Be warned that the following is a very unfocused financial commentary on a bunch of topics.

Everybody is trying to figure out when the US Federal Reserve will raise interest rates.

My own opinion is that they will wait as long as possible and not get caught up in the market mania that is currently projecting a 1/4 point increase sometime mid-year. December Fed Funds Futures say that the year-ending rate will be 0.5%:

While unemployment figures would suggest a rise in rates is warranted (as part of the Fed’s mandate is employment, unlike the Bank of Canada, which is purely inflation-driven), with very obvious global deflation occurring, the Federal Reserve should merely be happy that the markets are buying into the threat of higher rates, rather than having to do the job themselves. This persistent threat, but consistent inaction, of higher USA interest rates will likely be the theme for the rest of 2015.

Absent of World War 3, it does not appear that inflation is rearing its head. Too many central banks are trying to stir up inflation with their versions of quantitative easing programs. Japan and the EU are trading moribund, while even China is lowering interest rates and loosening credit policies (as they do not want to precipitate the collapse of their finance system quite yet).

What does this mean for Canada?

Part of Poloz’s strategy is to wean markets away from forward guidance. I’m not sure what the master strategy in doing this is, but by eliminating forward guidance, effectively Poloz is telling the markets to come to their own conclusion in absence of information from the central bank. Thus, it is likely that the Canadian central bank will lag markets rather than lead them. My guess at this point is that they will be standing pat for the indefinite future to see where all the cards lie. Effectively the quarter point move was a signal to the market that “We’re not going to play the soothsayer game anymore.”

The threat of higher US interest rates can only take US currency so high relative to all others. If the threat is executed on, then the next threat will be even higher rates, etc. Since I do not believe the threat is going to be executed on, it would stand to reason that we will be in a holding pattern in the macro scene for the next little while.

Institutions that have taken advantage of extremely cheap money are likely to pare back their leverage, but non-financials should do reasonably well, excluding US exporters.

The forward curve on crude markets is at an extreme point right now and does not bode well for future prices beyond that of the contango slope. That said, there are a few entities out there that are trading as if the entire province of Alberta is going to shut down and while things should get bad in Alberta, they should not get that bad. So watch for opportunity in that area.

As for Canadian real estate, the calls for its demise are loud and clear, but absent of sudden rises in interest rates, I very much doubt it is going anywhere. There is simply too much capital flooded in the market and still too much availability of leverage (either by bona-fide purchasers or investors, whatever the case may be). One item of relevance in Canada vs. the USA is the heavily urbanized and sectorized nature of the distribution of our country’s population and effectively each population center has its own variables affecting real estate valuation.

There is a good component of foreign investment (whether by nominally “resident” Canadians or whether it is through offshore capital) in Vancouver and Toronto’s markets and I do not see signs of this drying up, specifically from China.

Finally, something that I am looking at but is nowhere close to the point where I would want to be accumulating yet, is an odd choice. Gold.

One of the arguments against Gold is that it does not bear any yield. In economies where you end up paying negative yields to invest in sovereign debt (e.g. Switzerland, Denmark, and a lot of the EU), it actually makes some sort of sense to hold value in alternative vehicles, whether that be paper currency or the world’s historical store of value. At CAD$1480 it doesn’t make too much sense from a risk/reward benefit, but in the odd scenario where this goes down a third like the rest of the commodity market, it will be worth looking at. As always, time will tell.

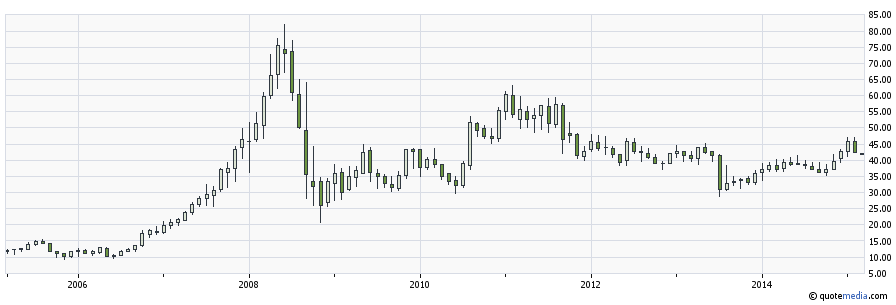

There is also one other commodity that has caught my attention, not for being exciting, but rather for being nearly dead and having very unfavourable supply/demand economics to the point where nearly all interest in it is gone. In fact, the only ETF I could find is rather undiversified to say the least simply due to consolidation in the industry. Still doing research – although the metrics look horrible, when one looks at the rise of other commodities, nobody ever tells you when things will rocket up. Just look at Potash Corp (TSX: POT) from 2006 to 2008:

Getting the “when” correct is always the big challenge.

Economically speaking, it is rational for oil to get back to a “new normal” at US$70-80/barrel given ever-increasing world demand, but I think it will get there later than sooner. We need to see actual shutdowns rather than simple statistics of drilling counts being gutted. When I see companies like Lightstream still dumping $100-120M in capital expenditures (albeit they are going to drop about 20%-25% in production from year-to-year) this is a relatively good sign for upcoming supply drops, but there needs to be time for this to get worked in the system. Most companies are incorporating US$65-ish prices in their financial models and with those rosy projections, it still means they are going to be overspending on the oil patch.

Better to look for businesses that were disproportionately hammered by the plunge in oil prices rather than the commodity itself at this point. Unfortunately my assessment of the situation back in the second half of 2014 was completely incorrect and I have moved on.