.81 and 13.00 in 2017.

Saw this on Geoff Castle’s twitter feed. Wonder if HCG was selling out of any of the junkier prefs like AIM, BBD in etc…

Heard rumours earlier this week of a portfolio of Canadian preferred shares being sold at 10% below mkt. Looks like the seller was $HCG

https://twitter.com/geoff_castle