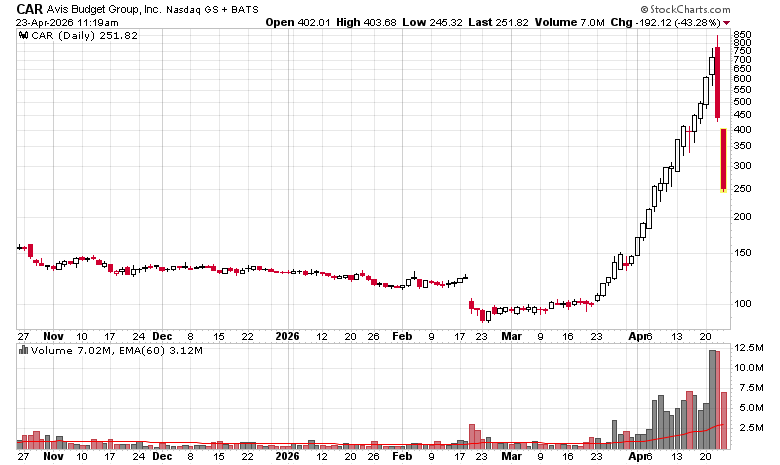

The bipolar market continues – we have companies like Rocket Lab (RKLB) shooting up into the stars, presumptuously in anticipation of the SpaceX IPO, and companies like Sandisk rising by a factor of 20x over the past year.

Conversely, I am looking at most of the usual suspects in software being down for the day – ADBE, CSU, etc.

The war in the Middle East still continues and a good chunk of the world’s crude supply is still out of circulation. Every day that this continues is another layer of embedded cost in the real economy, which will take months for the ripple effects to show themselves. When the ripple effects show up in financial statements, many reactive algorithms will make adjustments accordingly.

I do note that many “traditional” names are fading away – Nike (NKE), Whirlpool (WHR), and LuluLemon (LULU) are depressed far below their traditional norms – are these brands going to be the Kodaks of this decade, where the foundation of the companies has essentially been hollowed out over time and not maintained? The only difference is that Kodak was a technology adaptation failure, while the three aforementioned companies are marketing brands, where shoes, washing machines and lifestyle clothing

Conversely, from a broad market perspective, perhaps this is the market’s way of saying that the “death of money” is occurring – and claims on companies that produce goods and services is what is driving demand and not necessarily the quantity of earnings they derive from fulfilling such demand.

Despite having a huge cash fraction in the portfolio, my YTD is still better than the primary indexes. It’s a very odd situation in that I do not feel particularly satisfied with the performance even though objectively things from a risk-adjusted perspective can be considered borderline perfect. It’s difficult looking at these things that are going up 20x in a year like Sandisk and wondering why you don’t have one in your own portfolio. Even if you took a 2% position in the stock at the beginning, if it goes up 20x, it would balloon to 29%.