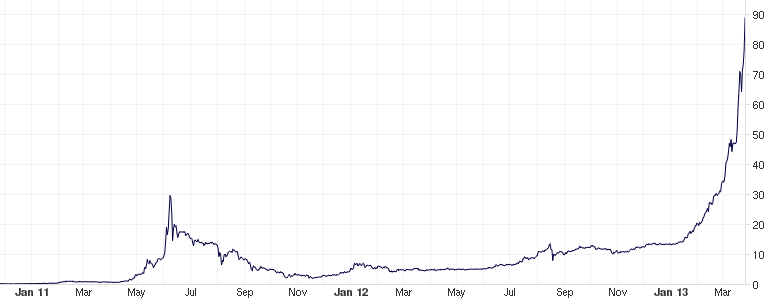

Bitcoins have been making some media headlines as of late because their chart recently went exponential:

I wrote about Bitcoins quite some time ago and my analysis today is still the same – ultimately a currency is only as good as the confidence that people have in it, and digital currency has a drawback of counterfeit-style currencies (e.g. why not take the open source of Bitcoin and then create your own new type of virtual currency?). Again, Bitcoin has the first-mover advantage, but who wants to subscribe to using Bitcoins when essentially the scheme has a pyramid scheme style element where the initial players in the market have a huge economic edge on those that start on it today?

My suggestion for those that are genuinely scared of their purchasing power of their money is to invest it in something that will continually be in demand. Whether this is in equities, gold, guns, or fine scotch is another matter – each of the four categories goes through its periods of high and low price variations.