There has been a considerable amount of bandwidth on the future outcome of Teekay and Teekay Offshore on the Seeking Alpha channel.

When you see this much bullishness on a public forum, watch out. The “news” (if you want to call it that) has already been baked in.

There is also a material amount of mis-information in some of the analysis presented on Seeking Alpha, including the J Mintzmyer analysis which got most of the flurry of TK/TOO posting started. There’s no point for me to argue about the fine details of the analysis here.

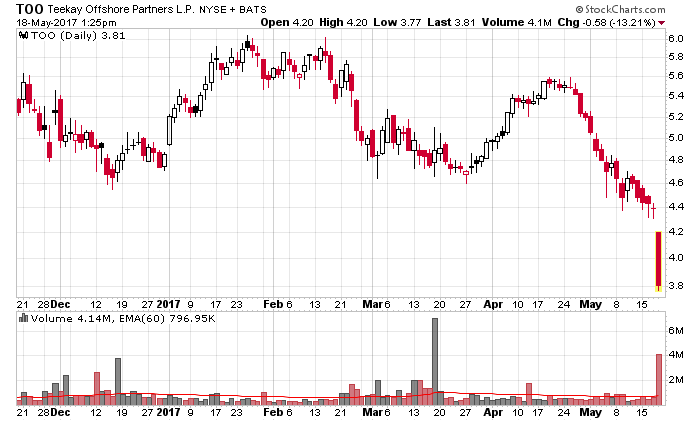

My original post about Teekay’s 2020 unsecured bonds of April 2016 still applies today – at a current price of 90.5 cents on the dollar they are in the lower part of my price range but not a wildly good buy as there is real risk involved. My initial purchase point was below 70 cents on the dollar back in early 2016. My only update to my April 2016 post is that I have long since offloaded my Teekay Offshore equity position – my optimism back then about TOO was considerably over-stated and when my own modelling changed, my price targets subsequently changed and I bailed out.

TK’s inherent value is primarily focused on their TGP entity (Mintzmyer got this correct, but grossly over-states the value of the company). Most of the discounting of TK unsecured debt’s value is that they are likely to offer guarantees to future TOO and/or TGP financings that would make it difficult for TK unsecured debtholders to realize value in the event of a Chapter 11 equivalent event (this would involve cross-defaults between entities and be incredibly messy to resolve). There is currently cross-default potential with TOO’s debt complex, not to mention that TK has made unsecured loans to TOO to bridge TOO’s liquidity situation. My general expectation is that there is a gigantic incentive for the controlling shareholder (Resolute Investments) to avoid a default scenario and would instead opt for a dilutive recapitalization instead, which would of course render TK unsecured debt maturing at par. I still think this partial recapitalization scenario is probable.

TK and TGP have announced dividends and distributions, respectively. The TK dividend surprised me somewhat as they are obligated to pay dividends by raising an equal amount in equity capital until a certain debt is paid off. TOO has been silent and they will likely be announcing suspensions in conjunction with some financing announcement in the upcoming weeks.

My assessment at present is that the only people that will be coming out of this with money are the debt holders. Such is life when oil is at US$45/barrel.