This is another rambling post with no coherency. The quarterly reports from companies are flowing in and I am reading them – but there are few companies that are below my price range where I start to care about them in detail. As such, my research pipeline at this point is in the exploratory mode rather than doing detailed due diligence.

It is in the middle of summer and I am not expecting much in the way of volatility – it is truly a summer where major portfolio decision-makers have decided to take away from the trigger switches.

Accordingly I have been sitting and watching with respect to my own portfolio while I do my casual research. Probably my biggest error of omission was watching the solar market rise over the past six months – I’d written them off, along with almost everybody else, as languishing when the price of fossil fuel energy dropped. A lost opportunity there – there was one company in particular which I earmarked, financial metrics looked great, but didn’t even pull the trigger, primarily due to insider selling. If I executed correctly on it, I would have been looking at a double now. Oh well.

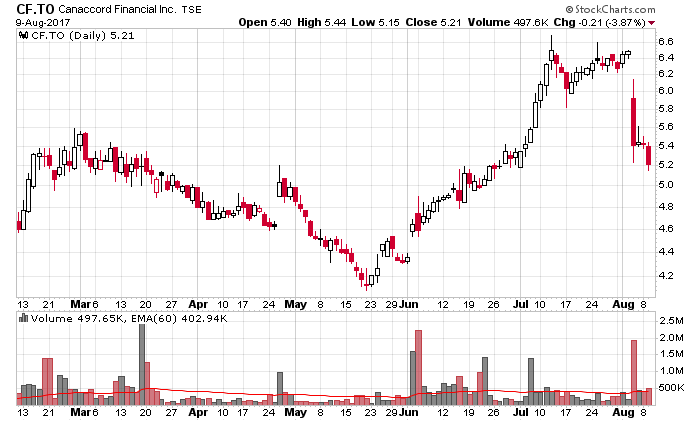

An equity chart that caught my attention was the high expectations of investors of Canaccord pulling a great quarter, which came nowhere to fruition:

This is very obviously the chart of expectations crushed after a quarterly report – a regression to the recent mean would suggest a $4.50-ish stock price. I also notice their domestic competitor, GMP, being crushed after their quarterly report.

I also notice most liquid fossil fuel companies are getting hit badly and are close to multi-year lows. In the USA, most of the companies receiving boosts are the ones that have had been relieved of their debt burdens through the Chapter 11 process (LNGG is a great example of this). I still don’t think equity holders of fossil fuel extraction companies are going to be too happy over the next 12 months.

I also took notice with Interactive Brokers, and Virtu’s commentaries with respect to Q2-2017 as being one of the lowest volatility environments possible – they are two types of businesses that generate revenues as a function of trading volumes. Volatility correlates negatively with an increase with the broad markets – I am looking for defensive-type companies that will do okay in an environment like present, but will really do well when volatility increases.

Interactive Brokers is a classic example of a great company (they are the best at what they do by a hundred miles over everybody else), but one who’s stock I am not interested in buying at current prices.

Mostly everything in the Canadian REIT sector seems to be over-valued. An interesting trend is that the downfall of retail is somewhat being projected by RioCAN’s chart – trading below book value, it might seem to be an interesting value, but are they able to keep up occupancy and lease rates to businesses that have to compete against Amazon? The residential darling of the market is Canadian Apartment Properties (CAR.UN) but they are most definitely not trading at a price that would suggest a future performance beyond a high single digit percentage point and this is under the assumption that their real estate portfolio asset value remains steady. Trading in the entire REIT sector seems to be entirely yield-focussed which is never a good basis to invest, but it is a good basis to evaluate other investors’ expectations on these entities.

Gold has also been up and down like a yo-yo and might be an interesting bet against dysfunctional monetary policy. Unfortunately my ability to analyze most gold mining firms is generally not that fine tuned.

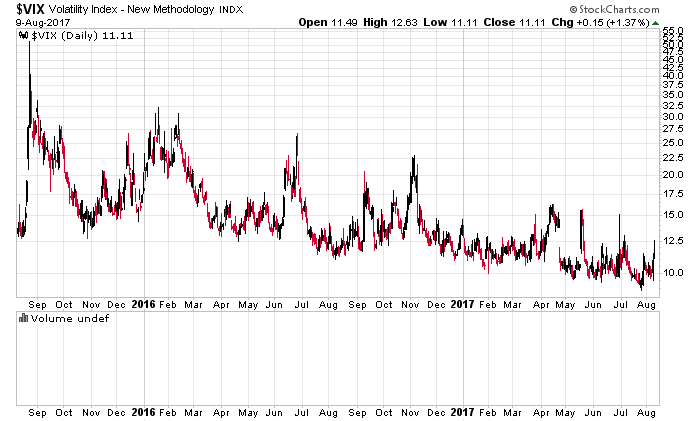

The liquidity of my overall portfolio is very high (nearly a quarter of the portfolio is collecting dust at a short duration 1.5%), but right now I don’t see much investment opportunity that would suggest avenues for outperformance. I could shove the money into some sub-par debenture (e.g. TPH.DB.F which buys you a 7% coupon until March 31, 2018 maturity) but do I really want to lock my capital into something that is questionable? It is the literal metaphor of picking up pennies in front of a steamroller. My policy is that if I have to force my money to work, chances are the investment decision’s risk/reward is worse than if I just held it in cash and waited for some sort of crisis to hit. I generally define “crisis” as something that will take the VIX above 30%, but it has been awhile since we last saw it:

It is pretty ironic how the election of Donald Trump was foreseen by most pundits to be the end of the world and higher volatility times, but so far the opposite has turned out to fruition. Will it continue? Who knows.

I see a lot of people making the mistake of impatience, and also the mistake of assuming that the index ETFs that they are investing into (Canadian Couch Potato, etc.) will leave them safe through masked diversification – works great as long as there are net capital inflows, but what happens if there is a correlated bust among these products? Will retail continue their conviction when they see a 10% drop in prices, or will they grit their teeth and add to their positions?

I continue to wait. It might be a very boring rest of the year with very limited writing. If you think you’re in a similar predicament, I’d love to hear your comments below.