The provincial government in British Columbia is trying to balance the politics of housing prices in the Greater Vancouver Regional District and the fact that housing and housing-related economic activity is our #1 source of economic activity.

The government knows that if they take policy decisions to snuff out the fire that is currently raging in real estate that they will collapse the economy into recession – our other industries (mining, forestry, oil and gas) have been withering away and this leaves real estate as our number one export.

Managing a “controlled landing” will be an interesting feat. I’m not sure whether the government can do it, but we will see!

CMHC released a report (July 27, 2016) confirming something almost anybody on the ground here knows: in real estate, there is “strong” evidence of problematic conditions in the Vancouver and Toronto regions of Canada.

This has implications for mortgage insurance. While rising prices is great for mortgage insurance (i.e. there is a much lessened chance for mortgage defaults), the residual concern is one of regression to the mean – if insurers write policies for people taking mortgages at the peak of pricing, insurers will have a considerable amount of downside exposure in the event there is a deep decrease in real estate pricing.

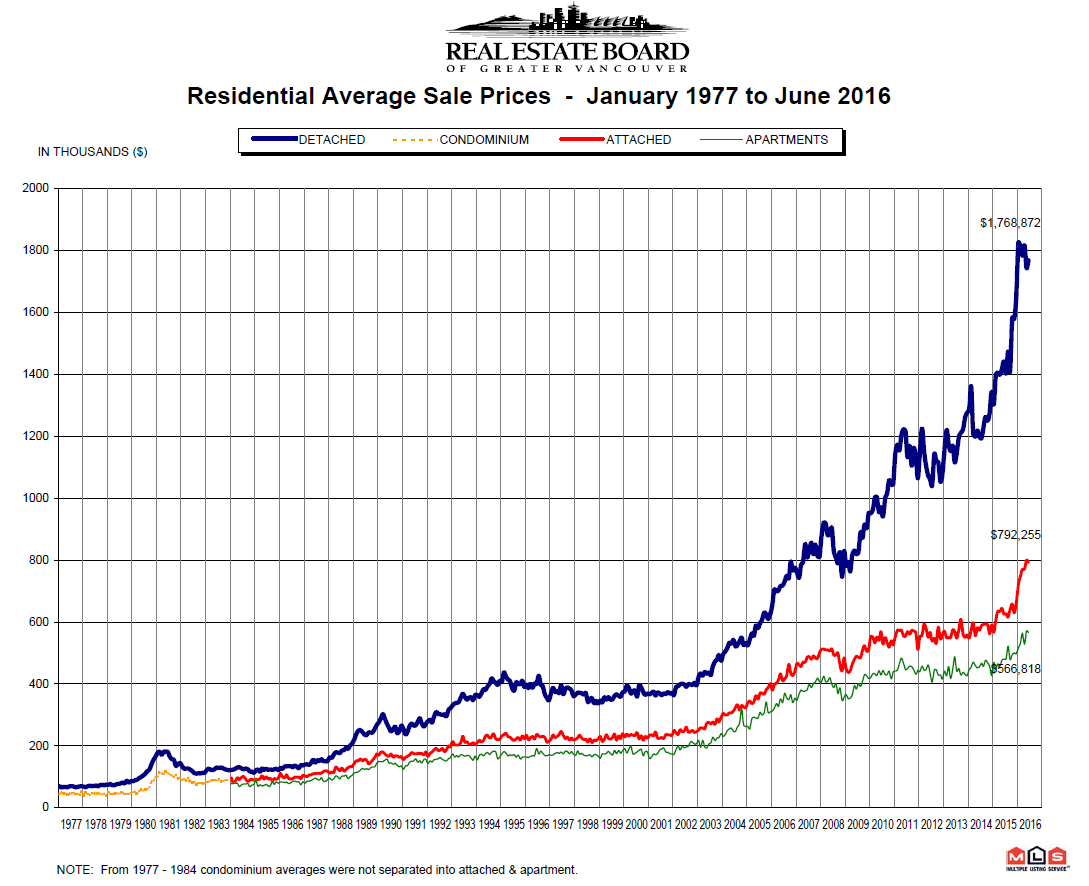

The last time that real estate prices fell for any significant period of time in the region was back in the early 1980’s:

Interest rates at that time were in the double digits. Real estate from the beginning of 1981 to the end of 1982 dropped by about 40%, but you would never detect it by looking at the chart above – this is why stock charts use a y-axis that is logarithmic scaled, not linear like the one you see above.