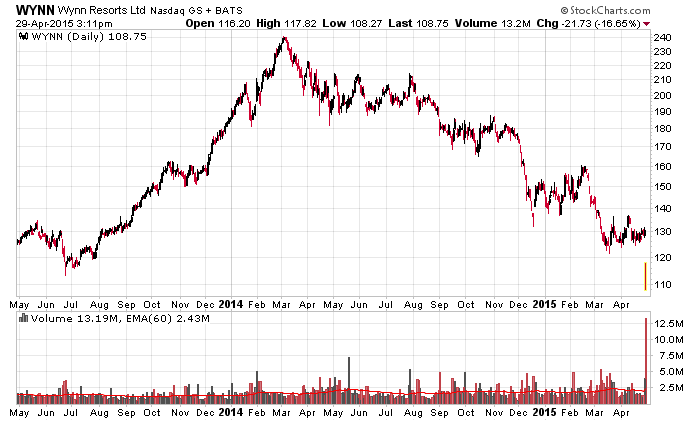

One of the best commentators on conference calls is Steve Wynn (Nasdaq: WYNN) and suffice to say, he has a few zingers in his last conference call. His company’s stock has gotten hammered some 16% today and over half since early 2014.

Some notable quotes from his conference call:

It is impossible for us to predict how long [the downtrend in business conditions] that will last. We’re not in a position to answer those kinds of questions intelligently. We’re only in a position to react intelligently to what we see.

He goes on a speech about how the company will always be able to manage its debts and affairs, and also about how dividends will only be given from cash that has historically been earned:

So as we look backwards for the fourth quarter and especially during the last four months, and understand what’s happening, both in Las Vegas because of the Asian impact on Baccarat, and we look back and then we extrapolate and try predict the future, or at least understand what most likely will be the future, it is foolhardily and immature and unsophisticated to issue dividends on borrowed money. We only distribute money that’s free cash flow based upon our earnings that trail.

…

Dividends are nothing and – we don’t say that because we have a business, that we now have a $0.50 dividends forever. That’s baloney and any company that does that is irresponsible. We distribute the money that we make after we make provisions for capital expenditures and all of our other obligations, to creditors and to our employees. And then we distribute aggressively whatever is free and easy to distribute after that.

The note about issuing dividends from borrowed money should resonate with most oil and gas producers in Canada these days – the only reason why most of them are issuing dividends is simply because they’d get their shares jettisoned from the huge pool of income funds. It would also be an admission of defeat and a negative signal to the market.

On a dialog on the conference call with his own president of the Las Vegas casino (which in my humblest opinion had a dinner buffet that was remarkably worth the US$45-ish that I paid for it):

If you were to ask me, since we’re making forward-looking statements, what will the second quarter look like in Las Vegas? Weak. Do you hear me? Weak. So I’m trying to lower expectations here. This notion of a big recovery is a complete dream. I don’t think Las Vegas is experiencing a great recovery. I think it’s still very patchy and I think that that’s probably our non-casino revenue in the first quarter was flat. I’d be thrilled if it was flat in the second quarter.

It is very rare when you get a CEO making such refreshingly honest statements. There’s a bunch of other commentary here, but I will leave that as an exercise to the reader.

Business notwithstanding, there is a whole bunch of drama going on over at WYNN at the present time, including the divorce of the CEO spilling over onto the business side of things.

Genworth MI (TSX: MIC) reported their 1st quarter earnings results yesterday. The report can be summed up as a relatively boring, “steady as she goes” type quarter, which is somewhat surprising considering the general predictions that the degradation in the Alberta real estate market would cause considerable stress in the sector.

The bottom line earnings took the book value to $36/share.

While the market is signalling there is going to be further losses later this year, the first quarter result had a loss ratio of 22%, which is generally on-level with prior quarters – the company projects 20% to 30% for the year.

Despite the winter quarter being the slowest quarter of the year, year-over-year statistics show a marked increase in unit volume (23,951 in 2014 vs. 32,760 in 2015) and also the net premiums written ($84 million to $130 million). The Q1-2015 net premiums written was also goosed up by the recent CMHC mortgage insurance premium increases. On June 1, 2015, there is another CMHC premium increase on higher ratio mortgages which will also result in a $25-30 million increase in net written premiums.

The company’s insurance in force exposure is 18% in Alberta for “transactional” type mortgages, which are mostly those with 20% or less down-payment. Delinquency rates continue to be very low (0.11% nationally) without any pronounced increases other than a mild rise in Quebec. Ontario has a 0.05% delinquency rate.

On the balance sheet, the company’s investment portfolio yielded 3.4%, but they had some interesting commentary, stating “At this time, the Company believes that the capital adjusted return profile of common shares is less favorable than in the prior year”. As a result of this and also minimum capital test guidelines, they have increased their allocation to preferred shares. Similar to last quarter, they also went out of their way to specify that 75% their energy company investments (in bonds and debentures) were in pipelines and distribution, and the other 25% were in “integrated oil and gas companies with large capitalizations”. The bond portfolio has a mean duration of 3.8 years.

The company has capital that is 233% of the minimum capital test (currently $1.52 billion required) and the internal target with buffer is 220%. This leaves $200 million available for the company to either repurchase shares or distribute in a special dividend. They announced their regular quarterly dividend of CAD$0.39/share with the quarterly release but did not give any indications as to what else they will do with the excess capital.

At a current market price of (roughly) CAD$35/share, I generally believe the company’s valuation is slightly on the low side of my fair value range estimate. I would not start to think of divesting until CAD$40, but an actual sale decision would likely be at higher prices.

I still hold shares from MIC, purchased back in the middle of 2012. Seeing the recent price drop to CAD$28/share would have been a decent opportunity to add more shares and I doubt we will see that again unless if there is a profound economic malaise that hits Canada. If we can survive US$50 oil, our economy is more robust than most think (noting that the rest of the commodity markets have also plummeted). MIC also continues to be a stealthy way to purchase Canadian real estate and also a proxy for a bond fund at a very low management expense ratio. The yield in today’s income starved market is a bonus.

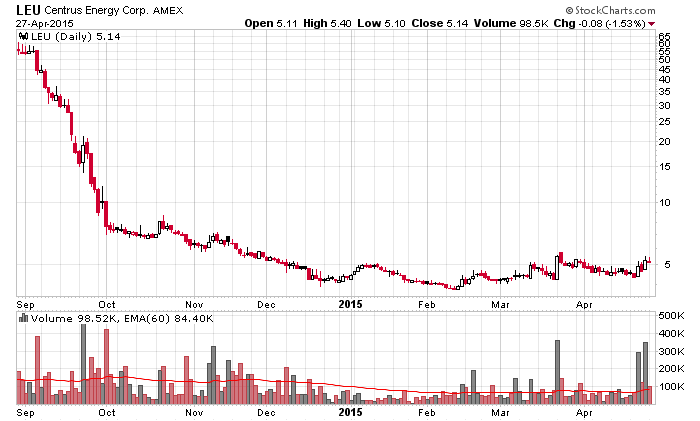

Centrus Energy (Amex: LEU) was formed out of the pre-packaged Chapter 11 bankruptcy proceedings of the entity formerly named USEC Inc.

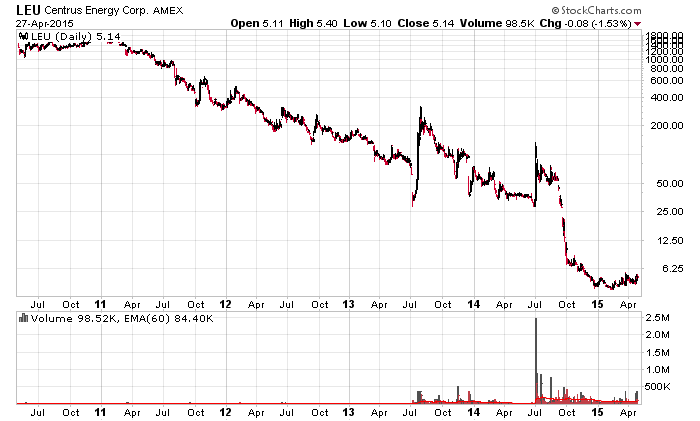

LEU since recapitalization (September 30, 2014)LEU – 5 year chart (adjusted for reverse stock split)

The corporation primarily derived its revenues from reprocessing Uranium from nuclear warheads from Russia and the USA. The reprocessed nuclear fuel was then sold to nuclear power facilities. It was a reasonably profitable activity – for example, in 2006 and 2007, the company earned roughly $100 million in after-tax income.

In addition, the company is working on a centrifuge project that would allow for the cost-effective (compared to gas diffusion) enrichment of low-grade enriched uranium. These enrichment projects, as Iran is discovering (and they are attempting to produce weapons-grade uranium), are not trivial tasks to overcome. Imagine being given a million ping-pong balls, and half of them weigh 1% lighter than the others – how do you separate them?

Things changed with the business. The contract with Russia expired (and diplomatic relations between the countries had soured anyhow). Nuclear energy after the Fukushima reactors blew up took a massive hit. The market for Uranium had essentially peaked in the early 2000’s and pretty much now most producers are on life support if your name is not Cameco or subsidiaries of Uranium One. We fast forward in 2014 and the company cannot pay back its $530 million in convertible notes and is forced to recapitalize.

The recapitalization left the company with $240 million in notes to existing note holders and preferred share holders and 95% of the equity. This also left USEC equity holders with 5% of the company. These shares continued to trade down some 50% post-recapitalization until the remaining entity has a market cap of about $50 million and $240 million in notes.

In terms of the balance sheet, things are very ugly. At the end of 2014, while they do have $220 million in cash, they have significant pension liabilities and also considerable negative tangible equity. On the income side, they have negative gross margins and without a real market for nuclear fuel, which is stocked up for the remainder of this decade.

So what could possibly be an investment case for this company?

It deals with the centrifuge project. One would suspect that this is an item of USA national security and that there would be geopolitical considerations to keeping it alive for future purposes. Accounting-wise, this project does not really appear on the balance sheet except as intangibles. One could argue that the “true” value of the project is worth much more than what appears on the balance sheet.

A very condensed consideration of nuclear energy at this point in time:

One also has to weigh in the factor that world uranium supplies have not been mined as intensively given the relatively low prices seen in the last decade. Nuclear power plant construction has also slowed down due to the 2011 Japan earthquake, but China is building more than 20 reactors, and this is higher than Germany’s 9 (which will be shut down). It is likely China will continue building more nuclear reactors to replace their coal power plants (pollution being one reason).

Japan is a wildcard – they currently have 43 reactors operating and the current government’s intention is to continue producing nuclear power. India is also expanding their nuclear generation portfolio (noting that their nuclear production is going to increase 70% in the next two years – reference Cameco).

Oil and gas does not explicitly compete with nuclear power because of how the power is generated – nuclear power provides base loads, while gas powered plants can be turned on and off relatively quickly and are peak load providers. Nuclear plants are direct competitors to coal powered plants.

The short part of the story is that the stock is trading extremely low simply because there is a culmination of nearly every single bad circumstance for the production and sale nuclear fuel. If these variables were to change, it would appear that a $50 million market cap for this sort of company would be extremely low. While it is not likely that they will ever get back to the days where they will earn $100 million in net income, there is a considerable chance they could generate positive income of some quantity.

Other than pension liabilities, the other primary liability the company has are its US$240 million in notes, which are structured for maturity on 2019 but can be extended to 2024 if the centrifuge project goes ahead. In 2015, the notes accrue 5% cash interest and 3% payment-in-kind (in the form of more notes), while in 2016 and beyond, the notes accrue 2.5% interest and 5.5% payment-in-kind (in the form of more notes). They will not be a huge financial burden until maturity.

Past history would suggest that the company would recapitalize these notes if solvency became an issue again.

The last reported trades on TRACE of any real size (i.e. par value of $100,000 or greater) was at 45 cents on the dollar, which is hardly a ringing endorsement by the bond market. Assuming a 2019 payout, that would be roughly a 25% yield to maturity.

TRACE prices of LEU 8% notes (maturing September 30, 2019 or 2014)

The risk-reward here on both the equity and debt are high risk and extremely high reward if things work out for the nuclear fuel industry. There are a ton of what-ifs to consider, but one would think the worst-case outcome for Centrus at this point is bleeding cash until another recapitalization in 2019 (I’d guess you’d see a maximum of 50% downside but it should be reasonably obvious that they are going nowhere). In terms of upside, if all the stars lined up correctly, you could see a 10-bagger over a few years. I have no idea what the probability of this would be, but I’d ballpark it at 10-30%.

This is also a rare company that would likely be bidded significantly higher in the event of a nuclear detonation occurring somewhere in the world, although they would likely be sold if there was a civilian nuclear power plant incident (in line with Chernobyl or Fukushima).

The financial statements otherwise are nearly useless in terms of properly trying to value the company.

Final note

There is a lot of analysis work that I have performed here that is not in this post, but the previous 1,000 words roughly summarizes the investment. A whole bunch of commodity risk, political risk, technology risk and financial risk.

North American Palladium (TSX: PDL) operates a mine which has been somewhat profitable, but financing expenses have killed any chances of the overall operation returning money to shareholders.

Balance sheet-wise, they invested $450 million in mining operations, while having a $220 million debt to deal with and a requirement for some cash, which they do not have. A classic case of solvent, but not liquid.

The primary cause of this was doing a deal with the Brookfield devil, where management borrowed US$130 million at a rate of 15% interest in June 2013. The debt was secured by PDL’s assets. Not surprisingly, it has gone financially downhill since then. The debt has since morphed into US$173.2 million as interest has been subsequently capitalized into the loan (and other drama that has happened since that point which I will not get into).

What’s amazing is the corporation somehow managed to find enough suckers to invest in some toxic convertibles in 2014 that significantly diluted the company’s equity but kept enough cash to keep the zombie alive for another year.

Finally, they succumbed to having a quarter of your revenues go out the door in the form of interest expenses and are coming to grips in the form of a recapitalization proposal.

The term sheet (attached) that management came up with to ensure its own survival is quite onerous to all involved.

The salient details are that existing shareholders will keep 2% of the company, unsecured debenture holders will receive 6% of the new company, and Brookfield and partners will keep the 92% after generously injecting US$25 million and releasing their accumulated debt to the firm. Afterwards, Brookfield will float a rights offering where they will raise another CAD$50 million and this will presumably dilute the interests of the then-common shareholders even further if they do not wish to participate.

A holder of 52% of the convertible debentures has been spoken to and agrees to this proposal. They need 2/3rds approval, which is likely considering that the convertible debentures are unsecured and they would receive nothing if the company went through the CCAA route.

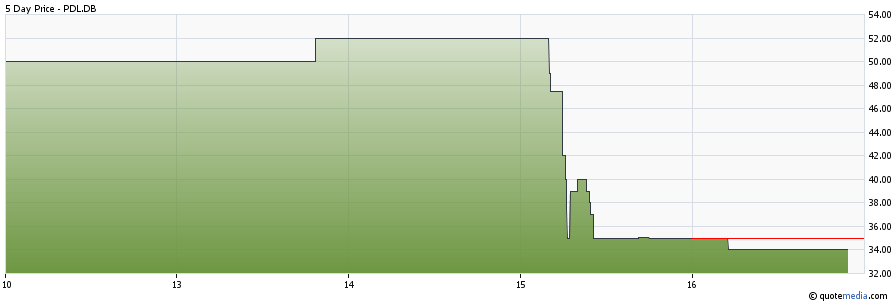

Not surprisingly, existing shareholders/debentureholders of PDL took down the price:

PDL.TO share pricePDL.DB.TO price

The recapitalization document was released on the morning of April 15, 2015 half an hour before trading opened, so astute traders that could skim through the news release and the actual term sheet would have been able to get out at 19 cents if they hit the opening market trade. If you waited until the end of April 15, you would be sitting at 12 cents.

At 7 cents per share of PDL stock and roughly 400 million shares outstanding, the market is valuing the recapitalized version of PDL at CAD$1.4 billion.

It does not take a genius to figure out that, with $220 million in revenues in 2014, the existing stock price is still significantly over-valued. If I was owning any shares of this train wreck, I’d still be dumping at market. Fortunately I’ve never owned any shares (or debt!) of PDL. Purchasing a mining operation at 7 times revenues is not exactly a value play.

However, the albatross of having to deal with a crushing 15% senior secured loan will be off their backs and the resulting entity may have a fighting chance when it doesn’t have to shell out $50 million a year in interest expenses. You just have to figure out at this point what Brookfield’s incentives are to ensuring they get the most of their 92%+ equity stake in a post-recapitalized PDL.

It is fairly obvious by looking at the graph of Genworth MI (TSX: MIC) that institutions are dumping stock in fears that mortgage default rates are going to spike up as a result of economic calamity in Alberta. The CEO of Genworth talking about “heightened vigilance” isn’t helping matters any.

While this might be true, it appears that other real estate metrics are relatively in tune. My cursory scans of the REIT market (e.g. Riocan, H&R, Calloway, all apartment trusts, etc.) doesn’t show any erosion in that marketplace. Banks (e.g. BMO, BNS, etc.) are showing some equity erosion since the middle of 2014, but I’d suspect this is more due to yield curve compression and partially due to the solvency risk posed by syndicate loans to various oil and gas companies.

Other direct lenders, mainly Equitable and Home Capital, have both seen erosion but it is not significant to the point where one would think there is going to be a complete and utter collapse in the fundamentals.

Genworth MI appears to be the whipping boy in the real estate industry. If such fears are warranted, then one would think that REITs and other related stocks would also get proportionately taken down.

So the question now is whether the market is wrong about REITs or wrong about Genworth. Assuming the negative momentum for Genworth MI continues, one would guess that looking at the financial metrics and historical charts (and then-fundamentals of the company at that time) that it is conceivable the stock can get down to about $22-23/share as a floor. This is based on the discount assigned to the stock during the mid 2012-2013 period and the fundamentals of the company at the time.

Today is a little different in that the company has less shares outstanding and has more equity on the balance sheet.

Assuming the Canadian real estate market does not completely nose dive, an investor would still be looking at around 20% downside on existing technical momentum, but fundamentally there is still significant value as the firm is trading deeply below book value at present (right now at a 20% discount). It is like purchasing a leveraged bond fund at a significant discount.

The combined ratio (this is the loss ratio plus the expense ratio) during the depths of the 2008-2009 economic meltdown, did not go above 62%. Delinquency rates never got above 0.30%. Today, it is 39% and 0.10%, respectively. Yes, these numbers will increase as people start defaulting on their Alberta homes, but I simply do not see at present those numbers getting worse than it was in the 2008-2009 era.

I am watching this carefully and may choose to add to my position.