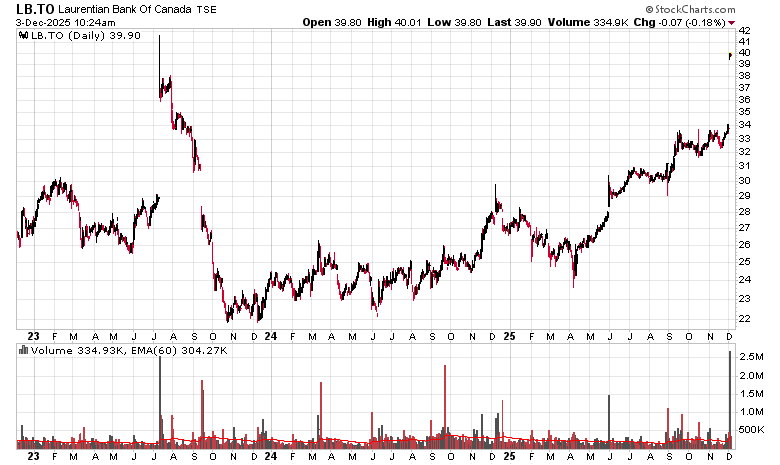

Laurentian Bank (TSX: LB) finally found its solution to its years-long strategic review and found a way to carve itself out to various suitors, leading to a CAD$40/share cash buyout offer. The three year history of the stock graph pretty much tells the story – with the prior outsider CEO in 2023 getting fired for not being able to sell the company, and new management being successful:

I was contemplating taking a relatively mid-sized position in LB around $25-ish early this year but simply didn’t. Even worse yet, I had a tiny position (a fraction of a percent) in late 2024 but cleared it out in early 2025 to just simplify my portfolio and reduce the number of names that sucked up my attention. It’s one more illustration (more like a financial slap in the face) of how 2025, despite the major indexes posting somewhere around a +20% year, has been quite sub-par for my own personal decision-making, which is shaping up to be my worst relative performance since 2014.

Going back to LB, this pretty much eliminates the “pure banks” out there, albeit LB was a very small fish in a large ocean and also Quebec-centric. We have the following banks remaining on the TSX with a market capitalization of over a billion dollars, and needless to say, they are names that you’d all recognize, in order from largest to smallest market capitalization as of 31-Oct-2025, and I will also post the approximate YTD performance (NOTE: CAGR over the past 0.9 years) and market cap as of the writing of this post:

RY (+28%, 304B)

TD (+60%!!!, 200B)

BMO (+31%, 126B)

BNS (+32%, 121B)

CM (+36%, 112B)

NA (+30%, 66B)

LB (+45%, 2B)

There’s pretty slim pickings when it comes to publicly traded Canadian Schedule 1 banks out there. They have all done pretty well this year. The only notable valuation nook was when CM was trading around book value earlier this year. Indeed, banking world-wide has done very well as interest rates have dropped – many of the European Banks have posted triple-digit percentage returns (e.g. DB is up +115%, etc.).

With Canadian Western Bank (CWB) being picked up by National Bank a little while back, this leaves the “sub-bank” companies, such as Equitable (EQB) and the like being potentially picked off – notably Equitable is one of the few that are down year-to-date, presumptively due to its exposure to less than ideal real estate financing assets. This is also likely why he largest residential REIT trading in Canada (CAR.un) is also down YTD.

If I were to describe my investment tone at the moment, it is quite restless. High valuations do not make for high returns, and with credit seemingly plentiful and corporate debt yields relatively tight to risk-free rates, it has been a struggle to find value. Indeed, holding a grenade like Ag Growth (AFN) has not been a particularly thrilling experience although thankfully I lightened out of that one in 2023 when things were a bit more optimistic there.

I do intend to continue my Late Night Finance episodes, but only when I have something meaningful to contribute. In our make-belief world of generative AI, it is difficult to compete – I do not know whether I am adding more to the slop or whether what I am contributing is signal. Based off of my performance as of the past couple years – it seems to be noise.

The good news – past successes or failures do not have to equate to future successes or failures – each decision can be considered afresh.

Feels like NA and this private company are getting a hell of a deal.

More bank/finance consolidation – EQB taking over Loblaw’s PC Bank:

EQB will acquire PC Financial for 1.15x book value at closing, excluding excess capital above a 13% CET1 ratio, for consideration estimated at $800 million, subject to adjustment pursuant to the terms of the Transaction Agreement. The consideration will be satisfied by the issuance to one or more subsidiaries of Loblaw of 7.2 million common shares of EQB, representing approximately 16% of EQB’s issued and outstanding common shares as at the date hereof on a pro-forma basis, and the remainder in cash. In addition, prior to the closing of the transaction and subject to regulatory approval, Loblaw will release and receive approximately $500 million of excess capital and other value from PC Bank, for estimated total value of $1.3 billion to Loblaw. Pursuant to and subject to the terms of the Transaction Agreement, Loblaw will own a minimum of 17% of EQB’s issued and outstanding common shares on closing of the Acquisition. Closing is expected to occur within calendar 2026, subject to customary closing conditions and regulatory approvals.