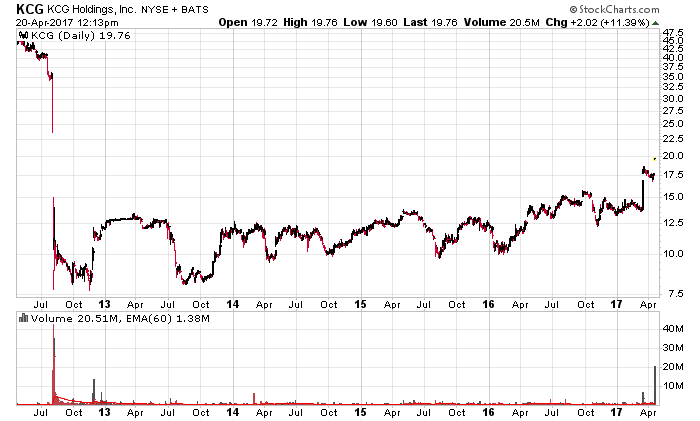

KCG Holdings (NYSE: KCG) looks like it will finally be bought out by Virtu (Nasdaq: VIRT) for US$20/share, cash. They also announced their first quarter results, and according to my scorecard they did better than expected – while their bottom-line net income was slightly negative, they were significantly better on trading revenues than I was expecting. I was expecting a very lacklustre quarter due to incredibly low market volatility in the quarter. Interactive Brokers (Nasdaq: IBKR) is a regular conference call I read and they can attest to the impact of low market volatility on trading.

My investment history with KCG is quite fascinating. I did not disclose things here until October 2016, but I have been trading the stock at various times since 2013, which resulted in material performance gains, especially in 2013 (I took a fairly heavy call option position at the second half of the year). It has exhibited a narrow price range since its merger with GetCo after their August 2012 trading blow-up. The company has generally been off the radar of most investors as it received little analyst coverage and was treated like toxic trash.

Virtu has a plan to raise $1.65 billion in debt financing for the merger and also has sold $750 million in equity at $15.60/share, which should make the buyers happy considering they are now trading at $16.40/share – the market believes this will be quite valuable for Virtu. KCG’s existing 25% shareholder has consented to the agreement, which makes it very unlikely that the deal will not pass through KCG shareholder approval. Given the highly strategic nature of the acquisition, I also doubt there will be other competitors for KCG. Thus, this merger looks like a done deal.

Current trading is at US$19.75. The expected closing is in the third quarter of 2017. As the current spread between market and US$20.00 is around 127 basis points, this would imply a merger arbitrage spread of about 3.8% annualized, so I am in no rush to sell as I have nothing else to deploy my capital into.

The only other issue of concern is KCG’s senior secured debt, maturing on March 15, 2020. According to the fine print, the notes can presently be called off at 103.438 cents on the dollar and there is a required offer for 101 cents on the dollar due to the change of control (which would be redundant since the notes are trading over this in the marketplace). I would suspect Virtu would be eager to get these notes off the books as quickly as possible as they contain covenants that would otherwise restrict the KCG entity. I’ll hold onto these as long as possible but do not think they will survive much longer.