Sodastream (Nasdaq: SODA) is an Israeli company that markets those “make it at home” carbonizers where you can make frizzy water, juices, and so forth, at home. Pepsi announced it would be buying it out for $3.2 billion.

What’s interesting is the financial history of the company:

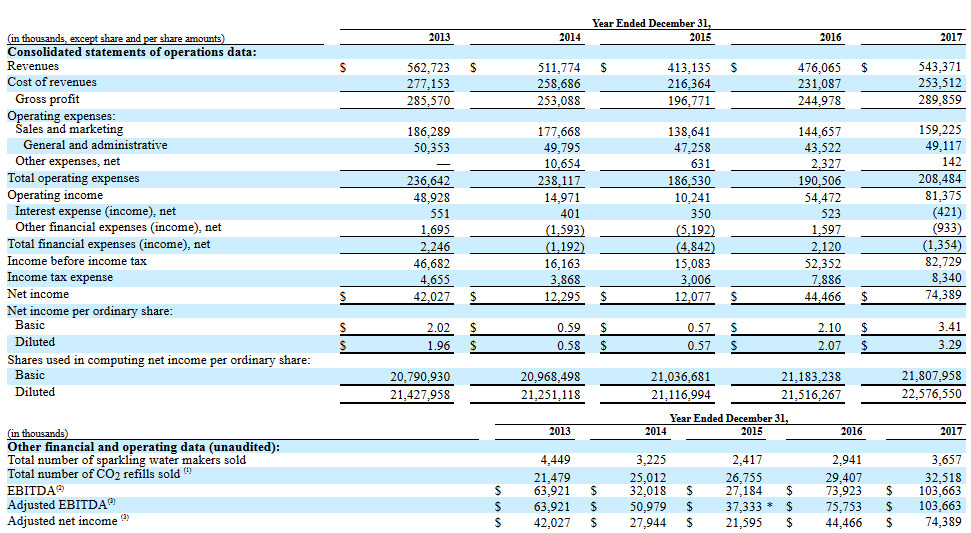

From 2013 to 2015, the company actually had declining revenues (down over a quarter) for a couple years and their profit levels went down as well. However, in 2016 they got back on track and managed to find a way to sell more and do it more profitably.

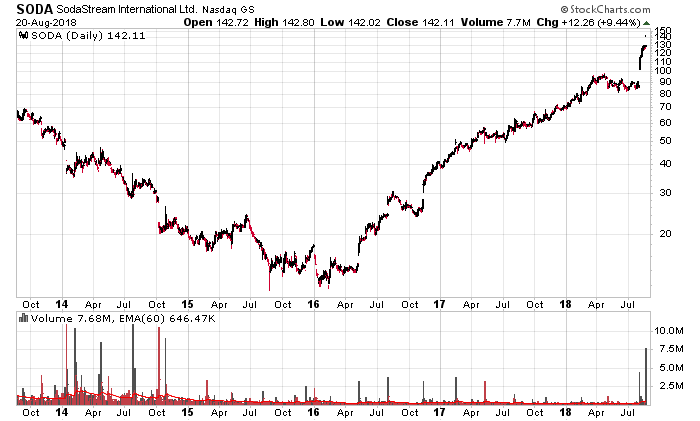

When looking at the stock chart:

Clearly in the middle of 2015 to the beginning of 2016, when things were at their financial worst, the market had valued SODA like it was some fad cupcake stock (wiki), but this would have been the perfect time to buy. A well-timed $12 investment would have turned into $142 presently.

The financial metrics of SODA at the end of 2015 (ended 2015 at $16 but crashed to $12 in January and February 2016):

Price/Sales – 0.83

Price/Earnings – 29

Today, Pepsi is paying (using 2017 financials, please realize I’m taking a shortcut and not using Q1 or Q2-2018 figures and taking the past 12 months) a Price/Sales of 5.9 and a Price/Earnings of 43.

Incredible. Let that sink in for a minute since people buying into Sodastream in late 2015 or early 2016 have made a fortune.

I’ll note that the balance sheet of SodaStream is not that special – it has a bit of cash in the bank, and no significant debt. They are not a book value play at all. The balance sheet (other than internalized Goodwill) is not a factor at all in this investment.

Finally, I will leave this following comment about investment psychology: Imagine you were convinced that Sodastream was going to turn around and start making significant amounts of money again at the end of 2015. You bought shares at $18 and took a heavy position in December 2015. Just a month later, your position was down to $12/share and it is a third (33%) under water. At that time, you must be feeling pretty stupid about your investment, not knowing that it would skyrocket over the next two years. The psychology of investing is a very odd one – at that point of maximum pessimism (at $12) people would probably question their own investment decision, whether the market sees something they didn’t. There were probably people that bought in at $18 and sold out at $12 because they couldn’t take a 33% loss on the way up to a subsequent 1,100% gain.