North American Palladium (TSX: PDL) operates a mine which has been somewhat profitable, but financing expenses have killed any chances of the overall operation returning money to shareholders.

Balance sheet-wise, they invested $450 million in mining operations, while having a $220 million debt to deal with and a requirement for some cash, which they do not have. A classic case of solvent, but not liquid.

The primary cause of this was doing a deal with the Brookfield devil, where management borrowed US$130 million at a rate of 15% interest in June 2013. The debt was secured by PDL’s assets. Not surprisingly, it has gone financially downhill since then. The debt has since morphed into US$173.2 million as interest has been subsequently capitalized into the loan (and other drama that has happened since that point which I will not get into).

What’s amazing is the corporation somehow managed to find enough suckers to invest in some toxic convertibles in 2014 that significantly diluted the company’s equity but kept enough cash to keep the zombie alive for another year.

Finally, they succumbed to having a quarter of your revenues go out the door in the form of interest expenses and are coming to grips in the form of a recapitalization proposal.

The term sheet (attached) that management came up with to ensure its own survival is quite onerous to all involved.

The salient details are that existing shareholders will keep 2% of the company, unsecured debenture holders will receive 6% of the new company, and Brookfield and partners will keep the 92% after generously injecting US$25 million and releasing their accumulated debt to the firm. Afterwards, Brookfield will float a rights offering where they will raise another CAD$50 million and this will presumably dilute the interests of the then-common shareholders even further if they do not wish to participate.

A holder of 52% of the convertible debentures has been spoken to and agrees to this proposal. They need 2/3rds approval, which is likely considering that the convertible debentures are unsecured and they would receive nothing if the company went through the CCAA route.

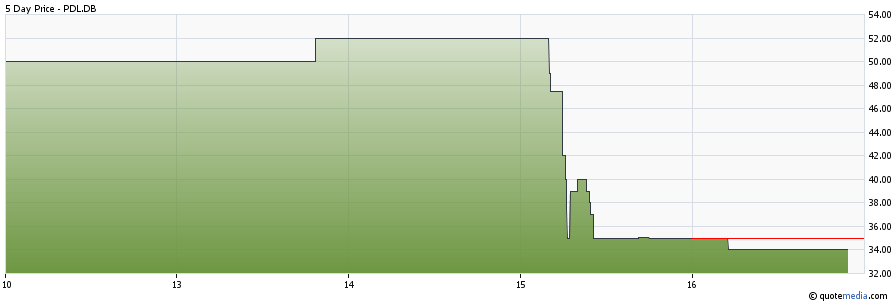

Not surprisingly, existing shareholders/debentureholders of PDL took down the price:

The recapitalization document was released on the morning of April 15, 2015 half an hour before trading opened, so astute traders that could skim through the news release and the actual term sheet would have been able to get out at 19 cents if they hit the opening market trade. If you waited until the end of April 15, you would be sitting at 12 cents.

At 7 cents per share of PDL stock and roughly 400 million shares outstanding, the market is valuing the recapitalized version of PDL at CAD$1.4 billion.

It does not take a genius to figure out that, with $220 million in revenues in 2014, the existing stock price is still significantly over-valued. If I was owning any shares of this train wreck, I’d still be dumping at market. Fortunately I’ve never owned any shares (or debt!) of PDL. Purchasing a mining operation at 7 times revenues is not exactly a value play.

However, the albatross of having to deal with a crushing 15% senior secured loan will be off their backs and the resulting entity may have a fighting chance when it doesn’t have to shell out $50 million a year in interest expenses. You just have to figure out at this point what Brookfield’s incentives are to ensuring they get the most of their 92%+ equity stake in a post-recapitalized PDL.