Brexit – Impact

Market volatility has been high leading up to and including after the Brexit referendum results. The VIX has climbed up to around the 25 level which is above the average ambient temperature of 15, but not ridiculously high (last August, for example, there was a spike up to 50 and I’m struggling to remember what calamity was the order of that day).

The UK exiting from the EU causes uncertainty in the minds of money managers. Whenever uncertainty is high, the natural desire is to raise cash and reduce portfolio risk, so futures get sold. This triggers automatic liquidations of underlying equities and debt portfolios, which leads to broad-based asset price decreases as the liquidations occur. There also may be some margin liquidation going on for more over-leveraged players.

Eventually this vicious cycle ends – the trick is anticipating when the vicious cycle ends. I believe it will be sooner than later, although the choppyness of the market will continue to confuse most market participants into believing that we are either entering into the new dark ages, or a golden era of economic productivity when neither seems to be the case.

Canadian Preferred Share price appreciation nearly done

Preferred share spreads (in relation to government) have compressed significantly since last February and it appears that the macro side of the preferred share market has mostly normalized and accounted for the incredible drop of dividends on the 5-year rate reset shares due to the 5-year government bond rate plummeting (0.62% at present with short-term interest rate futures not projecting rate increases until at least 2018).

We are still seeing significant dividend decreases as rates continue to be reset.

I have looked at the universe of Canadian preferred shares (Scotiabank produces a relatively good automated screen) and further appreciation in capital is likely to be achieved through credit improvement (e.g. speculation that Bombardier will actually be able to generate cash indefinitely) concerns rather than overall compression in yields.

As such, one should most certainly not extrapolate the previous three months of performance into the future. Future returns are likely to primarily consist of yields as opposed to capital appreciation.

While investment in preferred shares, in most cases, is better than holding zero-yielding cash (in addition to dividends being tax-preferred), one can also speculate whether there will be some sort of credit crisis in the intermediate future that would cause yield spreads to widen again. If your financial crystal ball is able to give you such dates, you can continue picking up your quarterly dividends in front of the steamroller, but inevitably there will always be times where it is better to cash out and then re-invest when everything is trading at a (1%, 2%, 3%, etc.) higher yield.

I am also finding the same slim pickings in the Canadian debenture marketplace.

Valuations have turned into such that while I’m not rapidly hitting the sell button, I’m not adding anything either and will continue to collect cash yields until such a time one can re-deploy capital at a proper risk/reward ratio. If I do see continued compression on yields I will be much more prone to start raising significant fractions of cash again. Things are very different in 2016 compared to 2015 in this respect – in 2015 I averaged about 40% cash, while in 2016 I have deployed most of it.

Small re-inspection of Bombardier

The on-again, off-again rumours regarding a billion-dollar injection with the Canadian government is purely negotiation strategies on both parts. The government wants to invest, but they also want to do it in a manner that allows them to save face. Conversely, the controlling shareholders of Bombardier want the money (it will indirectly end up in their pockets), but they also do not want to lose control over the gravy machine.

There will be a happy equilibrium where the taxpayers of Canada will transfer wealth to the owners of Bombardier, but the structure of the arrangement is up for debate. My suspicion is that some sort of arrangement will be made as long as they keep a certain number of jobs in Quebec, the Class A share owners will not be compelled to convert into Class B shares.

The credit market has been much more kinder to Bombardier, to the point where they can raise capital at a very reasonable rate:

The Class B equity has been hovering at $2/share, with the control premium (Class A shares) being around 10% of late.

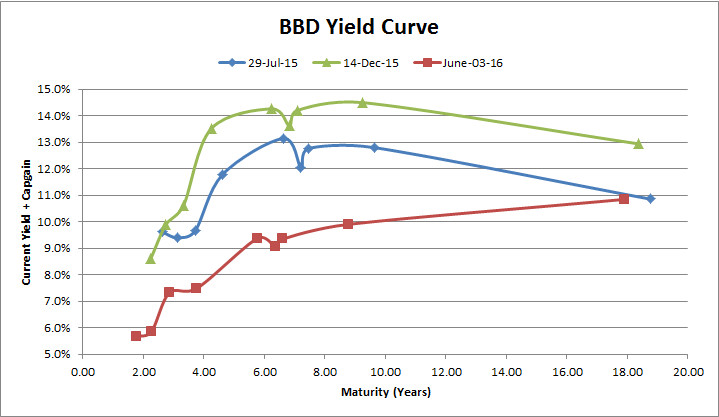

Floating rate preferred shares (TSX: BBD.PR.B) has been hovering around 8.4% yield, while fixed-rate with conversion risk (TSX: BBD.PR.C) has been hovering around 9.9% of late.

As I alluded to earlier, investors must make a distinction between revenues and profit, and Bombardier is focussed on revenues at the moment. They will continue to service their debt and preferred shareholders, but I do not believe equity holders will be receiving dividends anytime soon. There is also a significant overhang with the two Quebec deals, with a significant number of warrants outstanding at US$1.66 level – although these warrants are held by institutional owners (Quebec), this will be a valuation overhang which will serve to depress the maximum upside of the common shares. If it ever gets to the point where these warrants are exercised, it would buffer the serviceability of debt and preferred share dividends.

I am of the general belief that if Bombardier plods along and returns to a profitability at a level that is somewhat less than what they have touted in their 2020 vision, and that their C-series jet clearly has a “runway” of perpetual orders keeping the assembly lines busy, that BBD.PR.C would trade around the 8% level (or roughly $19.50/share). The credit markets are indeed pointing toward this direction.

Now the corporation just has to make money.

I am still long their preferred shares, but under the belief that a good quantity of upside has been realized by investors in relation to previous trading prices. I went long on preferred shares less than a year ago when there was a lot more gloom and doom, and having been called a “brave soul” by national media for doing so.

The very strange dawn of robotic marketing

This post is more of an experiment than anything from reading James Hymas’ May 25, 2016 post. A successful result will be me being sent a spam email by a robot. This is probably one of the most rarest times where receiving spam is a positive result!

On May 19, 2016, IGM Financial invested $50 million in Personal Capital, which is a robo-investing corporation.

Just so there is some information content in this post, there is clearly a scale where passive investing will deliver inferior absolute returns in relation to active managers. Although I have not done the detailed analysis (in terms of obtaining reasonable data in terms of capital flows and such), I would suspect we have already reached this point. Too much capital that is attracted to the main equities (TSX 60 and the like) will likely result in under-valuations in less liquid portions of the market – especially when there are market corrections and robotic investors decide to liquidate “roboticly” – i.e. without regard to price.