This is a rambling post, so be cautioned that there is little rhyme or reason to the thought pattern here.

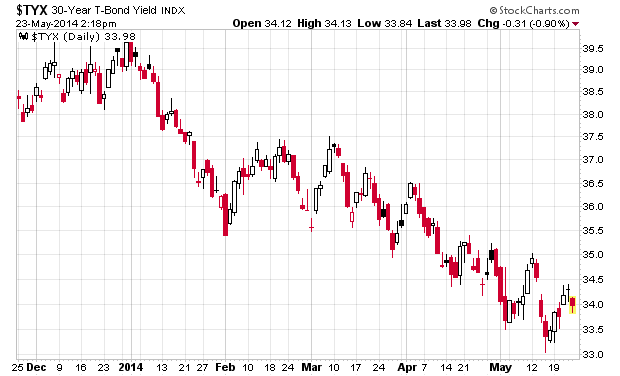

I look at the following chart of the 30-year treasury bond:

The risk-free return is very low at present. Relative to other sovereign entities (e.g. Euro-zone, Japan, Canada, etc.), however, the US 30-year bond actually still looks cheap and this can explain why it is the best performing asset class in 2014 to date.

As an exercise to the reader, please reconcile what we are seeing in front of us:

– S&P 500 is at all-time highs (approximately 1,900 as I write this)

– The economy appears to be plodding along at a low real rate of return

– Inflation is rising but not at ridiculous proportions (yet)

– US currency appears to be making a comeback

– Short-term rates are still basement low (fed funds target is 0-0.25%, but the effective daily rate has been closer to around 0.09%)

– Long-term treasury rates are relative low (see above chart)

– US government is still projecting $500 billion deficits although this is quite better than previous years; other liabilities (e.g. social security) and various other entitlements (e.g. pensions) generally remain huge liabilities and difficult to get a good rate of return

– Almost every retail Joe that is not involved in stock (lottery) picking is dumping their money in a variety of index funds that invest in the same things in the same proportions (Typical Canadian allocation: 40% TSX 60, 30% S&P 500, 30% some fixed-income ETF)

The demographic story is that the bulk of the population pyramid is entering in the stage of life where they are transitioning their capital into income-bearing instruments, which accounts for the very high cost of yield at present.

It remains very difficult to say whether we are entering in the Fairfax world of upcoming deflation despite everything (which would guarantee low interest rates for some time to come), or whether we’re entering some sort of inflationary world (because of all of the available credit, which would presumably translate into spending and consumption).

Although my style of investing does not depend on macroeconomic outcomes, it is always nice to know where you have the winds at your back. In terms of the big world-picture view, it is difficult to tell where these winds are blowing at present.

The only real convictions I have at this point is a general aversion to commodity-related products and a realization that those that are paying for yield are likely paying a premium beyond what the risk/reward ratio would suggest.

In other words, you are more likely than not to find the “hidden gems” amongst the list of zero-dividend yielders (or very low) on the equity side. Due to the “rising tide lifts all boats” phenomenon that we are encountering at present, until we see defaults of junk debt issues that go out for insanely low coupons and high durations, finding these gems is not easy. Most of them have been bidded up.

This leaves potential investment candidates in very un-ideal categories: the nearly illiquid and special situations (e.g. spinoffs, emerging from Chapter 11/CCAA, SEC/SEDAR “fine-tooth comb required because GAAP financials simply don’t explain the story” companies, closed-end ETFs, etc.). Not a lot of pickings here.