With the 2024 portfolio review, the year was punctuated by making some bad investment errors. It has been a long time since I have erred in this frequency, both on the errors of commission and errors of omission. I estimate my stupidity to date this year has cost me about a +10% differential had I just stayed away from the computer in three notable instances – in other words, terrible.

To generalize some permutations of transactions where things can go wrong:

1. You get your research correct, purchase, and then the stock goes nowhere (or worse yet, down!)

2. You get your research correct, purchase, and the stock skyrockets… except your position was 0.5% of your portfolio.

3. You get your research correct, purchase, and then the story changes, you sell, and then… oops! The “story changing” part wasn’t so right after all and the stock skyrockets.

4. You get your research correct, purchase, and the stock flops regardless.

5. You get your research correct (showing the prospect is a dud), decide NOT to purchase, and the stock skyrockets anyway.

6. You get your research incorrect, purchase, and the stock correspondingly flops.

7. You get your research incorrect (showing the prospect is a dud when in reality it is great!), do NOT purchase, and the stock skyrockets.

I’ve probably missed a few in this list as continuing on is feeling quite depressing. In addition, there is the flip side of the equation when you have a position in something, and the decision to sell has similar outcomes.

While writing this out feels like re-opening old wounds, I’ll outline one example in the hopes that the pain of writing this will hopefully prevent me from pounding my head on the drywall in the future.

The topic of the day is Canadian aviation companies.

As the whole world knows, starting March 2020, shutting down borders internationally and the introduction of 14-day mandatory quarantines in hotel prisons wasn’t conducive toward the economic profitability of aviation companies. However, we managed to survive this, but all of the aviation companies were saddled with the debts associated with maintaining the fixed infrastructure costs of an airline, without the corresponding revenues for a couple years.

Warren Buffett was previously known for his comments in various annual reports about how the aviation industry was a money pit, but also got attention of people before 2020 when he took significant minority stakes in a couple major American airlines (which he subsequently dumped after Covid hit). His justification was similar to that of what had happened to the railway industry – the industry had consolidated enough that the remaining survivors could extract the economic profits out of the system. This thesis is likely a good theory, other than when there is a global pandemic going on.

We come to the story of Canadian general aviation firms (not counting niche or cargo airlines), which is dominated by two players: Air Canada (TSX: AC) and Westjet (TSX: ONEX). Air Canada, by far, is the more dominant of the two airlines, and Westjet is not an investment option simply because Onex is a huge conglomerate of other corporations which muddies the “pure play” aspect of these companies.

Lynx Air was a Canadian low cost carrier that declared bankruptcy in February 2024. As soon as this was announced, I suddenly started getting interested in Air Canada and started doing some due diligence. Putting a long story short, because capital was no longer available at zero interest rates, it became incredibly expensive (more so than before) to obtain a bunch of cheap equity and debt capital, and lease a bunch of airplanes, assemble flight crews, purchase airport space, etc., and open up a low cost carrier. The increased interest rate environment made aircraft leasing and debt capital a lot more expensive than it used to be in the zero interest rate environment model. Every incremental exit of competition in the market is a boost to pricing power of incumbent providers. Although only approximately 30% of Air Canada’s revenues were domestic, the disproportionate increase in profitability the airline would have in being able to raise fares would result in a subsequent increase in profitability.

In addition, the historical financial statements of Air Canada at that time showed reasonable amounts of cash flow collections, and the mountain of debt they incurred during the Covid shutdown was being whittled away.

So after reading the annual report, and after the first quarterly report, I decided to dip my toes into the stock and take a position. My theory was that at their rate of cash flow generation, coupled with a boost in profitability, would come an enterprise value matching something around the pre-Covid levels (noting that AC had about 280 million shares outstanding in 2019 while today they have around 370 million).

We fast forward to July 22, 2024 when the company issues a pre-second quarter press release, generally guiding metrics downward. The release stated, “The updated 2024 adjusted EBITDA guidance range is largely driven by the lower yield environment, lower-than-expected load factors for the second half of the year and competitive pressures in international markets.”

“Competitive pressures” are two words that I did not want to be reading. “Lower yield environment” is another consequence of competitive pressures.

My thesis was toast, so I bailed out of the stock quite quickly. The fact that it was a pre-release of their actual quarterly earnings report (which came out August 7, 2024) did not help either.

We fast forward a little bit and the news concerning the looming pilot strike also took the stock down further. An airline without pilots does not function very well (although the conflict in Russia-Ukraine has shown that unpiloted devices are indeed showing that piloted aircraft are about as obsolete as battleships were in World War 2!).

However, Air Canada and the pilot union settled with a massive pay increase and they announced the third quarter result and the stock was off to the races. Even more insulting was that they announced that they finally were able to deploy some capital back to shareholders and launched a massive share buyback program – from November 5, 2024 Air Canada has been repurchasing about half a million shares a day (about $12 million dollars a day) into the open market and needless to say that puts a lot of bidding pressure on the price!

I totally missed the boat on that one. At the end, I suspect that the second quarter pre-release was a ploy for negotiation purposes with the pilot union. Had I stuck on, this particular position would have been a +50% gainer. Yuck.

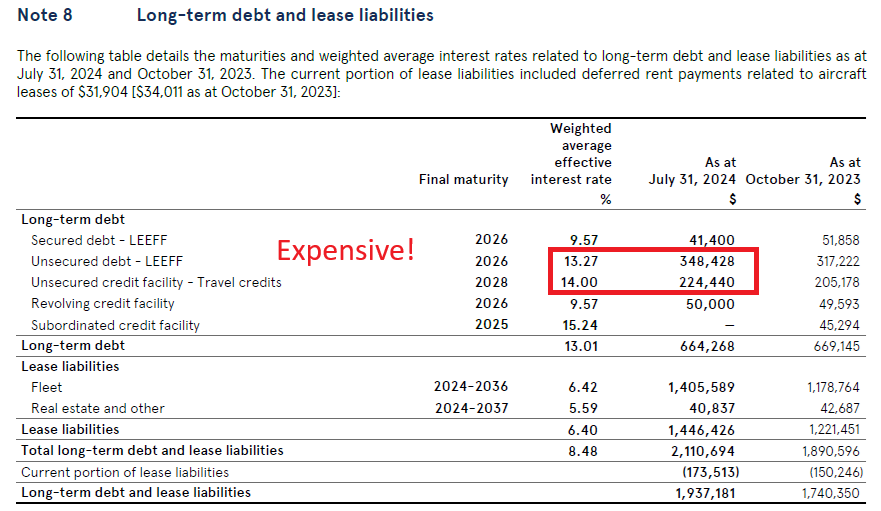

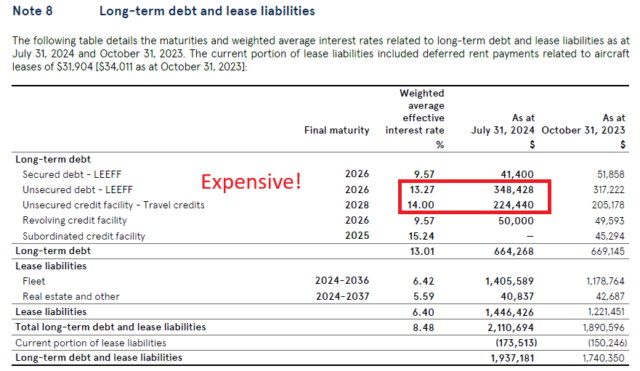

The “revenge trade” is looking at something else in the sector and the only entity that warranted my examination was another competitive airline, Air Transat – (TSX: TRZ). Unfortunately for them, they look financially wrecked. Before Covid, they had a modest amount of debt in relation to their operational cash flows, but after Covid-19 they were forced to take on too much debt and this is what is going to sink them.

It is difficult to come up with a ‘normalized’ earnings or free cash flow rate for the company because its historical performance has been quite spotty, but suffice to say the sheer quantity and expensive of their debt portfolio is going to be too much for them to overcome. My rule of thumb is to exercise exceptional caution when companies have material amounts of their debt priced at a coupon higher than 10%, and indeed in this case having $670 million of your own debt at around 14% is very difficult to recover in a price-competitive industry with relatively low margins. This is a fancy way of saying that although TRZ stock is trading at all-time lows, I can’t see how they recover from this without a recapitalization.

I also note that American Airlines (AAL, UAL, etc.) have all had insane recoveries – I think the Buffett thesis on this industry has some merit and although there will be more competition with airlines than in railroads, the consolidation will likely result in some sort of equilibrium where the big incumbent players will consistently be profitable.

Finally a footnote – although I have made significant mistakes this year, there have been a few prominent publicly traded entities that have blown up that I have managed to simply not be in at the “right” time. I have written before about Slate Office REIT’s debentures, where I managed to exit in the 90’s (currently trading in the 40’s) after coming to the conclusion that a minority holder cannot win; and there have been a couple others which I have eyeballed but explicitly have not taken positions in, and only to see them tank. During this USA Thanksgiving weekend, it is something I can be thankful for. Although I am underperforming the S&P 500 (I seem to be the only person on the planet not owning NVDA, TSLA or MSTR stock!), the differential is not too wide. However, if I did not make mistakes like I did with Air Canada, I could be outperforming the index despite the portfolio being de-risked with a significant cash holding!