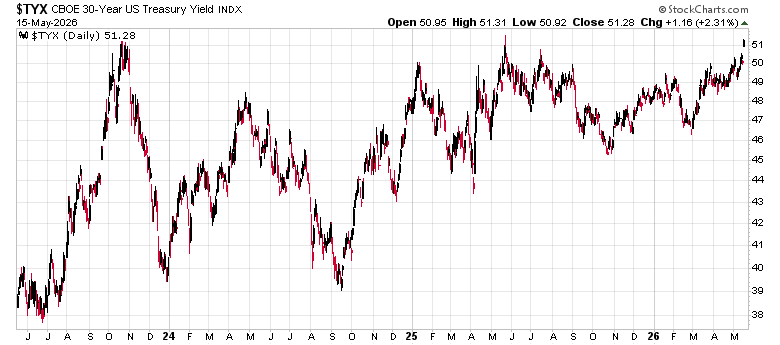

The rise in the 30-year US treasury bond yield post-Iran military action has been ominous:

What blows up when long-term US government bond yields go to 6, 7, 8%?

One answer – the purchasing power of cash.

Here’s the chicken and egg problem and this is what makes markets tricky.

A rise in the long-term risk-free (or let’s just say “so-called” risk-free rate as clearly risk-free is no longer without risk!) will result in the decrease in the capitalized value of future cash flows. This should depress equity valuations.

However, at some point, equities have a component of balance sheet value, which will maintain its value in real terms, but in nominal terms will increase in value over time, all things being equal. This especially applies to firms that have obtained their assets through non-floating rate debt financing.

So we have the yin and the yang of monetary debasement in action – future cash flows are worth less due in current dollars to rising interest rates, while asset values will rise in nominal terms.

Is there a value in holding cash when every day they purchase less in assets?

Possibly – but only when everybody has a rush for cash at the same time. Predicting when or if this happens is difficult.

What causes a rush for cash?

People needing to suddenly (key word – suddenly) make debt repayments or incurring expenses that need to be paid in short order. The perception that the assets in question are garbage and need to be dumped quickly.

When does this happen?

Covid-19 was a good example – nobody is working, everybody needs to raise money for insurance claims. Companies’ earnings will crater due to demand destruction.

9/11 was another example – massive insurance claims from disruptions triggers a need to raise cash immediately.

The 2008 economic crisis – the impending demolition of the financial system – raise cash!

There were obvious catalysts in these cases. What will trigger a need for cash in 2026?

“What will trigger a need for cash in 2026?”

One that might be obvious in hindsight is a crypto collapse once the market believes strongly that the Republicans will be trashed in the mid-terms, Trump will be impeached and the implicit/explicit support for graft evaporates.

Jeffrey Gundlach seems to think that as the long term yields rise there’s a strong possibility of some sort of restructuring of that debt. Not sure whether this has any merit. Not even sure if Mr. Gundlach is someone I should bother listening to…aren’t algorithms great!