More completely random ramblings, and even less marketable commentary:

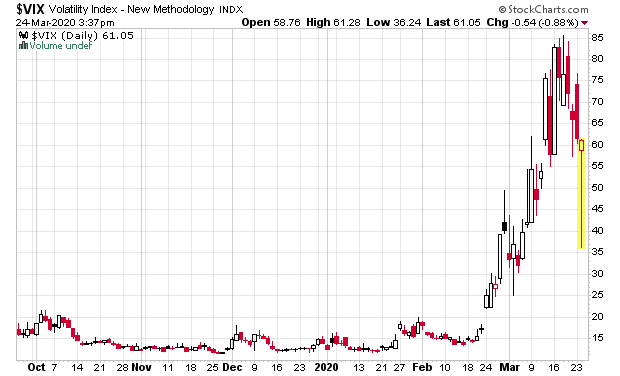

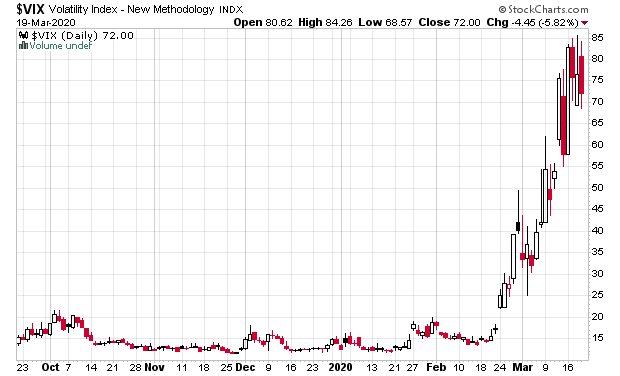

VIX has been above the global financial crisis 2008-2009 levels:

Are the “short volatility” funds going to re-enter the market at this point?

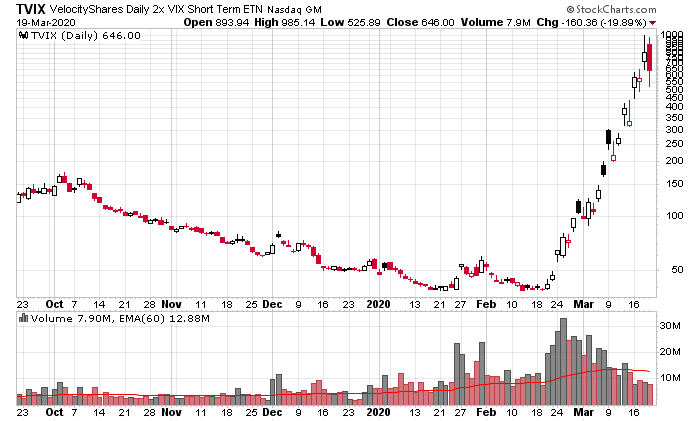

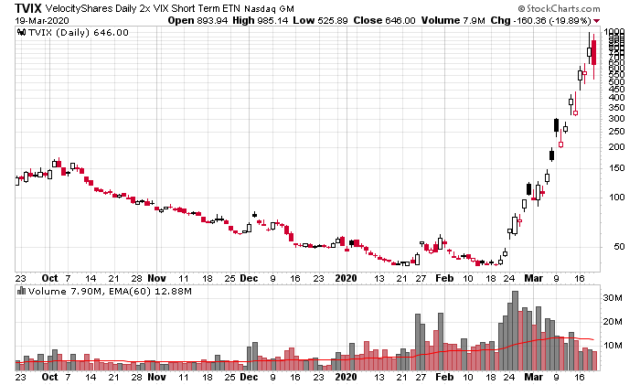

In particular, the leveraged ETF that I use to examine volatility, TVIX, had a massive spike up before subsiding:

Opened at 892, topped out at 985, closed at 646… my god! Trading or gambling at this point?

Option expiration this Friday – I’d think most of the specialists have already hedged off risk, but there are usually games played on the last day of options trading which cause volatility. Put sellers are going to be assigned.

Although pension funds are the last thing that are on people’s minds right now, companies with large defined benefit pension liabilities are going to be facing a haircut of about 15-20% if they are a typical 60-40 equity-bond split. Guess what? You’re on the hook as well since the government has plenty of people on its pension payrolls! Here in British Columbia the public service pension plan is decently managed, but in other less credible jurisdictions, they’re going to have to face the difficult decision – reduce benefits, or force existing workers to contribute more… a lot more. Companies with defined pension benefit plans will also have to make up the shortfall.

The impact on lease defaults is just going to start. Pretty much most companies with IFRS 16 “right of use assets” are sitting on a big fat zero, while maintaining the liability of lease payments. This is not going to end up well for a lot of REITs. Taking a look at Tailored Brands (TLRD), the operators of Moore’s (Canada) and the Men’s Warehouse, for example, in their last 8-K today stated:

On March 17, 2020, the Company issued a press release announcing that in response to the coronavirus and to protect the health and safety of its customers, employees and the communities in which it serves, the Company will temporarily close its retail locations in the U.S. and Canada starting Tuesday, March 17, 2020 through Saturday, March 28, 2020.

On March 19, 2020, the Company issued a press release announcing that in light of evolving government and citizen response to the coronavirus outbreak, it will, out of an abundance of caution and concern for its employees, close its e-commerce fulfillment centers starting Friday, March 20, 2020 through at least Saturday, March 28, 2020, and will suspend the currently limited operations in its retail stores during this period.

This is a big fat zero for at least 10 days of business. Mind you, buying a suit is the last thing that you’d want to do at this moment (so effectively it doesn’t matter whether you actually keep the lights on or not) but the counterparty, the landlord, is going to start feeling a bit of tension, especially when these companies are so close to the brink of wanting to just Chapter 11 themselves out of these agreements. This also explains why companies max out their revolving credit facilities – it is usually the first step before you do a Chapter 11 filing. You want to have enough cash to actually keep things going, otherwise DIP lending at this time is going to be ridiculously expensive.

Even Obsidian Energy (TSX: OBE) managed to get out of massive lease payments in Penn West Center in Calgary – I guess that’s going to be another abandoned commercial building in Calgary soon. Morguard REIT (TSX: MRT.UN) took the hit on that one. That’s what leverage does – all of these carefully planned cash flows balanced with interest payments from debt, and if you lose just a bit of that cash flow, the ratios all go out of whack, covenants get busted, and next thing you know it is a liquidity disaster.

Insurance companies – those with segregated or guaranteed funds will be paying liabilities, and also they have some of their investment portfolio in risk assets (debt that is no longer safe), although one would suspect they would do better than most. Nobody’s also heard a peep from Warren Buffett yet, back in the 2008-2009 days, you had him making $5, $10 billion preferred share deals with Bank of America, and Goldman Sachs during the bottom of the crisis. Nothing to that scale yet. Or perhaps he’s just buying back stock?

It’s also encouraging to see Costco doing as well as it has been. They should be declared a “too important to fail” national security company. Must say in my last visit, their supply chains are still looking mighty good. The employees are doing real hero’s work. Compared to Loblaw (TSX: L) chains (including Superstore, and Shopper’s Drug Mart), night and day difference. It shows.

What’s India’s secret? Over a billion population, but 194 reported cases to date…

Finally… where’s the climate emergency now? From a social/cultural standpoint, I think this event has given everybody a very healthy dose of perspective as to what happens when things go really dysfunctional, and the fact of how smoothly things have been running to date – do we really want to be throwing sand into the gears in the future once this is all said and done?

There’s still too much to look at out there. Found an interesting small software company that feels Constellation Software-ish but sadly without the management that has a huge ownership stake.