I’ve spoken about US dollar cash parking in the past (back in 2011!). Since then the offerings have not changed tremendously – the standard option is VGSH which gives you 2-year duration exposure to US interest rates. Whenever interest rate hikes abate, this ETF should do reasonably well – unless if there is a massive inflationary spike.

Interactive Brokers gives out 1.2% on US cash balances. This is not a terrible option if you don’t want to engage in transactions to eek out another 80 basis points or so of “nearly risk-free” money. However, other brokers generally don’t give out interest income on their idle cash balances and thus it makes it worthwhile to shop for short-term options if you have high cash balances while you wait for better investment options (as you can tell, I’m in that situation currently).

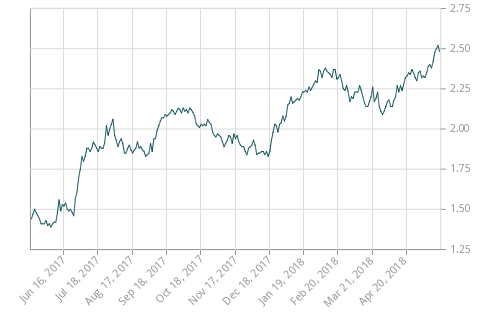

VGSH has been a perennial standby, but the duration risk over the past couple years really shows itself in the charts:

Interestingly over the past two weeks the 2-year US treasury dropped in yield from about 2.58% to 2.32% and hence this was enough to take the ETF up about 0.6% which is very unusual volatility historically. VGSH right now has a YTM of 2.5% and an MER of 0.07%, which still makes it very cheap for short-term exposure to 2-year AA-rated debt.

Still, one annoyance is that if you were unlucky to hit the rising interest rate lottery and be one of those September 2017 investors in VGSH, it can be annoying especially when you know you’re still in a tightening interest rate environment. Since 2011, there is an alternative ETF class that seems to offer a solution: target-date maturity ETFs.

In particular, BSCI will terminate at the end of December and contains investment-grade corporate ETFs that will mature throughout 2018. After June, the ETF will accumulate cash (by maturities) and invest the proceeds in T-Bills until the final termination at the end of the year. The yield to maturity on this fund is 2.17% and MER is 0.1%, so this is not a bad way to skim a couple percentage points while waiting. The ETF is also exceptionally liquid (spreads are a penny wide in size).

The main competitor to this is IBDH, and it is slated to mature on December 15, 2018. It is mostly the same product as BSCI except that it is already in its cash accumulation phase (47.5% in a short-term treasury fund). This will give 2.1% minus 0.1% in MERs. Liquidity is also typically a penny on the exchanges.

Barring a massive financial crash of cataclysmic proportions (e.g. something bigger than 9/11 – I’m thinking around the scale of multiple nuclear detonations in major US cities where we would have bigger problems than how to liquidate our investments from the radioactive ashes), these ETFs are modestly safer than VGSH by virtue of their lower duration. They seem to be a good vehicle to park cash in a rising interest rate environment.