Apparently some institutional shareholders are feeling the political pressure of the company’s ridiculously high executive compensation schemes. They’re voting against the “say on pay” resolution on the upcoming AGM.

Major Bombardier Inc. shareholder and supporter Caisse de dépôt et placement du Québec is voting against the company’s executive pay practices at its coming shareholder meeting.

It’s one of a number of major North American pension plans that intend to rebuff Bombardier’s compensation program. Some, including the Caisse, have grown sufficiently discontented to oppose reappointing directors to the company’s board.

Bombardier, like most major Canadian companies, submits its compensation program to shareholders for a non-binding “say-on-pay” vote at its annual meeting. Canada Pension Plan Investment Board (CPPIB), British Columbia Investment Management Corp. (BCI), as well as two major pensions from California and one from Florida, also say they are voting “no” Thursday.

At issue this year is Bombardier paying former chief executive Alain Bellemare a severance package of US$12.35-million when he was terminated in March, as well as promised future special payments and potential severance packages to other top executives when a deal to sell the company’s train division closes in 2021.

This is purely political posturing to the public to justify holding Class B shares (2.1 billion outstanding) in the company. Bombardier’s Class A shares (309 million outstanding) have 10 votes each, which give its holders effective control of the company. Bombardier’s Class A shares are currently trading at about a 30% premium over the Class B shares, so the market does ascribe some value to the voting component.

There is little remedy for the subordinate shareholders other than to sell if they wish to voice their opinion. This happens in any dual-class share structure company, where typically the founders get the supervoting majority to stack the board. You have cases like Berkshire (NYSE: BRK.A) and Fairfax (TSX: FFH) where you are being a silent partner to Warren Buffett/Prem Watsa, but you also have cases like Dundee (TSX: DC.A), which have made disastrous capital allocation decisions in the past decade (will they get their act together for the next one? Insiders are at least buying now). There are also firms like Biglari Holdings (NYSE: BH), where the controlling shareholder basically has open contempt for its subordinate shareholders – don’t like me? Go ahead and sell! Zuckerberg at Facebook (Nasdaq: FB) also has expressed the same sentiment – my way or the highway.

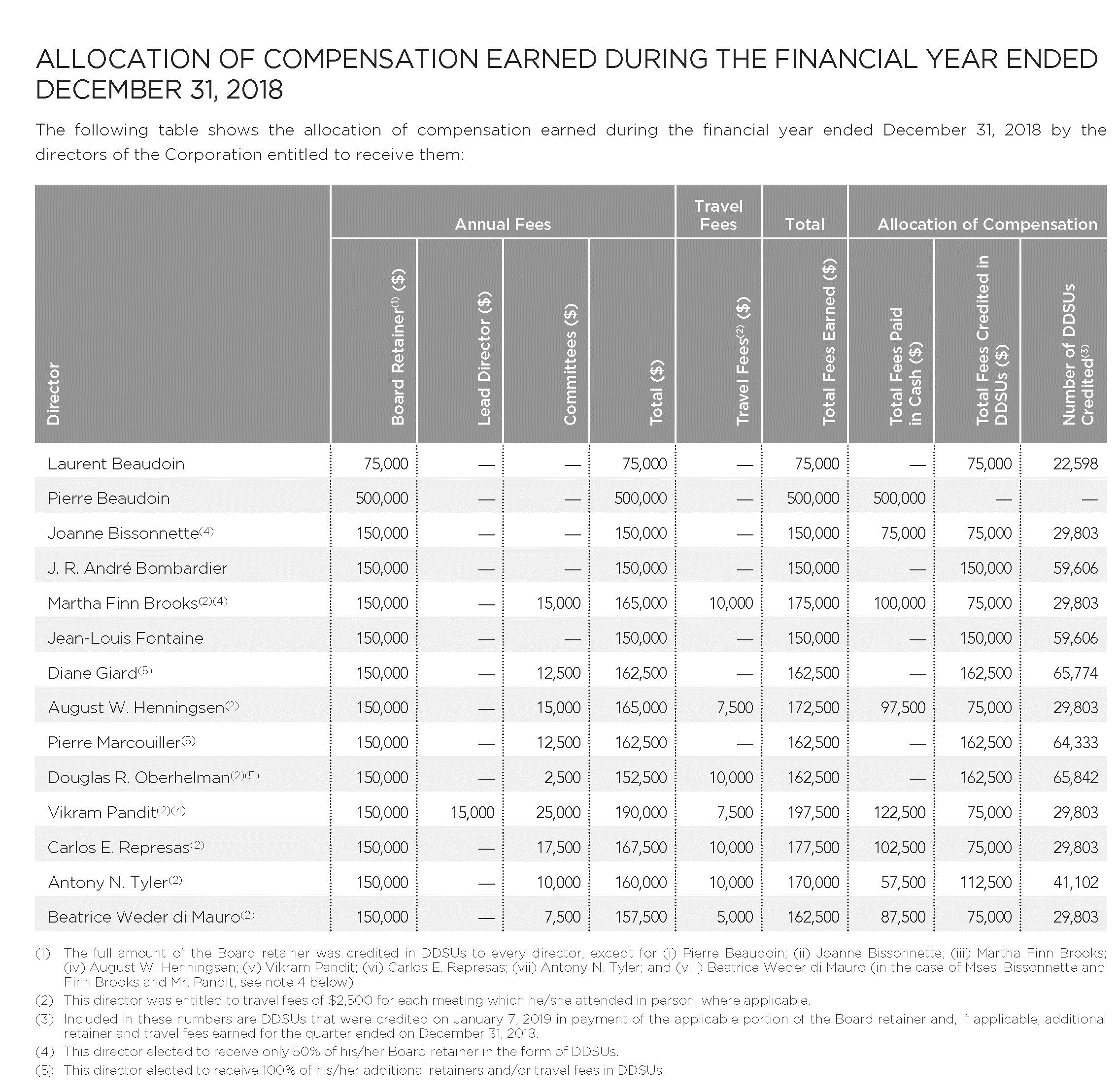

In all of these cases, investors, especially institutional ones, should know what they have gotten into. This doesn’t mean they can’t complain, but when it comes to exercising power to compel the board of directors to tell management to change their practices, the influence is very weak since controlling shareholders will always be able to replace potentially dissenting directors with those that favour their interests. In the case of Bombardier, who wants to give up $150-$190k for being a human rubber stamp?

(By the way, this board is far too large).

The only way to get any sort of leverage on an entrenched board is to own enough of the debt in a distressed situation, and then you will be able to get enough attention of management by the time the maturity comes to extract better terms. But these situations are rare, and they more often end up with management engaging in asset stripping and other extraction activities to the detriment of both shareholders and debtholders alike before they finally lose control.