Kinder Morgan Canada (TSX: KML) has agreed to be taken out by Pembina Pipeline (TSX: PPL), subject to a 2/3rds shareholder vote of KML holders, which will most certainly be approved. Details on this news release.

KML shareholders will get 0.3068 shares of PPL, which based on the closing price today (not the date of announcement) is about CAD$15.06/share for KML.

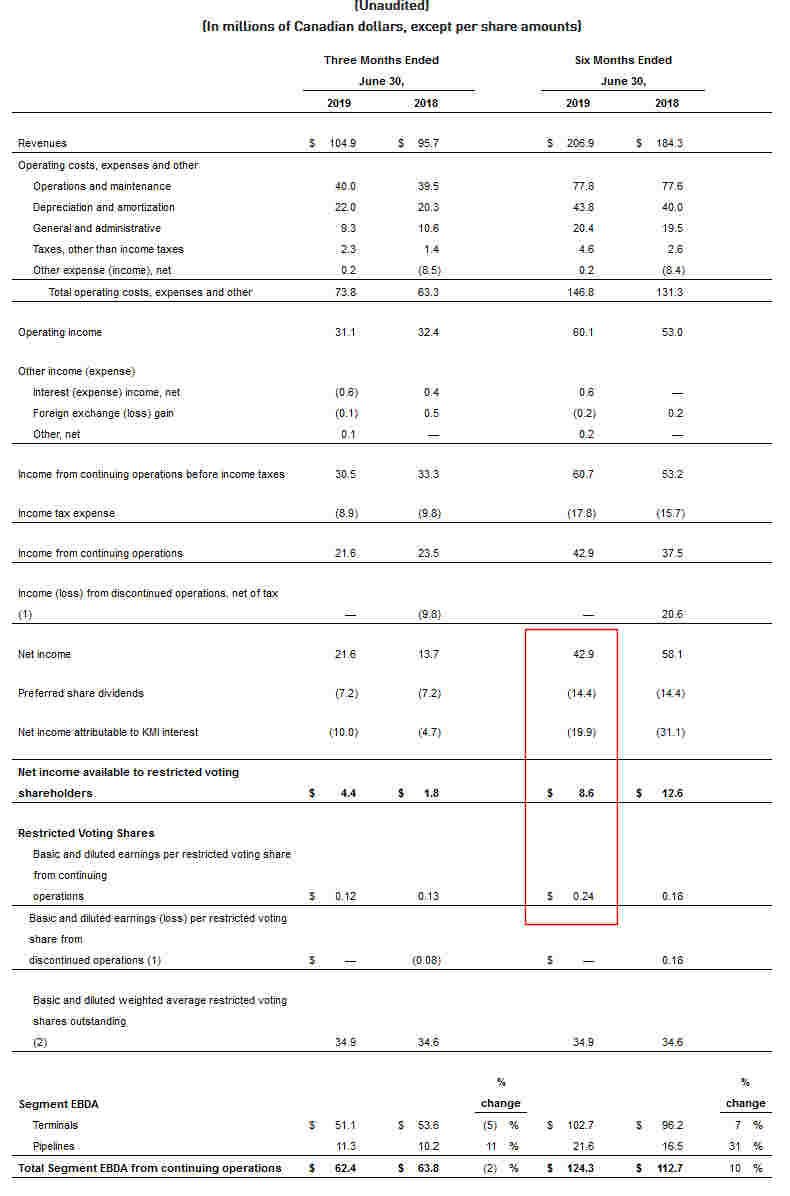

My comments are the following:

1. I thought this would happen in 2020 – my guess is while doing the strategic review they received a bunch of low-ball offers (and did not take any), but after the review ended they received a credible offer which was close to the initial KML IPO price of CAD$15/share (guessing their target price).

2. With regards to the preferred shares, I will point out that PPL has two preferred share series with minimum rate resets: PPL.PR.K (575bps, resets at +500bps with a 575bps mininmum rate) and PPL.PR.M (575bps, resets at +496bps with a 575bps minimum rate). Both trade above par value and both reset in the middle of 2021.

KML.PR.A (525bps, resets at +365bps with a 525bps minimum rate) and KML.PR.C (520bps, resets at +351bps with a 520bps minimum rate) are significantly worse featured – a reset rate of about 140bps adverse and a minimum rate of 50bps adverse. Both are trading slightly up (about a dollar) to ‘synchronize’ with the above – as PPL is a better credit.

Note that PPL is under no obligation to take out the preferred shares at par. Holders of KML preferred shares can keep clipping their coupons and have a little more confidence that the size of PPL will back it up.

3. Pembina is in a great position to take over the Trans-Mountain pipeline project (KML’s Vancouver terminal and Edmonton storage project synergize greatly with the pipeline). Although they claim they are not interested in it due to the obvious political mess, you can be sure if the Canadian government is going to give it away for cheap, Pembina will be right there bidding.

As such I think PPL was a great strategic buyer for these assets.