Bombardier’s bonds have traded considerably higher since their latest 8.75% bond issue (maturing December 2021) which is now trading at a premium to par.

They have to be looking at this and thinking about securing further long-term funding. It also gives them a lot more negotiating power with the Canadian government, who wants to inject some more money into the corporation (whether they need it or not) for political reasons.

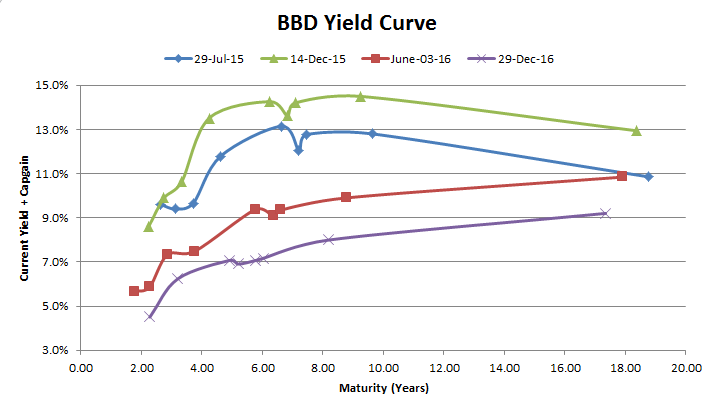

Floating rate preferred shares are yielding 8%, while the fixed rate is yielding 9% (quite the premium to pay for a floating rate). Given the difference between the bond market and the preferred share market, I still believe the preferred shares are trading slightly cheap to what they actually should be.

The equity is also receiving quite a bid as of late, despite the massive warrants overhang in their earlier year government fundings. If they receive another large order for C-Series aircraft (something slightly larger than Air Tanzania), it is quite likely the stock will rise even further.

“Given the difference between the bond market and the preferred share market, I still believe the preferred shares are trading slightly cheap to what they actually should be.”

AMA: Can you explain how you calculate fair value for the preferreds? Is it more a function of stock price or interest rates?

There’s no exact science, but one weighs the relative risk and merits of holding the preferred shares vs. the debt. The common share price can also be a barometer of whether they will choose to suspend dividends. In the case of Bombardier, credit quality is also a very important consideration as their common share dividend has also been suspended and they are currently burning more cash than they are generating.