When will we start hearing, once again, “Windfall profit taxes” in relation to oil prices?

Eyeballing the chart, we have spot WTI US$60 for January, US$65 for February and so far in March, let’s call it US$85.

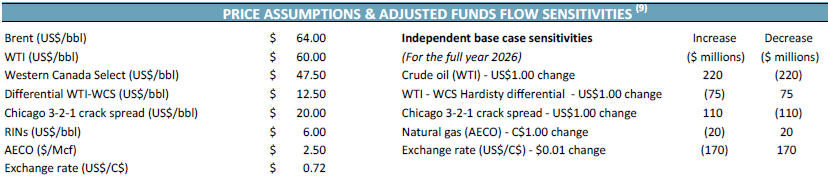

Just as an example, we look at Cenovus’ sensitivities:

CAD$220M/year in “adjusted funds flow” sensitivity per dollar of WTI, so a first-cut analysis of a US$20 one-month change in WTI would be about CAD$370M in cash flow, or about 20 cents a share. For a single month of elevated pricing.

Suncor is about C$215M/year per US$1 change in WTI. CNQ forces you to do your own homework, but very roughly, my paper napkin has a model going from US$65 to US$85 WTI resulting in a change from $4 to $7/share in free cash flow (assuming things go for a whole year).

Given the extreme slope on the oil futures curve (spot oil being US$88, give or take, while December 2026 crude is US$75, a 15% discount for patiently waiting 9 months for your delivery), this windfall is not expected to last. Or will it?