This is going to be a rambling post.

My investing thesis post Covid-19 is simple – invest in companies producing real stuff, with the sweet spot being primary and secondary industries. I am sure there will also be tertiary winners (e.g. technology) but there is a lot of competition in this space and I am unlikely to pick out the winners relative to current market valuations (for instance, if it turns out that Microsoft is the winner in cloud computing, on their current US$1.6 trillion market capitalization, it might not turn out to be very profitable).

In terms of real stuff, somebody has to keep pulling the raw commodities out of the ground in order to fuel the real (not digital) economy. Companies will incur costs to do so, but ultimately the commodity itself will have value. In a depreciating dollar scenario, these commodities will organically exhibit price increases, all other variables being equal. This is a well known process.

However, ultimately commodity pricing is a function of supply and demand. In many industries, there was an assumption with most producing companies that they did not want to hold inventories during Covid, and took actions to streamline. This is quite apparent in the lumber industry, and it was not generally expected that people would be using their CERB or US-equivalent to improve their homes, build fences, and so forth. The result is that lumber prices have skyrocketed.

Other commodities that have exhibited forced price cuts (e.g. oil) are now being bidded up because liquid energy consumption is clearly headed toward normalization (an examination of the Google Map traffic is enough to be said here, but I am sure the economic engineering department of Google makes much better usage of the data than we can from our consumer perspectives).

Gold is also going crazy right now. I have encountered some friends inquiring about gold, and also people with gains on precious metal funds, and inquiries about how to obtain physical gold, and so forth. It is to the point where it is feeling frothy. Just because things are frothy does not mean they will become more frothy.

The underlying basis of demand is likely a combination of a natural increase from the recovery of Covid-19, coupled with a fright of dollar devaluation. In light of the US Government (and world governments in general) blowing out deficits in record magnitude, it is reasonable to think that joint devaluation of currencies will result in increased prices for everything, starting with commodities, but in general, the price of energy is the core to it all.

The quantity of energy consumed is generally a barometer of the health of civilization – this goes back for millennia. Our lifestyle is inevitably linked to the consumption of energy. Don’t get me started on the production economics of mining bitcoins!

Fossil fuels have been shunned upon for various reasons (carbon emissions) and renewable sources have been promoted, but there is a scale limit to how much renewables can be introduced before you incur significant tradeoffs – either significantly higher costs, or reduced reliability (the higher percentage of intermittent sources you have, the more you need to buffer them with dispatch-able energy).

Despite this, renewable sources have been deemed politically correct and have received sky-high valuations and subsidies.

I will make the claim that in terms of industrial levels of power generation, in North America we are reaching a scale limit to intermittent energy production. This will certainly not be a popular opinion or claim. The short story is that renewable energy cannot scale to high percentages in all jurisdictions on an individual grid. In California, for example, during mid-day it produces a ton of energy from solar sources (on a day like today, 11.8 gigawatts!), but broadly speaking, the following are very relevant questions:

a) How much did it cost to get those solar arrays up and going, and to maintain them;

b) How do you buffer the amount of energy on days where it is no longer sunny, or off-peak times?

Question (a) tells you the trade-off economics of building one type of power generation vs. another. Incomplete accounting makes intermittent power look cheaper both from a raw cost perspective (for instance, you do not have to include the cost of a backup source of power when the wind dies down, or the sun isn’t shining), but also with subsidies and omitting environmental costs of production.

The question of (b) is not trivial, but typically it involves a combination of natural gas, hydro, load-following base power (e.g. coal, but not in California!), storage (very expensive in industrial quantities) or imported electricity.

Essentially, somebody has to produce the supply to meet the electricity demand – this is why the more intermittent supply that is added to the power grid, the better it will be for fossil fuels – either you consume a ton of energy up-front to build up your solar arrays or storage solutions, or you consume it in natural gas. Jurisdictions with ample hydroelectric power (such as British Columbia) are also blessed with dispatch-able power, but building dams is a very expensive endeavour, both in raw costs and significantly increased political costs (permanently flooding land is not popular). In other words, for each incremental addition of intermittent energy sources that you rely on to fuel demand, you need a unit of dispatch-able power from somewhere.

The logical course of increasing intermittent resources can be seen in a place like Germany, where the cost of power has skyrocketed as they have removed coal and nuclear energy from their power grid, and attempted to replace it with solar, wind and tidal power. This is not viable without relying on others in the power grid.

One major event that will occur in the future (a matter of when, not if) will be a significant power grid failure that will have been instigated by having too much intermittent energy sources on the grid, without available backup from domestic or external grid sources. This may be caused by a freak transmission failure (cutting an intermittent-heavy grid from a dispatch-able heavy grid) or some other ‘black swan’ event. When this occurs, there will likely be a dramatic shift in power generation policy to increase the robustness of a domestic power grid.

The preceding few paragraphs lead to very political issues regarding energy production. Many will not agree.

This leaves me to my last point of nuclear energy. It has been shunned for a very long time (the documentary Chernobyl was great to watch although it did embellish in some scenes for dramatic purposes, the Fukashima reactor, etc. are all stories that are in the public consciousness), but this is going to change, for no other reason simply because to expand power generation capacity in a carbonless manner there isn’t much room to go other than nuclear.

This is not a call that Uranium commodity pricing will increase (it is a relatively abundant resource at present), but rather that an exploitable avenue is a resurgence of nuclear power in general. I do not know how that will take place, but if de-carbonization continues to be popular, it would be a logical conclusion to replace base load coal, and natural gas plants with nuclear energy. Reactor technology has significantly improved in safety, where Chernobyl-type disasters have no way of happening.

The other issue is that nuclear technology is (for obvious reasons) highly secretive and countries that have competitive advantages in nuclear energy will tend to keep them, in addition to competitive advantages associated with domestic-only production. In the USA, this means companies like BWX Technologies (NYSE: BWXT), who are more or less the sole-source provider for nuclear engines for naval vessels. I bought them post-COVID.

Finally, we have the nuclear materials themselves. While Uranium is a hyped up commodity, and domestically there is only one Canada/USA credible stable large-cap company specializing in its production (Cameco, TSX: CCO), there are also a bunch of other smaller cap companies, including Energy Fuels (TSX: EFR), Denison Mines (TSX: DML), Laramide Resources (TSX: LAM), NexGen (TSX: NXE). Even further down are a bunch of TSXV companies which I won’t bother listing.

However, the commodity itself faces considerable cost competition from central Asian companies, which makes uranium production in North America relatively uncompetitive unless if you believe that geopolitical constraints (e.g. trade embargoes) will then put North American producers on a level cost playing field. In that case, I would be much more interested.

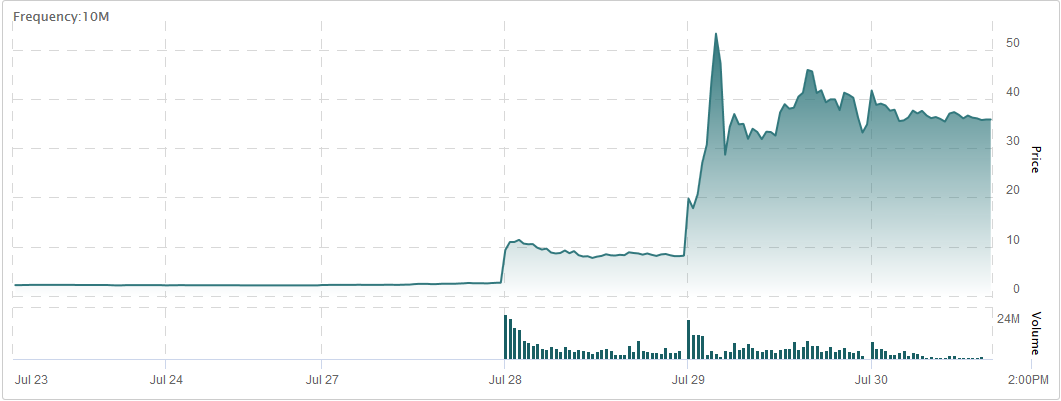

The refinement of Uranium, however, is a much less competitive space (just ask the government of Iran how their attempts on Uranium enrichment is going for it), and a company that I took a modest position post-Covid was Centrus Energy (AMEX: LEU), which has had its stock take off to the point where I can now freely write about it. Be careful – it is very thinly traded and has a small float in absolute numbers (it is heavily insider owned). A case can be made that in an ideal scenario they will trade for much higher than their current price, which has more than tripled since their Covid lows. I’m sure now that I’ve written about it, they have peaked – the downside scenario is that the next generation of nuclear won’t move from the planning stages.