I’ve written a lot about this in the past, but Canadian real estate in urban centers is simply about too much capital chasing too little yield. Financially it makes sense to borrow at 2.83% like REITs such as Rio-Can (unsecured debt!!) and turn it around and invest it in a real estate yield product at 5.8% and pocket the difference in income.

This only becomes dangerous when credit markets start shutting down and you’re facing a cascade of debt maturities, or the collateral backing your loans (in this case, real estate) has a material mark-to-market drop (and then your debt leverage ratios will go out of whack and nobody will want to lend you money).

So I will bring your attention to interest rates. I’m fairly convinced at this point that until interest rates start rising (or we start seeing provincial governments enact serious foreign capital restrictions that can’t be easily bypassed like it is in British Columbia) we are not going to see any collapse in real estate pricing in Canada.

However, the US Federal Reserve is going to start to rise all boats fairly soon, and this will likely have knock-off effects in the rest of the world, including Canada.

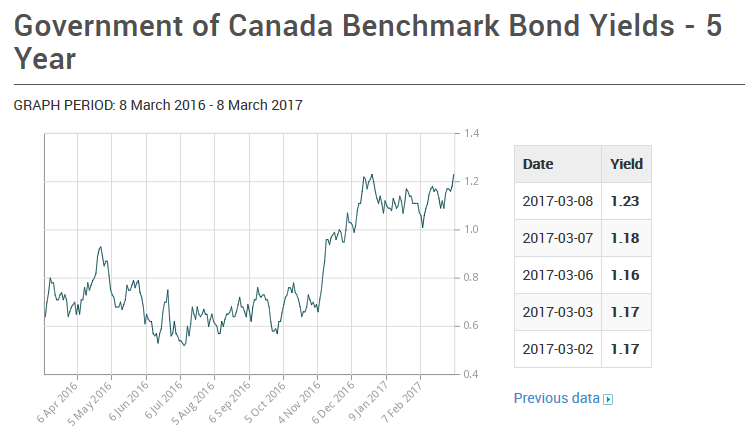

I’m looking at Canadian interest rates at the Bank of Canada, and notice those longer term yields start to creep up again – 5-year government bond rates are at 1.23% and the trend on yields are seemingly upwards.

It remains to be seen whether this is white noise or whether this is the start of a trend, but it is something worth watching. If interest rates normalize to something resembling historical standards (e.g. 2% higher than present levels), Vancouver residential real estate that is currently renting for a 3% cap rate would be selling for a 5% cap rate – the result would be a 40% drop in price. This is not a prediction, it would be financial reality if a 2% rate increase occurred. Leverage has gotten to the point where such a change in interest rates would cause significant financial dislocation and this is likely why central banks are very afraid to make sudden changes to short term rates.

Yeah – led me to recall the initial ScotiaPlaza deal.

On a side note – your thoughts on the term of GCM’s proposal on the 2020 debt?

Will – if it is what it seems to be according to the PR, a holder has to weigh in the extra income, and extra embedded option value (more time = more theoretical value) vs. getting paid back sooner. The downside is the structural subordination of the 2024 notes, risks to gold pricing (e.g. can they actually make money?) and “How come they can’t find anybody to buy the company if it really is this cheap?”. So there’s a lot to consider and I think it is situational to an investor’s preferences (the insiders probably just want to dredge more money out of the corporation with the higher coupon).

One thing for sure is that the U’s are likely to get 81% equity converted, which means the capitalization is entirely based on the senior secured US$101 million par value interest of the V’s. If you think the whole thing (debt-free) is worth more than US$84 million (current market value is 83% of par) plus whatever margin of error then the secured debt is a buy. Ultimately there is commodity risk here at play – but this is obvious.

I don’t have a clean yes/no on this which probably means it is a good proposal, where nobody is entirely happy.

Agreed on real estate and interest rates.

On GCM.DB.V, I think they are hoping the extension out to 2024 will make prospective common shareholders not worry about what will happen at maturity of the debs which will help increase the valuation. In the meantime, they can keep using FCF to buy back debentures until they trade at par or are all gone. Hopefully at some point the stock will trade above the conversion price and it won’t matter.

Safety – depends on how many of the .V holders opt for the 2024 extension. By the wording of the press release it looks like it will be an opt-in, and there will be two separately trading issues of debentures. I also don’t see why the market would “forget” about the fact that there is US$101M of senior secured debt above everybody else and until this is cleared through (or converted to equity) the upside equity potential is limited to US$0.13/share due to dilution.

Why isn’t anybody buying the firm (or at least the senior secured debt) if they are so cheap on the financial metrics?

Valuation is not really limited due to dilution. Even at the fully diluted 1.4bn shares outstanding, 4x 2017E EBITDA at US$1200 gold gets you to US$0.16/share. It’s likely not trading there for a lot of reasons besides dilution.

They say they are going to generate US$15m share in FCF this year. If the gold price were to stay flat that FCF should trend higher as they finish catching up on sustaining capex they slipped on over the last few years. It’s possible, they will create enough FCF to pay off all of the debt by 2024 especially if the gold price ramps (big if!). So it’s not necessarily forgetting as much as it’s not as big a concern.

As for being acquired, I think some of the political concerns means the shares won’t get anywhere near fair value if the company were to be sold. It’s also for an acquiring BOD to approve a 200%+ premium and hard for the GCM BOD to accept less. Plus the BOD owns a decent amount of 2020 bonds and I assume he wants more than 100 cents on the dollar. Perversely, the chance of being acquired might go up if the stock gets anywhere near fair value. Of course at that price, the debt is no longer an issue and the discount might lift!

not sure if I’m reading this right…..if approved, is it still 6% until 2020, then 8% to 2024…or 8% for the whole term?

Forgot to answer this. It’s not clear until the official documents come out in SEDAR. I’d suspect the 8% would kick in immediately.

thanks Sacha

@Marc: Looks like it kicks in immediately after it is done.

Also GCM.DB.V gets delisted if less than $2 million par is outstanding.

My guess is that they’ll get a 2/3rds take-up rate.

It’s a tough call whether to convert or not which makes it a reasonable proposal.

thanks for the update Sacha