After the news that the Minister of Finance, Bill Morneau, will be selling his remaining stake in Morneau Shepell (terms and conditions to presumably not disclosed), it was time to look at the company. Whenever you hear of anybody forced to liquidate a stake in a company (especially through a margin call) it is always time to look to see if the underlying company can be bought for cheap. When something like this becomes too public (which I believe this news would qualify as), the opportunity to take advantage is diminished, but it is still worth examining.

There are two issues trading on the TSX, the equity (TSX: MSI) and a $86 million convertible debenture (TSX: MSI.DB.A) that matures on June 30, 2021; coupon 4.75%, conversion price $25.10.

I’ve examined the June 30, 2017 financial statements. The corporation has about 55.7 million shares outstanding, diluted.

Valuation

On the balance sheet, the company is primarily financed with debt. Book value is $366 million, but $543 million of this is in goodwill and intangibles, which leaves a negative $177 million equity balance. This, in addition to working capital, needs to be paid for with debt financing. They have a $300 million available credit facility, and are currently utilizing $186 million. They also have the aforementioned $86 million in 4.75% convertible debentures outstanding. This financing is very cheap – the bulk of the credit facility is at Banker’s Acceptance rates plus 1.45%. Overall, the company is financed with very inexpensive debt financing. If at some point in the future financing costs were to increase, this would put considerable stress on the balance sheet and would be disruptive to shareholders if it occurred.

Income-wise, the company is stable and profitable. For the first half-year, they made $36.1 million before interest and taxes, and net was a shade above $20 million. Cash-wise, they are performing slightly worse than their income statement (operating cash flow was $15 million for the first half). Their dividend payout amount was $21 million for the half, and thus when accounting for capital asset acquisition and other business acquisitions, they are currently a cash negative entity unless if they can curtail their cash outflows.

The market capitalization of MSI is $1.1 billion and for an entity that has a negative tangible book value and only flowing (making some paper napkin adjustments that I will omit from this analysis) about $45 million annualized cash flow, does not make them a compelling investment at current prices. If the company’s equity traded around the $500-550 million level (about half of what it is trading for currently) I might get interested, but I do not see this as a probable scenario.

The convertible debenture is trading at 105 cents on the dollar (effective yield is 3.2% assuming maturity). Given the elevated equity valuation, the market is clearly pricing in some call option value in the debt, but given the high equity valuation I would not consider this debt for purchasing at existing valuations.

Minister of Finance Sale

Over the past month, about 50,000 shares of MSI trade daily. The Finance Minister, from an April 2, 2015 SEDAR filing (Management Information Circular) owns or controls or directs 2,247,812 shares of the corporation. This is presumably through the family trust that is speculated around with media, held in an Alberta corporation.

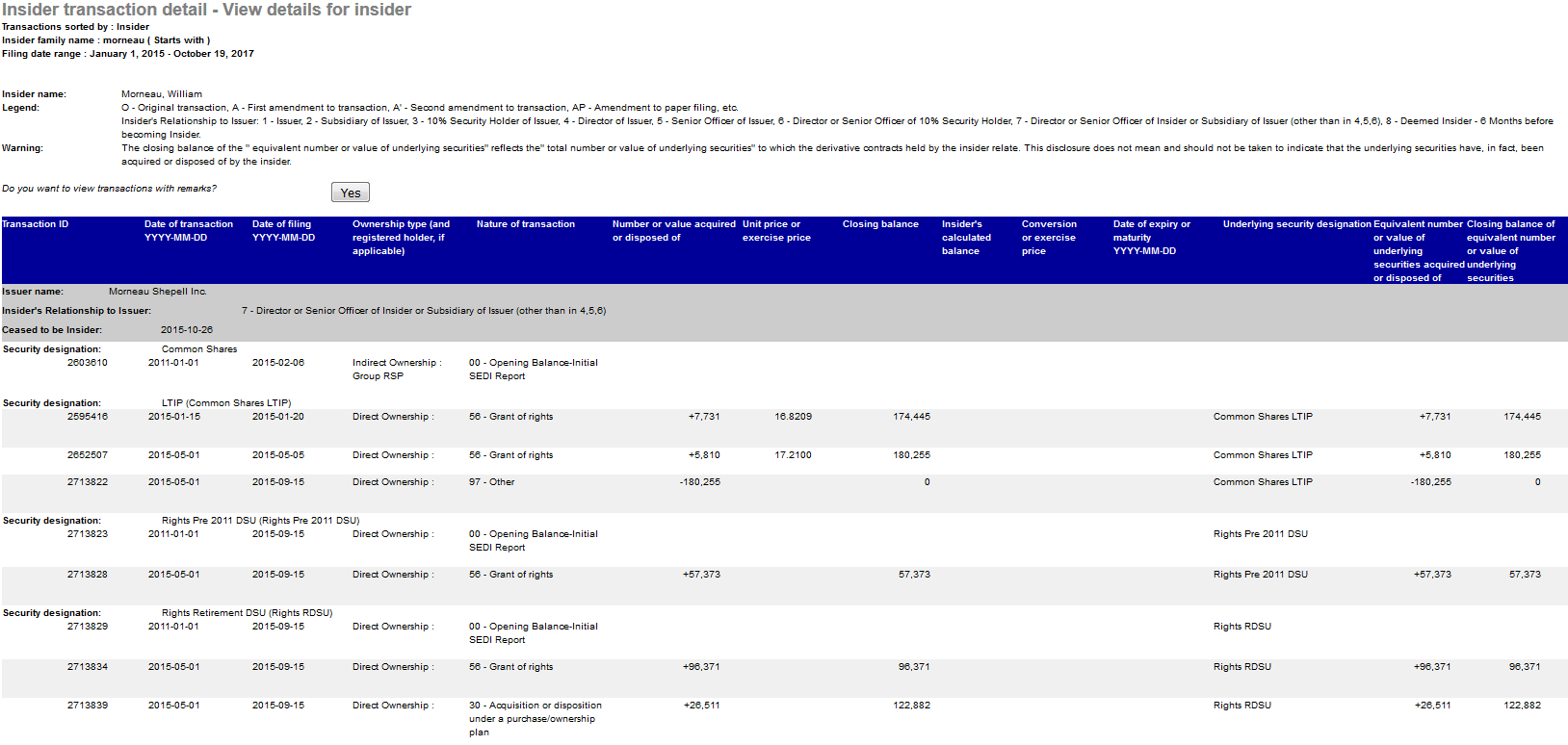

Where things look odd is when I look at his profile on SEDI (profile ID WMORNEA001) – He ceased to be an insider on October 26, 2015. According to SEDI filings, filed on various dates in 2015, he owned/controlled long term incentive plan shares and deferred share units, but there is no evidence on SEDI that he owned or controlled any common shares of MSI, which I find very odd and mysterious as it does not reconcile at all with the April 2, 2015 management information circular.

My big question: is the non-disclosure of the family trust an Ontario Securities Act violation? If Morneau had control over a larger number of shares than declared on his SEDI disclosure, is that not a non-disclosure that would be subject to penalties? A competent securities lawyer or somebody better versed in this section of law than I am would be able to answer this.

(Addendum, October 26, 2017: Turns out I totally missed the entry for his numbered Alberta corporation’s holdings of 2 million shares – so this was disclosed – back in 2011)

Also I’m cynically concluding that given the over-valuation status of MSI, the Finance Minister is also conveniently choosing this moment to unload shares.