This is a brief review of the companies that have reported their quarterly results to date in the oil and gas space – specifically the ones in the Divestor Canadian Oil and Gas Index. (ARX, CNQ, CVE, MEG, SU, TOU, WCP have reported).

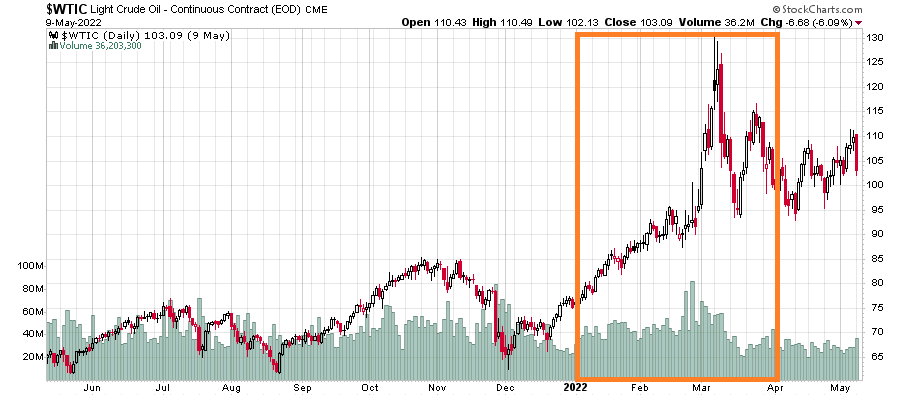

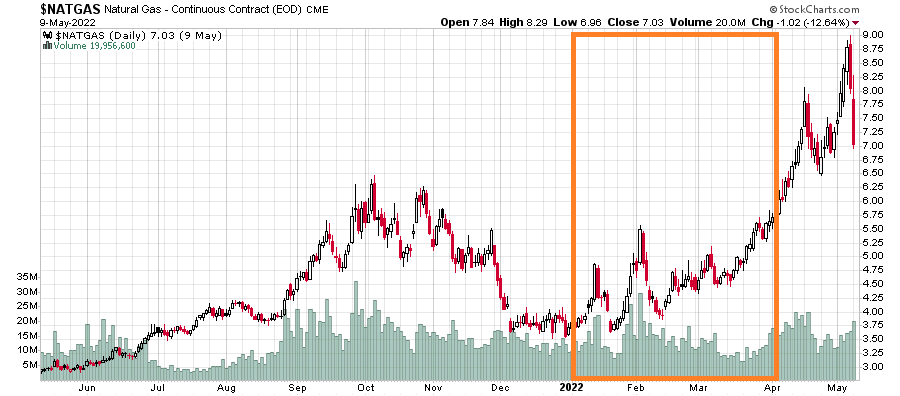

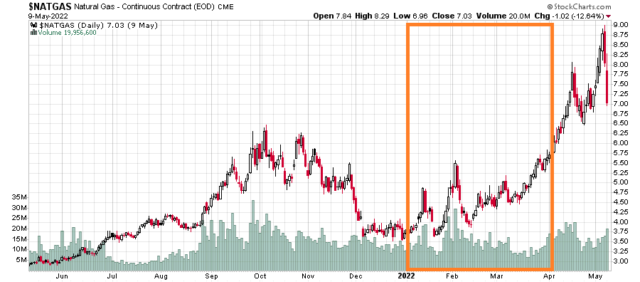

When your spot commodity exposure charts look like this, you know things are looking good:

The amount of bullishness out there in the previous week was a bit nuts and ripe for a correction. When markets ascend for this much time for this duration, there is a natural process where momentum and technical analysis players get cashed out, regardless of any fundamental underpinnings.

The financial market moves much, much, much faster than what goes on at a glacial pace in reality. While the amount that has evaporated out of my portfolio in the past week is impressive, it goes with the nature of finance that things will indeed be volatile, but the intrinsic value of the portfolio remains intact, reflected by real-world economics instead of financial economics.

All of the companies in the oil and gas index have been reporting record free cash flows, but most notably all of the players have been quite tight on growth capital in the sector – the free cash flow for the most part has gone into debt reduction, dividends and share buybacks. Now that most of these companies have reached their leverage targets, they are now continuing to deploy more cash into share buybacks, or (in the case of TOU) special dividends.

The financial mathematics of companies giving off sustained free cash flows (key word being ‘sustained’, noting that fossil fuel extraction is a cyclical industry) is interesting to analyze. I will use Suncor as an example.

Suncor guided in Q1 that their income tax payments will go up from the lower $2 billion range to $4 to $4.3 billion (note that income tax is a function of operating income minus interest expenses and after the removal of royalties, which is another huge layer of money given to the government!). Suncor does not have a material tax shield so they will be fully paying cash corporate income taxes. The Canada and Alberta corporate tax rate combined is 23%, and they have other operations in other provinces and overseas, so we will assume 23.5% as a base rate, which puts Suncor at $17.7 billion in pre-tax income ($13.5 billion after-tax).

Those with an accounting mindset will ask whether net income translates directly into free cash, and Suncor’s capital expenditures are roughly in line with depreciation. My own on-a-paper napkin free cash modelling also corresponds roughly to this $13.5 billion amount in the current commodity price environment.

Suncor has 1.413 billion shares outstanding as of May 6, 2022, so the upcoming year of income is $9.55/share. Suncor trades at $44/share as I write this, and has an indicated quarterly dividend of 47 cents per share ($1.88 annually). Although management has hinted this will go up over time, for now let us assume it is a static variable.

Deciding between debt reduction, dividends and share buybacks usually are a dilemma, but when the math is this skewed it is not.

Suncor’s debt currently costs them about 5.25%, or 4% after-tax. A share buyback not only alleviates the company from paying out the 4.27% dividend, but is also purchasing a 21.7% return on the equity.

This is a no-brainer decision from an optimization standpoint – every penny after regular capital expenditures, should go into a share buyback. The dividend should be brought to zero and shares should be bought back with that amount instead, until such a point where the return on equity goes below a particular threshold (my own personal threshold if I was calling the shots at management would be 12% or anything below $80/share in the current price environment!).

However, there are other variables to consider.

One is that the commodity price environment might not (and indeed is very unlikely to) last forever. There is a pretty good case to made that this particular price environment will last longer than most (instead of spending on capital expenditures like drunk sailors, companies across the grid are shockingly being very disciplined about limiting the amount of growth in production), and also the margin of error of the price level itself is quite high – West Texas Intermediate is at US$100 and even if it goes down to US$75, my models still have Suncor making around $8 billion in free cash. My $80 threshold price for share buybacks would drop to $47/share in this scenario – very close to the current market price.

So the argument to reduce debt is not out of financial optimization, but rather reducing the brittleness of the financial structure of the company. Hence the decision to allocate the residual 75% of free cash minus capital expenditures and dividends to debt reduction, and the other quarter to share buybacks. Although it is not financially optimal if you assume the current environment exists, it is a safe decision. They will do this until they go to under a $12 billion net debt position, which will happen at the end of Q3/beginning of Q4. (Note that Suncor introduced a new conservative fudge factor by adding in lease liabilities into this definition which inflates the net debt number).

After they reach the $12 billion net debt figure, then 50% gets allocated to debt and 50% to the share buyback. At the current commodity environment and share price, they will be able to complete nearly the 10% full buyback with this regime. After they get down to $9 billion in net debt, then the debt reduction goes to 25% and share buyback will go to 75%. I just hope that management has the prudence to taper the buyback and increase the dividend if their share price gets too high.

The other variable is the dividend. While the tax inefficiency of dividends are well documented elsewhere, it does provide a “bird in the hand” component to the stock, and also gives the buyback itself some metric to be measured against. While other people consider a dividend to be very important, I am agnostic about a particular dividend level, except in context of alternatives.

Obviously if a company has capital investment opportunities, you do not want to see a dividend. You instead want to see them deploying this capital in productive ventures. However, in the fossil fuel industry, there is a very good argument to be made to just keep things as-is and just go on cruise control – this is exactly what is happening for all of these companies. They are paying down debt and allocating cash to dividend and share buybacks, especially when all of them are giving out 20%+ returns. There is no reason not to.

The ultimate irony here is that in such an environment where cash flows are being sustained, it works incredibly in the favour of investors that the market value of these companies remains as low as possible, to facilitate the execution of cheap share buybacks.

This leads me to my next point, which is that it does not take a CFA to realize that on paper, many of these oil and gas companies are perfect candidates for leveraged buyouts. Only the perceived toxicity of fossil fuels and ESG has prevented this to date, and I am wondering which institution will be making the first step in outright trying to convert a leveraged loan (even in the elevated interest rate environment, they can get cheap debt) to buy out a 25% cash flowing entity. It is inevitable at the current depressed market prices.

The first warning shot on this matter (which is cleverly disguised as a strategic performance improvement scheme) comes from Elliott Investment Management’s Restore Suncor slide deck. They can’t outright say what they’re thinking – let’s LBO the whole $60 billion (market value) firm!

Needless to say, an investor in this space makes most of their money “going to the movies”, as Warren Buffett said about one of his earlier investment mistakes (selling a company too early). I think this will be the case for most of the Canadian oil and gas complex.