I have been analyzing Blackberry (TSX: BB) on-and-off since their last quarterly report disaster and gained a rather wide comprehension of the challenges facing the mobile sector. It is almost reminiscent of what happened in the personal computer space in the 1990’s, with the notable exception that in terms of marketing, mobile vendors (Canada: Telus, Bell, Rogers, USA: AT&T, T-Mobile, Sprint, Verizon, etc.) become a material consideration in terms of consumer acceptance of handheld devices. While in the PC-space, people would just purchase their computers outright (with the obligatory Microsoft Windows license), typically people purchase their handheld devices on an opaque financing plan where you pay the implicit fee of the phone that is baked into the monthly payment for mobile phone service.

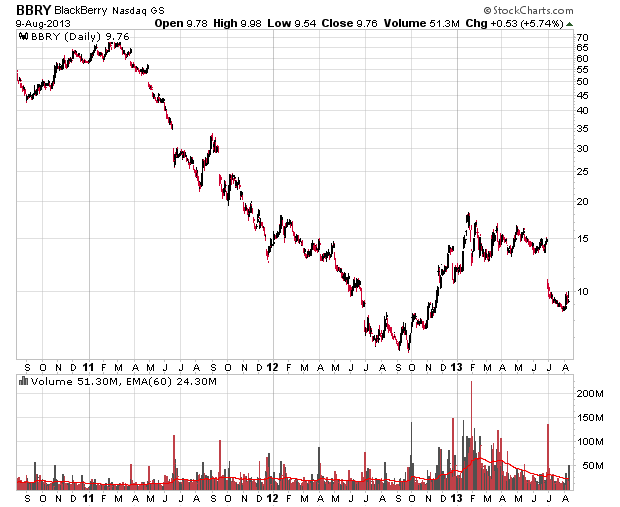

Blackberry stock has been hammered over the past few years – any investor in the stock from 2011 and earlier is guaranteed to be in a loss situation:

Still, as many market participants are aware, from a financial perspective, at current valuations Blackberry is not that in rough shape – despite having a market cap of $5 billion at Friday’s close, they have about $2.8 billion cash in the bank, and still have a very significant revenue base, and most importantly, their technology platform is still top-notch and relevant. It appears the challenge at this point is from a marketing perspective.

None of these financial metrics are a secret and thus should not be a material consideration in terms of a purchase decision unless if one believes the market is somehow misreading the financial statements (which I do not believe is the case). Rather, the relevant variable to consider is whether Blackberry will retain some sort of presence in the market that will enable it to be profitable, whether it is through technical or marketing clout.

I generally do not believe that it is a requirement to be the mass-market leader in order to be profitable – rather, if they can continue carving out their typical niche in the corporate-type sector that they should continue to survive with acceptable profitability. Right now, Samsung through their Google Android offerings are mopping up the consumer market, but the industry is very flighty – Apple iPhone was all the rage a couple years ago, and tomorrow, who knows?

According to some survey data (and this was a quickly pulled off link from the internet and is not designed to be authoritative by any means and is strictly USA geography), Android controls about 50% of the market, and iPhone controls about 40%, and Blackberry is currently at around 5%. This could go up or down, but intuitively it is not a stretch to think that in the future more than 1/20 phones sold could be a Blackberry.

While the rumour last Friday about them potentially going private gave their stock a boost, I highly suspect that such rumours are simply about some hedge fund creating the news piece to allow it to bail out of an outsized position. I also doubt the regulatory environment would enable this transaction to occur.

Prem Watsa, through Fairfax, has a 9.9% stake in the company and also is sitting on the board of directors. He has a savvy, contrarian mind, and although the investment is probably somewhat out of his niche, I’m going to guess that he did have some staffers that are more in tune with the industry to give him some good advice on this one. His purchase price was considerably higher than existing valuations.

I’ve written about Blackberry (RIMM) before (link) and made a comment on analyst expectations – how important it is for potential investors to be purchasing when the expectations are low rather than high. In my June 2012 post, I noted the following estimates:

Today, we have the following estimates (noting the significant notch down after the last quarter update!):

Now, these are estimates that are getting close to worth investing in – mainly the February 2015 estimate of the company losing 80 cents a share (or about $410 million!). This is not a lofty goal for the company to achieve if they can maintain some sort of market presence. The number does assume a significant amount of erosion of the current customer base.

I am factoring in a high probability for the rest of 2013 that the company will continue to languish in the upper single digits as institutional investors attempt to offload shares for tax loss purposes and also the investors that invested into BBRY for the turnaround story likely will have their backs broken and will bail out – what fund manager wants to confess to holding this dog in their 2013 statements? However, the investment story at present is more compelling from a risk/reward ratio today than it has been over the past two years and I will be keeping a very sharp eye out for a potential entry. Obviously I’d like to see more negative sentiment baked into the stock price, and I certainly wouldn’t want to be paying any potential “takeover and go private” premium and will wait for this to blow over before considering my options.

Also not helping is my outlook on the macroscopic side of the market, which I believe is getting frothy on the equity side.