I was fortunate enough to get rid of most of my Teck in 2024 when there was a massive amount of speculation with regards to whether the company would sell itself out entirely or just the coal business division. While I had been against the sale of the coal division, in retrospect it has turned out to be a fairly good decision for the company (at least in the short term) – while metallurgical coal pricing has generally stayed at levels where Teck would have been profitable, it is nowhere close to what it was in the 2022 price boom.

Teck’s resultant business is now concentrated in the sale of two metals (noting the mining of ore and the refining are separate processes) – copper and zinc. The byproducts of lead and molybdenum is coincidental. There is also a relatively small amount of silver and gold refined at their Trail operations (still, hundreds of millions and a hundred million respectively!).

Revenue-wise, the copper operation is about 2/3rds of the company, while the zinc operation is 1/3rds.

The Zinc operation is relatively stable. Over the past year the price has been trading at roughly a 20% price band.

The real action is in copper. Teck gambled and succeeded with its QB2 copper project – while actual results have been slightly less than initially promised, it has borne fruit and has made the company a primary copper play.

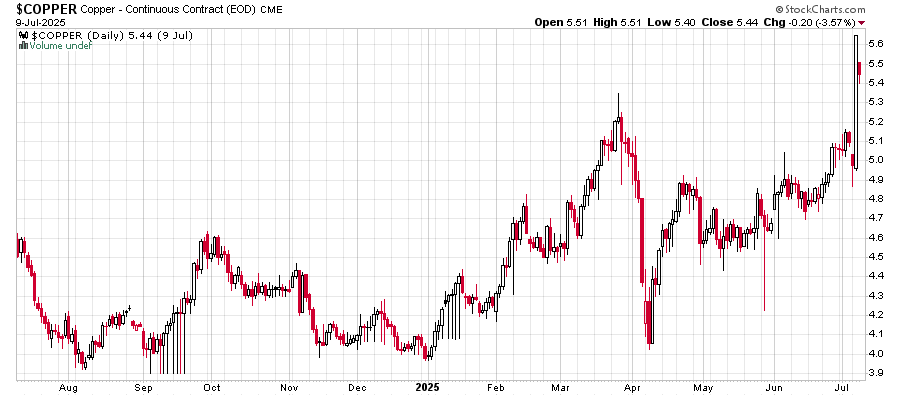

Cue in the commodity price of copper going nuts over more tariff threats:

Teck is projecting 490-565 thousand tonnes of copper production in 2025. With a sensitivity of $15 million EBITDA per US penny on copper, if this is sustained, they will be raking it in at USD$5.60 copper. The market, by virtue of Teck’s stock price drop on the increase in the spot price of copper, is skeptical.

Very roughly, the US$1 increase alone results in a $3/share EBITDA increase on an annual basis. Minus roughly 40% in taxes results in +$1.80 EPS over and above what they’ve posted. Given the relatively unlevered balance sheet (which is flush with cash from the coal sale, albeit management is blowing money like crazy on share buybacks at all-time high prices) the valuation is not bad compared to other purer copper plays like Freeport (NYSE: FCX). I’ve been a little puzzled at the market reaction. While I wouldn’t be buying shares, I do not have a problem holding onto what I currently own – barring a crash in commodity pricing, it would appear the downside from the 50 level is relatively limited.

There’s the idea that the latest rush is just folks stockpiling ahead of US tariff.

This did not age well at all!! The most recent Q2 had major cost overruns and delays on everything and the market (and myself) clearly do not like it at all. Maybe Rio Tinto or somebody else can put Teck out of their misery as originally intended.

“it would appear the downside from the 50 level is relatively limited.”

Oh my, my post was terrible.

Trump took down copper futures today US$1.10, neatly reversing what happened three weeks ago.