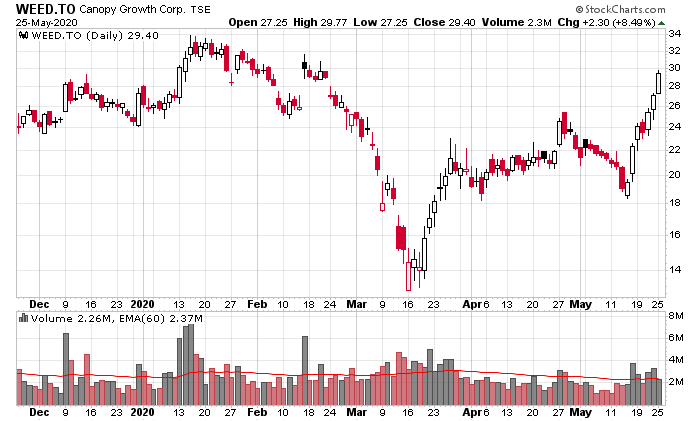

Why anybody continues to invest in this sector is beyond me. But for whatever reason, over the past 7 trading days, Canopy Growth has skyrocketed – yes, this is over a 50% surge up:

I’m not short the stock, but those that are are obviously hurting. It is a heavily shorted stock, with about 40 million shares short on the US side and 11 million on the Canadian side, with a cost of borrow of around 25% (assuming you can actually get shares to borrow).

While I’m not the type to gamble on these stocks, my gut instinct says that it might Tilray these short sellers before crashing again. In March 2019, they reported CAD$4.5 billion in cash and marketable securities on the balance sheet, and at the end of December 2019, it was about C$2.3 billion, an impressive cash burn trajectory. While Constellation Brands did exercise C$245 million in warrants on May 1st, I’m sure Canopy would love another opportunity to raise cash again!

I’m guessing all of these Robinhood and Wealthsimple investors have been happily buying shares. Who knows, they might have the last high!