Centrus Energy (Amex: LEU) was formed out of the pre-packaged Chapter 11 bankruptcy proceedings of the entity formerly named USEC Inc.

The corporation primarily derived its revenues from reprocessing Uranium from nuclear warheads from Russia and the USA. The reprocessed nuclear fuel was then sold to nuclear power facilities. It was a reasonably profitable activity – for example, in 2006 and 2007, the company earned roughly $100 million in after-tax income.

In addition, the company is working on a centrifuge project that would allow for the cost-effective (compared to gas diffusion) enrichment of low-grade enriched uranium. These enrichment projects, as Iran is discovering (and they are attempting to produce weapons-grade uranium), are not trivial tasks to overcome. Imagine being given a million ping-pong balls, and half of them weigh 1% lighter than the others – how do you separate them?

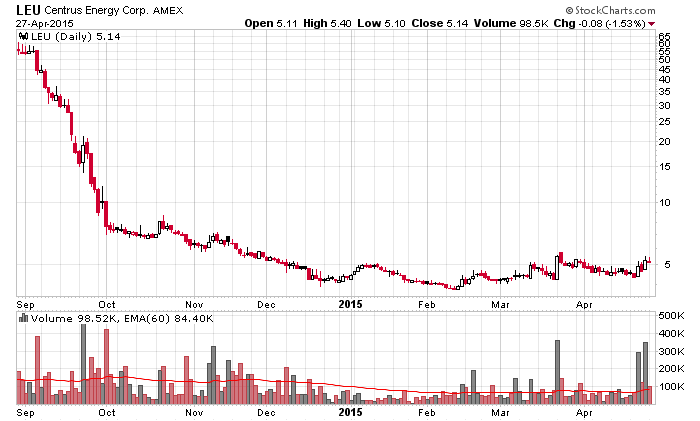

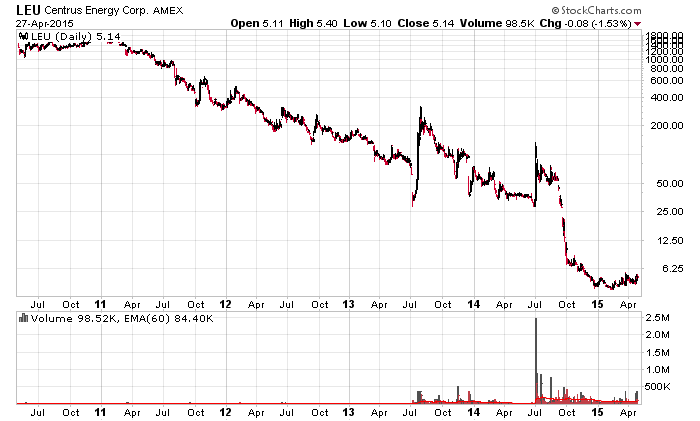

Things changed with the business. The contract with Russia expired (and diplomatic relations between the countries had soured anyhow). Nuclear energy after the Fukushima reactors blew up took a massive hit. The market for Uranium had essentially peaked in the early 2000’s and pretty much now most producers are on life support if your name is not Cameco or subsidiaries of Uranium One. We fast forward in 2014 and the company cannot pay back its $530 million in convertible notes and is forced to recapitalize.

The recapitalization left the company with $240 million in notes to existing note holders and preferred share holders and 95% of the equity. This also left USEC equity holders with 5% of the company. These shares continued to trade down some 50% post-recapitalization until the remaining entity has a market cap of about $50 million and $240 million in notes.

In terms of the balance sheet, things are very ugly. At the end of 2014, while they do have $220 million in cash, they have significant pension liabilities and also considerable negative tangible equity. On the income side, they have negative gross margins and without a real market for nuclear fuel, which is stocked up for the remainder of this decade.

So what could possibly be an investment case for this company?

It deals with the centrifuge project. One would suspect that this is an item of USA national security and that there would be geopolitical considerations to keeping it alive for future purposes. Accounting-wise, this project does not really appear on the balance sheet except as intangibles. One could argue that the “true” value of the project is worth much more than what appears on the balance sheet.

A very condensed consideration of nuclear energy at this point in time:

One also has to weigh in the factor that world uranium supplies have not been mined as intensively given the relatively low prices seen in the last decade. Nuclear power plant construction has also slowed down due to the 2011 Japan earthquake, but China is building more than 20 reactors, and this is higher than Germany’s 9 (which will be shut down). It is likely China will continue building more nuclear reactors to replace their coal power plants (pollution being one reason).

Japan is a wildcard – they currently have 43 reactors operating and the current government’s intention is to continue producing nuclear power. India is also expanding their nuclear generation portfolio (noting that their nuclear production is going to increase 70% in the next two years – reference Cameco).

Oil and gas does not explicitly compete with nuclear power because of how the power is generated – nuclear power provides base loads, while gas powered plants can be turned on and off relatively quickly and are peak load providers. Nuclear plants are direct competitors to coal powered plants.

Management

Centrus’ first real act was to hire the former deputy secretary of the US Department of Energy in the US federal government. His rolodex must be quite large and considering that the Republican-held congress has made some inquiries is probably a better sign than not that the new CEO carries a bit of clout as Centrus is fairly dependent on US government funding at present.

The investment thesis

The short part of the story is that the stock is trading extremely low simply because there is a culmination of nearly every single bad circumstance for the production and sale nuclear fuel. If these variables were to change, it would appear that a $50 million market cap for this sort of company would be extremely low. While it is not likely that they will ever get back to the days where they will earn $100 million in net income, there is a considerable chance they could generate positive income of some quantity.

Other than pension liabilities, the other primary liability the company has are its US$240 million in notes, which are structured for maturity on 2019 but can be extended to 2024 if the centrifuge project goes ahead. In 2015, the notes accrue 5% cash interest and 3% payment-in-kind (in the form of more notes), while in 2016 and beyond, the notes accrue 2.5% interest and 5.5% payment-in-kind (in the form of more notes). They will not be a huge financial burden until maturity.

Past history would suggest that the company would recapitalize these notes if solvency became an issue again.

The last reported trades on TRACE of any real size (i.e. par value of $100,000 or greater) was at 45 cents on the dollar, which is hardly a ringing endorsement by the bond market. Assuming a 2019 payout, that would be roughly a 25% yield to maturity.

The risk-reward here on both the equity and debt are high risk and extremely high reward if things work out for the nuclear fuel industry. There are a ton of what-ifs to consider, but one would think the worst-case outcome for Centrus at this point is bleeding cash until another recapitalization in 2019 (I’d guess you’d see a maximum of 50% downside but it should be reasonably obvious that they are going nowhere). In terms of upside, if all the stars lined up correctly, you could see a 10-bagger over a few years. I have no idea what the probability of this would be, but I’d ballpark it at 10-30%.

This is also a rare company that would likely be bidded significantly higher in the event of a nuclear detonation occurring somewhere in the world, although they would likely be sold if there was a civilian nuclear power plant incident (in line with Chernobyl or Fukushima).

The financial statements otherwise are nearly useless in terms of properly trying to value the company.

Final note

There is a lot of analysis work that I have performed here that is not in this post, but the previous 1,000 words roughly summarizes the investment. A whole bunch of commodity risk, political risk, technology risk and financial risk.