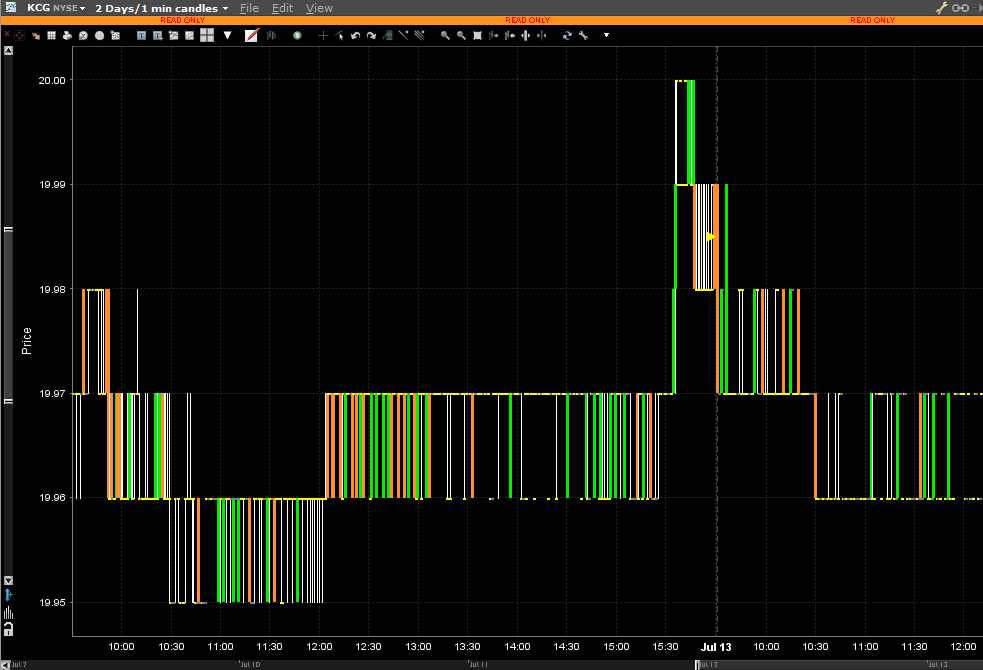

KCG Holdings (KCG) is due to be bought out by VIRT for $20/share cash. The meeting for KCG shareholders to approve is on July 19 (which at this point is practically a done deal). Over the past two days we had the following trading:

See that spike up to $20/share at the end of yesterday’s trading? I wasn’t expecting that! It is not financially rational to purchase shares at $20 unless if you believe there will be a higher bid for the company. At this point, however, a successor bid is simply not going to be happening.

A more reasonable $19.98/share means a 2 cent premium obtained over a week, which works out to about a 5.2% simple interest rate, assuming no trading costs.

I had some July call options so I figured it was a good time to dump the remainder of my shares into the market. There was a legal complication from one of the class action lawsuits that might require the company to obtain a 2/3rds shareholder vote of all non-insider owned shares and considering the general apathy of voters these days, that is not a threshold that I would want to bet my kidneys over.

Once the merger is completed then KCG’s senior secured bonds will be called away (at 103.7 cents on the dollar, while my purchases were a shade above 90 cents) and that will conclude one of the better investments I’ve made over the past 5 years. It took a lot longer to happen than I anticipated – had it occurred at select points over the past 5 years I had even higher amounts of leveraged option positions on this company (which sadly expired).

One thing I will miss about these bonds is that the 6.875% coupon I was earning was virtually guaranteed money to maturity. I will no longer see that.

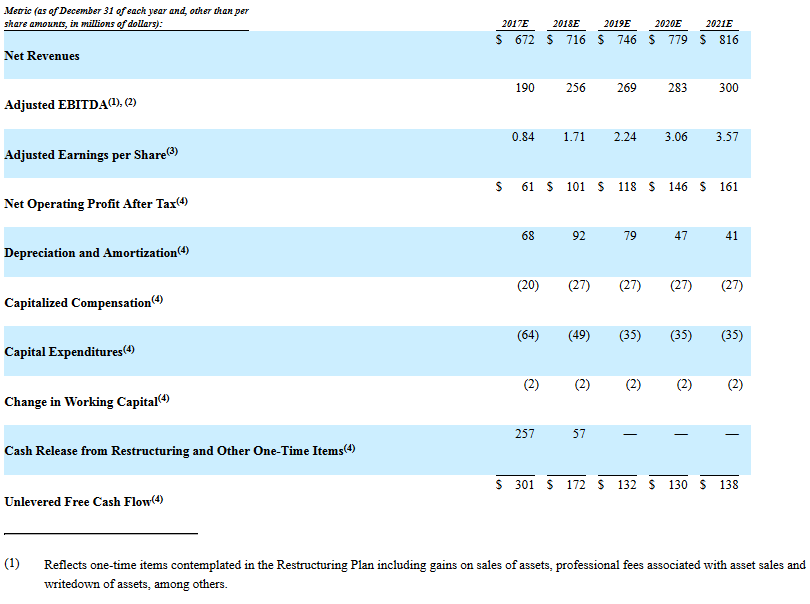

The analysis for VIRT is a little more muddy – I expect some serious integration pain to occur after the merger is finished. In the definitive proxy statement materials, however, I was very intrigued by the following table which illustrated the financial projections of a management restructuring:

So in the above, we had management projecting a 2019 estimated free cash flow of $132 million, which appeared to be sustaining for future years. This worked out to about $2 per KCG share, which VIRT is now purchasing for 10 times earnings.

Management projections are always on the optimistic end of things, so this is not likely to materialize as presented, but it still makes one wonder whether VIRT is worth investing in or not. I do not like their corporate structure (public shareholders have no control over the company and a vast minority of the economic stake of the firm) and I am inclined against it.