KCG Holdings (NYSE: KCG) is probably best known as previously being “Knight Capital”, which was one of the top-tier US market-making firms back in the days when the Nasdaq traded in quotations of 1/16ths.

The second reason why they are well-known is because due to a badly botched software upgrade on August 1, 2012, where their algorithms managed to incur $440 million in 30 minutes of trading losses before technicians were able to pull the plug. I am quite confident with an unlimited amount of equity on my Interactive Brokers account I could not manage to lose that much money using my fingertips and mouse.

The company was forced to recapitalize and what incurred after was a reverse-takeover by the algorithmic trading firm GETCO. The existing shareholders were massively diluted and this functionally served as a way for GETCO shareholders to liquidate their holdings (backed by General Atlantic). The combined entity was renamed “KCG” (yet another example of a firm acronym-ing their name) and what ensued was an internal purge of legacy Knight Capital personnel. The transition at this time is more or less complete.

The corporation still makes the bulk of their money through market making and related trade execution services. Their prime competitors include other high-frequency trading firms, including the newly public Virtu (Nasdaq: VIRT). In general, the firm makes money when market conditions are volatile and they operate at a loss when volatility is quite muted.

The July to September quarter was a disaster for KCG (and other market-making entities, including Interactive Brokers), while the April to June quarter was quite profitable (think about Brexit!).

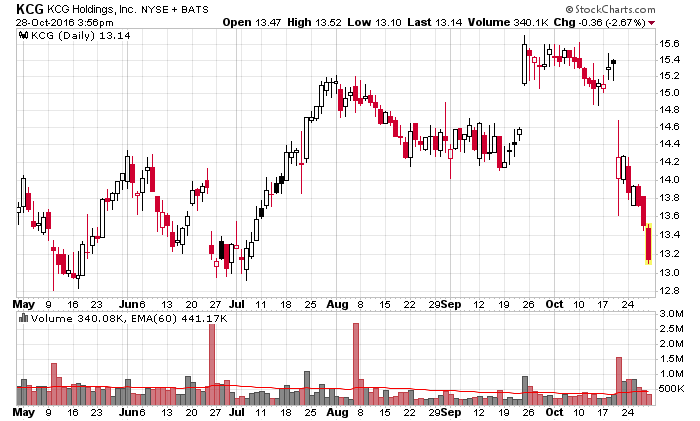

Since the last quarter’s results, KCG shares have tail-spinned:

The business, quarter by quarter, is highly volatile. In the Q2-2016, they reported operating revenues of $280 million, and in Q3-2016 they reported $200 million. As you might tell by this seasonality, it creates volatility in the stock as quantitative algorithms that purchase and sell shares on fundamental data generally go wild with companies like these.

Profitability also varies. The corporation is still trying to cut costs and become lean and mean (like Virtu), but it is taking them time to get to that position where they can be profitable in a very low volatility environment like the last quarter. On the aggregate, they are profitable in the medium run, which means I do not regard them as much of a risk at this moment (unless if their programmers decide to botch up another software upgrade like what happened in August 1, 2012).

The balance sheet is a little more interesting.

Its tangible book value is $15.54/share at the end of September. The underlying corporation has $508 million in cash, and a whole host of financial instruments that vary from quarter to quarter as they maintain an inventory for market making purposes (13F-HR form attached for illustration). In addition, they also own 13.1 million shares of BATS (Nasdaq: BATS), which is presently in the middle of getting acquired by the CBOE (Nasdaq: CBOE) sometime in 2017. The BATS stake is worth a pre-tax amount of about US$380 million at current market value.

Where my accounting experience comes in handy is how this is reported. You would think that owning US$380 million in a publicly traded entity would be reflected as US$380 million on the balance sheet, but this is not the case with KCG’s BATS stake. Instead, it is reported under the equity method of accounting. I will leave out the complications and state that it is reported as $94 million at present on the balance sheet. As KCG sells their BATS shares, the differential between sale price and their carrying value on the asset side will be reported as a gain (subtracting a provision for income tax).

So there is actually about $285 million of pre-tax money that is bottled up and waiting to escape. After taxes, this will be about $200 million leftover (using 30% as a basis – the actual rate may be higher).

You can see why most people do not have the time or patience to go through this minutiae.

On the liability side, we have one significant liability – $465 million face value outstanding of secured senior debt, with an 6.875% coupon maturing March 2020. The debt restricts the corporation to repurchasing shares at a fraction of KCG’s income (if you care to read the fine print, it is available on this 8-K filing) in addition to other nitty gritty details that I will omit from this post.

KCG initially issued $500 million in debt, but decided to repurchase debt at a discount to market earlier this year, when their debt was trading at about 89 cents on the dollar.

Readers of this site perhaps would not be surprised to know that I decided to purchase a decent-sized block of debt at around 90 cents earlier this year. My first disclosure of that purchase is in this post. Unless if the corporation decides to do an August 1, 2012-style blow-up, I regard it as virtually impossible that they will be unable to pay back this debt.

The company has also been actively engaged with the repurchase of its equity (and warrants related to the GETCO merger) at values that have been below book. They conducted a dutch-auction tender last year with excess capital, and they have not made sufficient amounts of money this year to conduct further stock repurchases – their authorization after the previous quarter was a paltry $2 million. However, they can liquidate BATS shares and use those proceeds for equity buyback purposes.

Considering the firm is now trading at a 15% discount to tangible book value, any equity repurchases would be accretive to their book value, in addition to being an EPS boost whenever the markets are volatile enough for them to make money.

So this is a compelling business with a relatively wide moat (market-making is not as easy as initial perceptions may seem), a decent balance sheet, and reasonable prospects for much better business conditions (did I say anything about Donald Trump in my previous post?). It is a company that would find better business conditions when there are higher amounts of market volatility, and assuming they can keep some sort of competitive business edge on the algorithmic side of things, they should be able to generate positive cash flows.

In other words, the downside appears limited, but the upside is less defined.

A question of what their terminal value would be is an interesting study – one would think that if they decided to go private (which would be a legitimate avenue considering everything presented above) that they could do so at a share price obviously above the US$13.10 they closed at today. Management has made promotions of aiming for a “double digit return on equity” in 2017, which I believe is generous, especially on the operating side, but if they get anywhere close to this (or even half of it), the market should value this well north of US$13.10.

So I’m in. Both the equity and debt.