This might sound obvious, but the most amount of income you can generate from a dollar of revenue is one dollar. Eventually taxes will kick in, and that will go down to a net profit margin of around 74%, depending on what province you live in. Then you add in expenses such as salaries, or cost of goods sold, or marketing, and that net margin goes lower. Finally, you have non-operational expenses such as financing which will bring the number even lower.

However, it all starts with revenues – if you can’t bring in anything on the top line, it is guaranteed that you won’t see anything flow to the bottom!

Which is why one of the periodic value screens I typically conduct are companies that have low price to sales ratios.

Most typically they trade that way because they are either in debt/solvency trouble, or in traditionally low margin industries (or both) – if your gross margins are 10%, you better be selling a lot of product in order to cover the other fixed expenses. It is one of the basic premises of my original CMA designation (now merged as CPA) to construct methods to judiciously track the linkage between the top line and the proper allocation of overhead expenses to different divisions.

However, if a company with relatively high top-line sales is not producing good financial results, there are value opportunities if one is lead to believe that management can tweak things to either induce higher profitability or to reduce fixed costs in a manner that will not endanger revenues. These results do not show up in historical financial statements, but when they do appear, the results can be very dramatic.

The most recent example of Francesca’s (Nasdaq: FRAN) fits the definition of dramatic:

FRAN has 3.06 million shares outstanding, so at the end of July they were about a $10 million market capitalization company. I’ll skip the bulk of their corporate history (they were one of those high-flyer retailers that caught tailwinds before they became like the next beanie baby), and their Q1-2020 result (note: their fiscal year ends January) was horrible – $87 million in sales, $9.7 million loss in operations. The trajectory looked like they were going into Chapter 11 (they did have some net cash on the balance sheet but not a ton).

Fast forward to Q2-2020, and a miracle happened – $106 million in sales, $1.4 million income from operations. The stock went haywire as you can see – especially given its low float. It’s very interesting to see when a company with 3 million shares outstanding has a day with 20 million shares traded in volume.

What’s interesting is some very smart people (or insider trading) edged the stock up a few days before the quarterly release. The day after Q2 was announced, the stock doubled and proceeded to wipe out the short sellers (on August 30, 2019 there were 1,163,624 shares that were short!).

Retail fashion is currently an industry that is getting killed because of a confluence of factors. There is the typical Amazon effect – most retailers are in malls, and malls have less traffic these days because people are discovering the experience is a pain in the ass. There are other transient factors, but in general the industry is taking it on the chin.

Reitmans (TSX: RET.A) is a good example. I can get a chart of their stock from October 2016, and place a ruler on my computer screen at a downward 30 degree slope, and it extrapolates to today.

Just because it is cheap doesn’t mean it is a good value – these cases can be classical value traps.

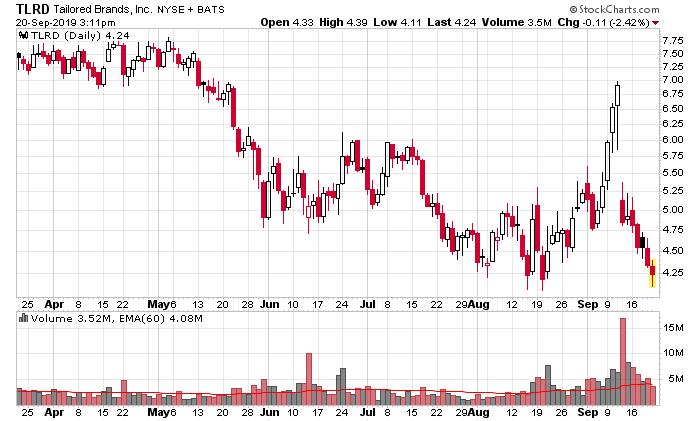

We move onto an interesting case, Tailored Brands:

Tailored Brands initially got on my radar a few months ago because it was on Michael Burry’s 13-F form. Burry is somebody that I have been aware of well before his “Big Short” days, specifically when he wrote on MSN Money at the turn of the millennium (his write-up on American Physician’s Capital was complete genius). Needless to say, I respect his thought process greatly. I was wonder what the heck he was thinking with TLRD, but I guessed the general thesis involved. He eventually explained some of his thinking in a 13-D filing indicating that he has been accumulating shares between $4.30 to $6.00.

Putting a long story short, his letter was that the company still makes money and if management believes in the business, they should scrap the dividend ($36 million a year) and instead buy back shares and increase the EPS materially.

This hype from Burry (who recently went public after a multi-year hiatus with an investment in Gamestop, another retailer, which I do not believe is a good decision because they are truly vulnerable to the Amazon effect) presumably got the short sellers in trouble (in the first week of September, there was an obvious spate of short covering – this is what happens when the stock goes up 40% in a short period of time!). Short interest is VERY high – 23.3 million shares as of August 30. The quarterly report is what got TLRD back down to earth again.

Looking at their financial statements, TLRD does look cheap from a price to sales perspective – annualizing the first 6 months, they sell $62 in revenues for every share outstanding. Operating income is still $91 million for the first half, although definitely going down.

The balance sheet isn’t great, but it is a manageable position – they have a large line of credit that extends out until April 2025 ($884 million outstanding), and a senior note ($229 million) which matures on July 2022. The senior notes trade around 99.5 cents on the dollar with a YTM of 7.2%. Right now the credit market does not look like it is locking out TLRD. Most of this debt acquired in the takeover of Joseph A. Banks (another clothing retailer) which was a total disaster. TLRD also has a large amount of lease liabilities, similar to other retailers, and more visible now due to IFRS 16.

In the last quarterly report, the company also listened to Burry and cut the dividend to zero, and made noise about buying back shares. This was actually a good sign.

When a company reduces its dividend to zero (a brave decision), in addition to the negative psychological sentiment associated with it, there is also the effect of having income funds dump the stock due to the investment policy, not to mention retail people that are deluded into believing the yield statistic they see on the stock is sustainable. There will be the technical effect of a lot of forced selling after the quarter, and I believe we are seeing it presently. The question is how many shares will get force-dumped, and when will the short sellers cover.

It is interesting how at one point the cost to short TLRD went as high as Beyond Meat for a few days – signs that borrowing is getting tougher.

Tailored Brands is mostly associated with the Men’s Warehouse brand, and in Canada it is Moore’s. The question is whether men’s fashions (suits and the like) is still subject to the Amazon steamroller. I would think this segment of retail fashion is less vulnerable than Reitman’s.

So the question is whether management is capable of clotting the bleeding. Guidance for the 3rd quarter was awful (sales down roughly 5%). Operationally management does appear to be getting into a better and more profitable niche (customization), and the question is whether they can pull it off competently.

The risks are pretty obvious. The situation can get worse. The operating income to debt ratio is quite high. Fashion is fickle, and I don’t even want to divulge on this website publicly the last time I bought a suit. That said, I think men’s fashions are less fickle than women’s, but if we get this much-anticipated recession or economic slowdown it will also not help the company’s financial fortunes – a suit is the last thing on the shopping list when one is worried about their employment (note: the Men’s Warehouse still made money during the 2008-2009 economic crisis).

That said, there was a pretty good reason why this thing was trading at $24/share a year ago. It could easily get there again – a couple quarterly reports with stabilization will do this. They set the bar very low for Q3. The CEO also put up $72k of his money into the stock after the quarterly report, which is better than nothing.

I’m buying shares in the low 4’s. It will not be a large position, but my price target is $20/share.

Normally I do not like these sorts of companies for a few reasons. One is that there are too many eyeballs tracking this, especially now that Burry has made his 13-D filing public. I am not typically a “follow Buffett” type of investor – usually when I read about something from another source, I use it as an exclusionary criterion. However, there is a good chance the market sentiment is so negative that the chances of a less negative outcome are a lot better than the consensus.

If it works out, I’ll buy a cheap suit.