Most corporations that specialize in maintaining equity portfolios typically trade less than their component parts, simply due to the control issue. Shareholders generally have little control or say on when the company can reach their purported net asset values. Management usually has an incentive to not sell off their companies so they can collect salaries and/or benefits and/or power that comes with control.

As a result, it is a very relevant consideration before investing in such vehicles that the incentives of management are in line with your incentives (presumably as a minority shareholder). Some managements do care about their overall shareholder base (Berkshire presently I would judge to be part of this category, although they are much more of an operating company than most think), while most generally regard minority holders as an annoyance to be mitigated. It is rare where minority shareholder groups will organize to a point where a credible proxy fight can be contested, but such contests are expensive and usually the bias is toward incumbent management. A good example of a failed proxy fight was the contest for Aberdeen International (TSX: AAB) in early 2015 (a very brief legal summary is here).

Aberdeen was a notable case where it was trading far below its net asset value and the share structure did not have super-voting shares. The dissident group failed to accumulate enough support and shares to overthrow the board. Aberdeen at that time was trading at 15 cents a share and the book value was roughly 40 cents. Today they are down to a market value of 5 cents per share.

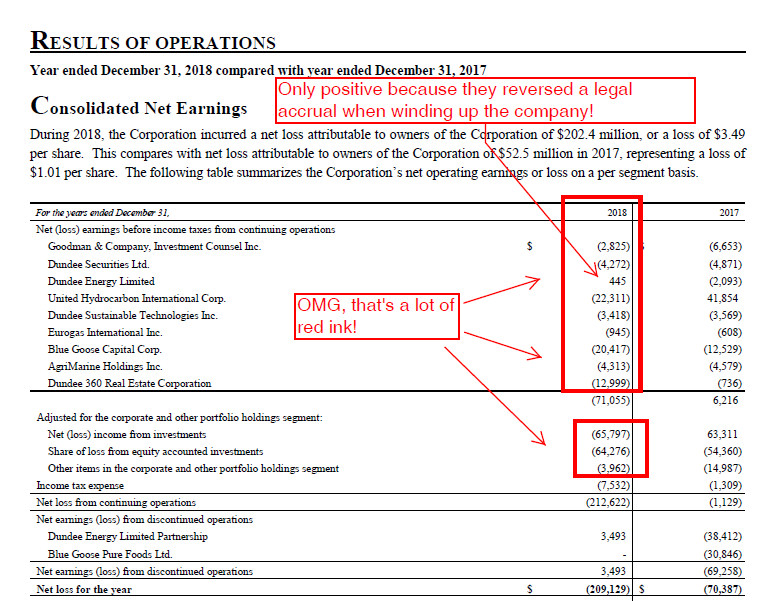

There are plenty of other cases to examine with these types of companies. Dundee Corporation (TSX: DC.A) is a conglomerate with consolidated and non-consolidated investments and has been trading below book value for a considerable period of time. In their last annual report, I highlight the salient page which shows that their operating entities are not doing too well:

Dundee is a dual class structure, with the founding family controlling the entity via super-voting shares. In order to resolve a situation with a redeemable preferred share issuance (which I have written about in the past) they also notably diluted their shareholders – issuing about 42 million shares to go from 61 million to approximately 103 million shares outstanding effectively – at a conversion price of $2/share. After this conversion, the parent company will hold no material debts and management will have a lot more time to be able to figure out how to transform the operating businesses into profitable entities. Presumably until this happens, Dundee will be trading under book value.

The last entity I will point out is Difference Capital (TSX: DCF). They were notable with having “Dragon’s Den” titan Michael Wekerle being their original CEO and lead investor and they invested in a whole smattering of private placements and various business ventures.

This didn’t quite work out for them for the majority of their history. In 2018, they able to focus on monetization of their portfolio in order to mostly pay off a convertible debenture. The remaining part was financed with a 12% secured loan which was partly paid for by insider money. In their year-end of 2018, they held a net asset value of $7.20/share on their financial statements and this was contrasted with a $3 share price (indeed, shortly after the new year, they executed on an asset disposal that spiked their share price up to $4) – hardly a risk for insiders to take when they were first in line on security and taking a nearly guaranteed 12% return – the shareholders are the ones effectively paying for this.

The final monetization of their company was announced on April 15th – however, it was to another company called MOGO Finance Technology (TSX: MOGO) which is chaired by Wekerle and 22.4% of MOGO is already owned by DCF.

DCF is nearly majority controlled by Wekerle (47% via a holding company that he wholly owns). Thus, a DCF shareholder has to ask whether their interests are aligned with his.

The agency issue is whether DCF minority shareholders benefited from the MOGO transaction. The obvious answer, when looking at the financial situation, is no. It reminds me of what Elon Musk did when he merged SolarCity and Telsa together – SolarCity was about to financially fail, but Musk wanted to fold it into Tesla to avoid the negative attention that such a failure would cause, with Telsa shareholders picking up the bill to deal with the entrails of that transaction.

Instead, this transaction was likely to give MOGO some financial breathing space as they were effectively buying the residential value of DCF’s private equity portfolio and more importantly, cash.

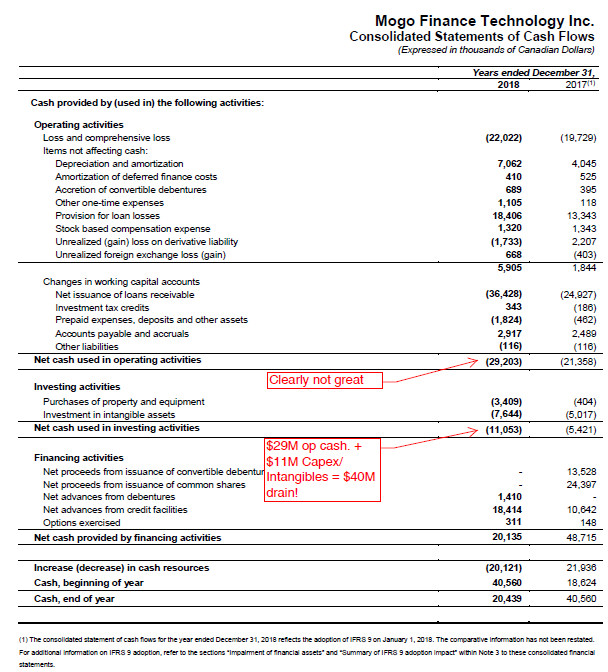

MOGO is bleeding significantly serious amounts of money:

The cash shortfall is significant. Operationally, MOGO is not in terrible shape – they reported an operating income loss of $4 million in 2018. The real deficit in MOGO is the cost of their capital. They have $75 million outstanding on a credit facility, $42 million in non-public debentures (ranging from 10% to 18% interest), and $15 million in 10% convertible debentures (TSX: MOGO.DB). When reading the fine print on the credit facility, the following is the key paragraph (note the underlined):

On September 25, 2017, the Company finalized a new senior secured credit facility of up to $40 million (“Credit Facility – Other” and, together with the Credit Facility – Liquid), which was used to repay and replace Mogo’s previous $30 million entered into on February 24, 2014 (“Credit Facility – ST”). This transaction resulted in the extinguishment of the Credit Facility – ST. On December 18, 2018, the Company increased the borrowing limit on the Credit Facility – Other from $40 million to $50 million. The facility bears interest at a variable rate of LIBOR plus 12.50% (with a LIBOR floor of 2.00%) up to the first $40 million of borrowing, a decrease from the variable rate of LIBOR plus 13.00% (with a LIBOR floor of 2.00%) under the Credit Facility – ST. The incremental portion of facility borrowings above $40 million bears interest at a variable rate of LIBOR plus 11.00% (with a LIBOR floor of 2.00%). Consistent with the previous facility, there is a 0.33% fee on the available but undrawn portion of the $50 million facility. The Credit Facility – Other matures on July 2, 2020, compared to the maturity date of July 2, 2018 under the previous facility. The amount drawn on the new facility as at December 31, 2018 was $44.3 million (December 31, 2017 – $28.8 million) with unamortized deferred financing costs of $0.2 million (December 31, 2017 – $0.2 million) netted against the amount owing.

You’re not going to get rich borrowing money at LIBOR plus 12.5%! Indeed, as a percentage of revenues, interest expenses are 28% – they will never show a profit at that level of interest bite.

Hence the presumed justification for the merger with DCF – Michael Wekerle has invested significant resources into MOGO. MOGO is borrowing money at exorbitant rates and DCF will add some assets to MOGO’s balance sheet, which can eventually be liquidated for desperately needed cash.

Does this in any way benefit non-controlling shareholders of DCF? Not at all. This explains why DCF traded down after the transaction and MOGO traded up.

Currently, MOGO has a market capitalization of $80 million (this is after it received a good 15% rise after the DCF announcement). Will they be able to find cheaper financing? Most of their debt matures in 2020.

But either way – this is yet another example of making sure to check the motivations of controlling shareholders before you jump on board – you might find they will make decisions that will have little to do with adding value to the stock and instead use the entity for other strategic purposes.