Since February, yields have compressed to the point where I am getting a bit suspicious that we are going to see some spreads widen again whenever we get some sort of credit event that will cause another round of financial distress. I am not forecasting when this will happen, but historically speaking, the lead-up to the presidential election always causes unwelcome volatility. Right now the assumption is that Hillary will win, but between now and the early November election date, things will change when the public actually starts to pay attention again to their two choices.

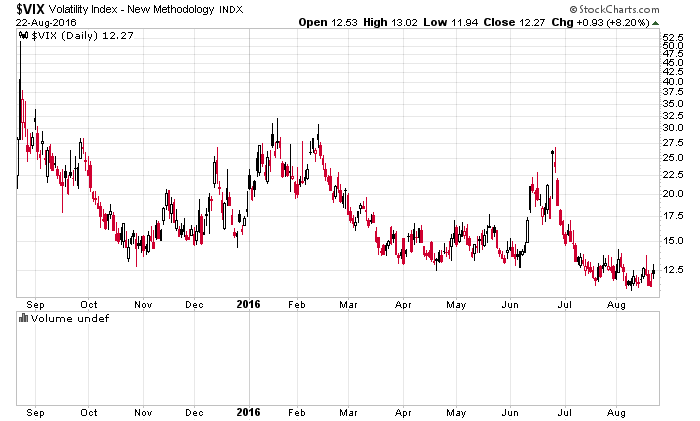

The markets, however, do not appear to indicate to price in much risk. Following is a chart of the VIX:

The last time volatility got that low was back in the middle of 2014 (remember when oil was at US$100/barrel?).

Volatility is typically anti-correlated to positive price movement. Right now, investors that sell risk on the main index are not receiving much money for what is a piddling amount of yield – an at-the-money option sold a month out on the S&P 500 will only yield an investor about 1.1% on their at-risk amount, which is very, very, very low. Looking out nearly 5 months to mid-January, that same premium is 3.7%.

In the event of a market crash, an investment in put options not only profits due to the pricing differential between market and strike, but also due to the increase in volatility that occurs during turbulent markets. There’s probably never been a better time to invest in a potential market crash than right now, but the phrase that says markets can be calmer for longer than one can remain solvent applies.

Indeed, I am seeing many market prognosticators talk about skepticism of the existing market conditions, that the indexes (which are at all-time highs) are sputtering, that the economy recovery is long in the tooth, etc, etc. This does not bode well for crash conditions, which happen when there is stress and underlying causes to force entities to liquidate at all costs.

I can’t conceive what could cause crash conditions other than a major WMD event to the scale of a 9/11.

I still believe that a cautious approach is appropriate and that the market participants that will get the most out of the market will do so on the fixed income side. However, these opportunities I have noticed have basically vanished from the good risk/reward column to just ordinary. Ordinary valuations are good enough for me to hold onto things, but not nearly enough for me to invest in.

I was fortunate enough to fully participate in this market cycle, but in general at present, I am in a very slow liquidation mode as I do not see much worth investing in. There are a couple portfolio components (fixed income) that are trading at prices that are within 5% of me dumping it, but I am no rush for them to get there – I will keep collecting dividends, distributions and interest to pay down the very low interest margin debt. In general, I see about a maximum capital appreciation of about 15% in the remaining portfolio for still relatively low risk – even if the actual appreciation is zero, the weighted average coupon is 7.9% and I get paid to wait.

If we get some sort of spike that caused a general portfolio rise of 10%, I would have sold enough to have a healthy double-digit percentage cash balance. If this portfolio spike was 15% from present levels, the only things I’d be holding would be my bonds to maturity (unless if those too were trading ridiculously above par value). Then I would go on vacation and wait a long time.

Sometimes I am furiously active on trading, and sometimes there are very dull moments. The past few months have been very dull and I’ve been twiddling my thumbs. My investment strategies have been working and there will be a time to shift gears once my current strategy has run out of gas. Just not today.