Most of us know about the Yellow Pages – it was the old phone book directory that had listings of various businesses by category. I have written about this company before in the past, but the last article was back in 2012! I still have kept track, however.

This post is less about raw financial analysis and more of what appears to be an operational turnaround story.

Yellow Pages’ history

Historically, it used to be fully owned by Bell Canada (TSX: BCE), but was later partially sold off to the Ontario Teacher’s Pension Plan and KKR (NYSE: KKR). In August 2003 Yellow Pages finally went public as an income trust. The last bit of incumbent ownership was sold off in June 2004, at a valuation of $3.7 billion (at an enterprise value of $4.7 billion – an extra $1 billion of net debt on its balance sheet at the end of 2004). 2004 was a good year, they made about $320 million in cash flow, and distributed most of it to unitholders. In case if anybody cared, their units were initially sold to the public for about $11/unit and they gave out a monthly distribution of 7.33 cents per unit (88 cents annualized).

KKR are not dummies, however, and knew the gig was going to be up soon – that’s why they got out of the game. This thing called the internet came along with search engines, and that proceeded to completely destroy the print directory business. Most print media companies got completely killed as a result, and that included Yellow Pages.

Recapitalization and subsequent financial falling out

We fast forward to the end of 2011, when Yellow Pages converted to a corporate structure, and the full weight of its $1.8 billion in debt (plus preferred share obligations) eventually caught up to the company when it floated a recapitalization proposal in July 2012, which was eventually adopted with some modifications to placate some debtholders (December 2012). Everybody along the capital structure took a bath (especially common shareholders), and left the entity with $750 million in senior secured debt (9.25% coupon), and $107.5 million in convertible debt, trading today as (TSX: YPG.DB) (8% coupon, due November 2022, $19.04 conversion price).

Keep in mind the number of the $750 million senior secured debt issued in late 2012 – it contained covenants that required mandatory cash redemptions, including the restriction on paying dividends.

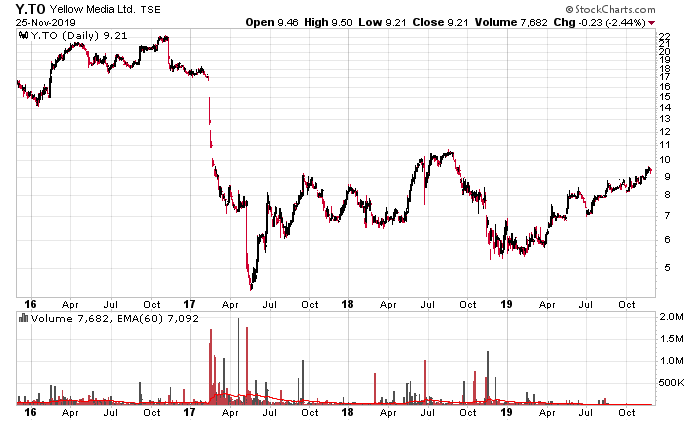

After the 2012 recapitalization, the company meandered into trying to make a living in a digital universe. For the most part, they tried to experiment with digital acquisitions and conversion of its customer base into buying digital products, which had limited pockets of success here and there, but by no means close to achieving the raw cash flow of the prior glory era. The debt loomed over them like a vulture ready to eat the remaining scrap of meat on the carcass, and by the time the 2016 year-end results came in, it was looking pretty ugly (noting the 50% drop in stock price after the release of their Q4-2016 results in February 2017):

More recent financial history

From the end of 2015 to 2016, the cash flow from operations minus capital expenditures went from $191 million to $145 million. Management had blown in those two years $206 million on acquiring other businesses and intangibles without materially contributing anything to the bottom line. The senior secured debt balance went from $407 million to $310 million, but the maturity date of November 2018 loomed and they would need refinancing since there was no way to generate enough cash to pay them down at maturity.

New management takes over

After the recapitalization, Yellow Pages had a few significant shareholders and they decided to take action. This started by removing the existing management (July 2017) and the installation of current management, the current CEO David Eckert (September 2017). Since Eckert has been in control, Yellow has divested most of its other business divisions, cut costs and locations, and has had a laser-like focus on engaging in profitable business, rather than revenue-focussed business.

One of the first major financial decisions made was to refinance the senior secured debt (October 2017) which they received a very unfavourable price (98 cents on the dollar WITH a 10% coupon!), but this allowed them to extend their maturity profile until November 2022. I remember taking a look at the company at this time and said to myself “good luck”.

2017’s financial results (most of which can be attributed to previous management) were pretty disastrous, with about $48 million in free cash generated ($85 million in operating cash flow minus capital expenditures, and another $37 million spent on intangible assets). Even worse yet, the company still had the senior secured debt hanging like an anchor on its neck, accumulating even higher amounts of interest payments.

Then came a wave of cost cutting. From an abstract operational level, implementing cost cutting in a corporate environment is never easy – it is very easy to trim the proverbial bone along with the fat. Closing down facilities and laying off people causes morale problems within organizations and never makes those subject to the downsizing happy. But current management appears to have done a very good job identifying where the fat was.

Management has been very good at providing colour commentary in their conference calls. From Q1-2019 (underlined emphasis mine):

Look, this is David. Let me first try to answer a bit and then I think, Franco, will probably come in as the cleanup batter here on this one. We have constantly looked at every dollar that we spend, and we don’t differentiate between above the line above, below the line, operating or capital or anything. And continue to — and I know all management team say they scrutinize their spending, but we’re really serious about it, and we really have cut a lot. And let me just give you a couple of examples, on a consolidated basis, we used to have many thousands of employees, now we’re less than 1,000 on a consolidated basis. The real estate footprint that we use, when we started, what was about 1.5 year ago, depending on how you count, we occupied between 28 and 35 different locations in North America, almost all of them in Canada, a little bit United States at the time. So depends on how you count, and again, this is consolidated. Now we operate 3 plus a little 1, 3 — so call it, kind of, 3 and a little — 3.1 locations. And the amount of square feet that we operated in — at the beginning of that period of time, which was late in 2017, now compared to that is down by slightly more than 3/4. So we have slightly less than 1/4 the amount of square feet. Those are — I love getting rid of spending that’s like leases, the rent and things like that because those actions in no way harm anything that matters. A square foot of real estate never sold a single dollar of revenue and never made a single one of our customers delighted. So those are just examples of some changes that are large and dramatic in just the last 5 quarters that are still showing up newly, certainly, in this first quarter and that have propelled us to not only really good EBITDA and really good EBITDA minus CapEx, but I think pretty huge cash generation and the ability to paydown whether you look at net debt or whether you look at the $90 million of debt payments we’re going to make in the next 30 days or the $120 million that Franco just said we expect to make during the calendar year. So it’s a lot of things, it’s all over the place and it’s in particular with a focus to not having negative effect on our customers or our revenue.

In January 2018, they announced a streamlining of 500 employees from their workforce. (April 2018) The board of directors was reduced from 12 to 7. They also divested a whole variety of non-core businesses: (Western Media Group, and Totem, May 2018), (ComFree/DuProprio, July 2018), Red Flag Deals (August 2018), (Mediative/JUICE January 2019/December 2018), YP Dine/Bookenda (April 2019). When examining financial results, it does not appear that these businesses contributed materially to the profitability of Yellow Pages.

But perhaps more interesting was the decision to engage in a collective bargaining agreement modification with their unionized salesforce (September 2018 – lockout, November 2018 – settlement), which, according to conference call transcripts, will now allow management to incentivize employees in a manner that is aligned with the profitability of the business. This decision (never easy to be the one doing the locking out) probably provided negotiation leverage with the rest of the unionized employees in the rest of the corporation, which was all settled in January 2019.

Elements of a turnaround

Fiscal 2018 featured $118 million in free cash flow ($135 million minus intangibles, and PP&E), and a reduction in senior secured debt to $170 million. Compared to the ~$50 million performance of 2017, this was a considerable increase in cash that went directly to debt repayment. The EBITDA margins shifted from 25% to 33% in 2018, which is not a result that one would expect without knowing the underlying reasons for it (cutting unprofitable revenues). Correspondingly, the customer count also dropped from 227,300 to 186,700 (-18%) and revenues also took a nosedive from $728 million to $577 million (-21%). In the first three quarters of 2019, despite the revenues being 32% below 2018’s results, EBITDA minus capital expenditures was down 15%.

A business can’t last very long if they keep losing 32% or 21% of their revenues in a year, which is why in 2019, the focus of management has shifted from cost containment and enabling a structure where they can incentivize employees to sell profitable business and to “bend the revenue curve”, which the modification to the collective bargaining agreement will be correlated to.

The results on cost containment in 2019 have been pretty dramatic. On December 2, Yellow Pages will repay the remainder of their senior secured debt, which is quite the accomplishment since in 2017 the trajectory (in my books, and probably theirs as well) had the company going into another recapitalization. This also means that the strangehold on the company with the financial covenants associated with the debt are gone, in addition to the 10% interest rate payable. This opens up the door for capital allocation decisions if management desires, although their track history strongly suggests they are intent on eliminating the debt entirely.

In Q3-2019, the company ended with $94.9 million in cash, and in Q4-2019 has retired the remaining $80.2 million in senior secured notes. Assuming a positive cash inflow of about $25 million in Q4, this will leave the balance sheet with about $40 million in cash and on the opposite side the convertible debentures, of which $107 million is outstanding. There is little doubt now that Yellow Pages will generate enough cash to handle these debentures. The debentures are callable today at 110% of par, or at par after May 31, 2021, so it is unlikely management will call them with the 10% payment penalty (very expensive capital – might as well do an SIB at 103 on the dollar). Rather the question is going to be how much money the company will be able to make before the cash generation and revenues stabilize, and heaven forbid, grow.

The thesis here is pretty simple. The stock trades very low because everybody thinks Yellow Pages is a 20th century company that is roadkill of the internet, and trades as a non-going concern. Almost everybody that I mentioned this company to just gives me a puzzled look like I’m insane and moves on. The sentiment is Yellow Pages is dead! A lot of people got burnt on them when they were an income trust more than a decade ago. They look at the revenue curve and just make the automatic assumption it’s going to end up like a newspaper company. It doesn’t take much to assume a perpetual 15% revenue decline and come up with a valuation for the residual equity in the company. The old business model might be dead, but not the new one.

Since Eckert took over, it is pretty clear that the terminal value of the company when modeled in such a manner is going to be higher than zero. Such a theoretical terminal value is probably around to what the stock is trading at currently – higher single digits, say $7 or so.

The upside scenario, however, is if management can be as competent in stabilizing revenues as they have been in cutting costs. If this occurs, Yellow Pages is dramatically undervalued. The question is when this will occur – will it eventually stabilize at $10 million a quarter? $5 million? Zero? Or 20? Keep in mind that in the first three quarters of 2019, Yellow generated $105 million in cash, net of capital expenditures. This is a ton of cash flow for an apparently dead business.

A simple scenario is if they’re able to stabilize cash flows to $15 million a quarter, which is less than half of what they’re doing presently. $60 million of cash generation is $2.14/share – if stable enough, this will produce a market multiple of at least 8, and probably 10. In the dream scenario of management being able to clot the bleeding earlier than later, and then get back onto a growth trajectory, there will be a considerable multiple applied to the stock price when everybody tunes back into the company again.

The business

Aside from the traditional print directory business (which they have monopolistic rights until at least 2031 with Telus and 2032 with Bell) where they have an obvious but diminishing competitive advantage (by virtue of being the only game in town in a rapidly declining market), the other (currently 75% and increasing) component to the business is essentially functioning as a digital advertising provider. This includes (from their 2018 AIF): content syndication, search engine solutions, website fulfillment, social media campaign management, digital display advertising, video production as well as print advertising. While in itself this is not a market they have an organic competitive advantage in, the primary competitive advantage they continue to have is their database of customers which provides incumbency advantages. This advantage is weakening.

Ownership structure and stock trading

Presently, there are three major shareholders in Yellow Pages. GoldenTree Asset Management owns 30% of the equity, and they have owned it for a considerable period of time. Canso Investment Counsel owns 26% of the equity, and approximately $39.5 million in convertible debentures (and they used to own $136.5 million of the $315 million 10% senior secured debt before this was paid off). At the beginning of 2018, Canso owned about 27.5% of the equity and they sold off about 1.5% in 2018. Finally, Empyrean Capital Partners owns 18% of the equity and about $1 million in convertible debentures – they disclosed a 10% stake in April 2018. Combined, these three shareholders own 74% of the company, leaving about 7.3 million shares freely trading for the public. This is a very small float, and typical trading is about 5,000 shares a day.

The company used to have a fairly large short interest, but this has diminished throughout 2019. It used to be the case where the borrow rate was over 20%, but sadly now that rate has dropped into the mid single digit percent. The short sellers have more or less closed their bets on this one.

The concentrated shareholder structure creates a proposition where it might be more convenient for these insiders to either propose a going-private transaction (likely with some inside knowledge that the revenue curve is bending), or to sell the entire company as some strategic acquisition (mainly the 162,000 customers left on the books is not an inconsiderable intangible asset to be acquired by another business that would be able to monetize it more efficiently than Yellow). The other option they have for liquidation is for the company to announce a substantial issuer bid for the equity if it is still undervalued. In either case, it would involve upside from current equity prices.

Downside risks

It could be that the revenue decline is impossible to stem or will exhibit an unacceptable erosion of profitability. In that case the thesis is dead, but given the payment of the senior secured debt, the equity downside is much more muted than it was five years ago.

Another concern is the state of the defined benefit pension liability – about $130 million at the end of Q3-2019. The pension ended with $444 million of assets at the end of 2018 and estimated obligations of $543 million. At some point in the future, this will have to be paid, but noting that the assumed discount rate for the plan is 3.8%, which should hopefully be eclipsed.

The business is also subject to the usual macroeconomic risks associated with advertising agencies – if businesses stop making money, ad budgets typically shrink and competitive pressures increase. This isn’t an exclusive risk to Yellow Pages, but given the long-in-the-tooth nature of this economic expansion cycle, is worth mentioning.

Price target scenario

In a revenue stabilization scenario the stock probably will trade in the $20s again. This would also imply that the convertible debentures would be converted into equity at $19.04/share sometime between now and maturity. Multiples will most certainly rise from the current 1.5x TTM EBITDA figure (or about 2.1x TTM EBITDA on enterprise value).

In relation to the potential reward to risk ratio, I believe the ratio is high potential reward to medium risk at present prices.

Conclusions

Everybody was waiting for Nortel to rise back from the ashes again. Perhaps they were looking at the wrong company and should have considered Yellow Pages. Time will tell.

Disclosure: I took a position earlier this year. Initially I started in March 2019, from $5.78/share, and adding upwards to $9 as I have gained confidence from their quarterly reporting. After Q3-2019, the stock still appears cheap, but clearly not the no-brainer it appeared to be when it was still in the $6-7 level. The stock is thinly traded and it doesn’t take a lot of action to move the stock price. It is my highest weighted position presently. I’m also going to give a hat tip to Mispriced Markets, who seems to be the only other person I know of that has written substantive thoughts on this matter – he wrote about it on October 2019.