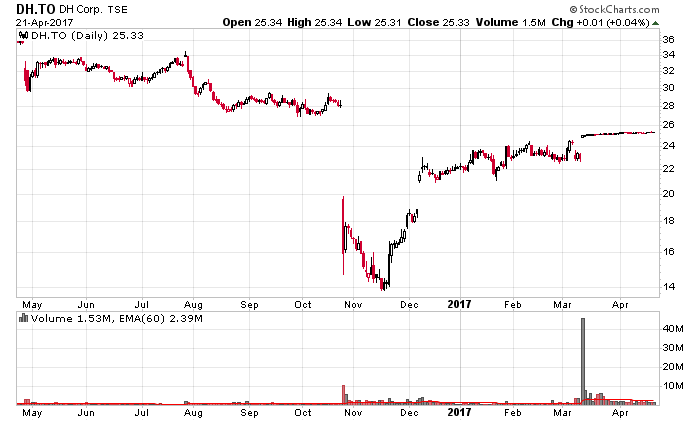

I’ve written a little bit about D+H Corporation (TSX: DH) in the past. On March 13, 2017 they received an all-cash buyout offer for CAD$25.50 from an international firm and there is no reason to believe this will fail.

In my opinion, DH shareholders are getting a good deal since there are plenty of storm clouds on the horizon for the company.

However, there is a lesson for me in this story even though the last time I owned shares was in 2010.

Back in October 2016 when they released their disaster of a quarterly earnings report, their stock subsequently traded as low as CAD$14.06, although realistically if you had started accumulating after their earnings disaster you would have received an average price of around CAD$15/share. I also predicted the company would slash its dividend in half (which it nearly did, from 32 cents to 12 cents a quarter) and thought the stock would get hit even further as I projected a spiral of selling by panicked investors.

This did not happen. Instead, when they announced their dividend slashing, the stock quickly went up to $16 and never looked back. The company announced a strategic review to sell out the firm on December 7, 2016 which sent the stock up to $21/share and you can see the rest of the story in the stock graph.

So in the span of six months between an earnings disaster and the buyout offer, the company’s stock price has appreciated by a factor of 70%.

In retrospect, the October quarterly report and subsequent dive in stock price (from $28.70 to $16.20) should have been an equity purchasing event, not an event to continue throwing eggs and rotten tomatoes at the corporate body.

It makes me wonder about my valuation methods and why I got this one incorrect.

I wasn’t in a very good position to invest back in October 2016 (I was mildly leveraged at the time), but even if I was in more of a cash situation I probably wouldn’t have dipped my toes until around CAD$12/share where I would have seen an acceptable risk/reward ratio.

I have performed equity and debt research on hundreds of companies. Some companies I keep current on even though I have not taken a position on them. Some companies I just look at once and don’t look at them again until years later when there is some reason for them to show up on my radar again. There are also some like D+H that I have invested in a long time ago and check in from time to time. Whenever companies like these appear again, there is always the knowledge that I have done my due diligence over a larger period of the company’s history compared to those that are freshly looking at the company. In the case of D+H, it will be sad to see this accumulated research knowledge go away, but that is life as an investor in publicly traded securities.