(Thanks to Marc for commenting on this offering in the Debentures comments section)

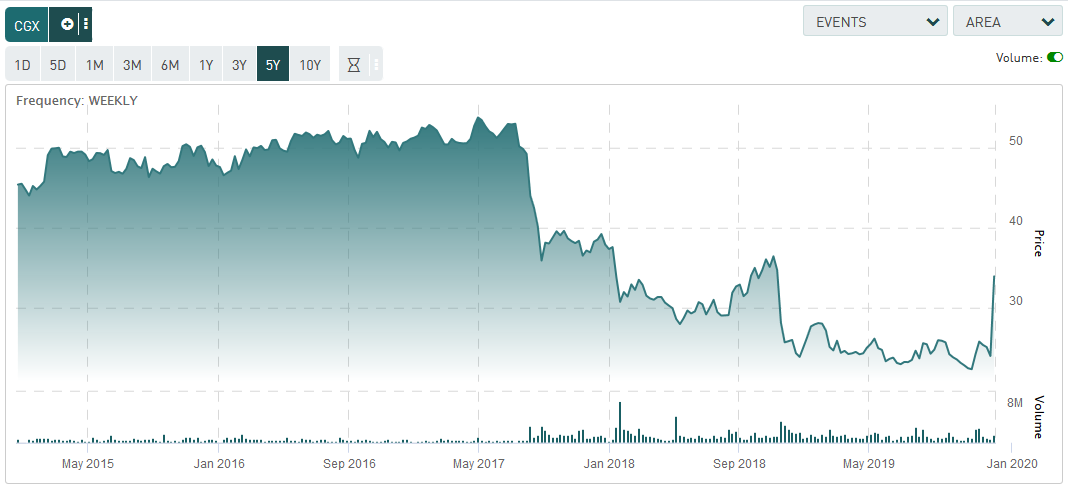

Cineplex (TSX: CGX) was about to exit the escape room for CAD$34/share. Their timing was nearly perfect (December 16, 2019 announcement), but COVID-19 struck during the closing process. Now they’re a $8.40 stock and their business has been decimated due to the reaction over COVID-19 – movie theaters were right up there with cruise ships as being COVID disaster zones.

However, yesterday they raised $275 million in unsecured convertible debt financing! 5.75%, convertible at $10.94/share.

Quite frankly I was surprised. Maybe it is a sign of how frothy the market environment is. Their last published financial statements were from March 31, 2020 and I will dissect them:

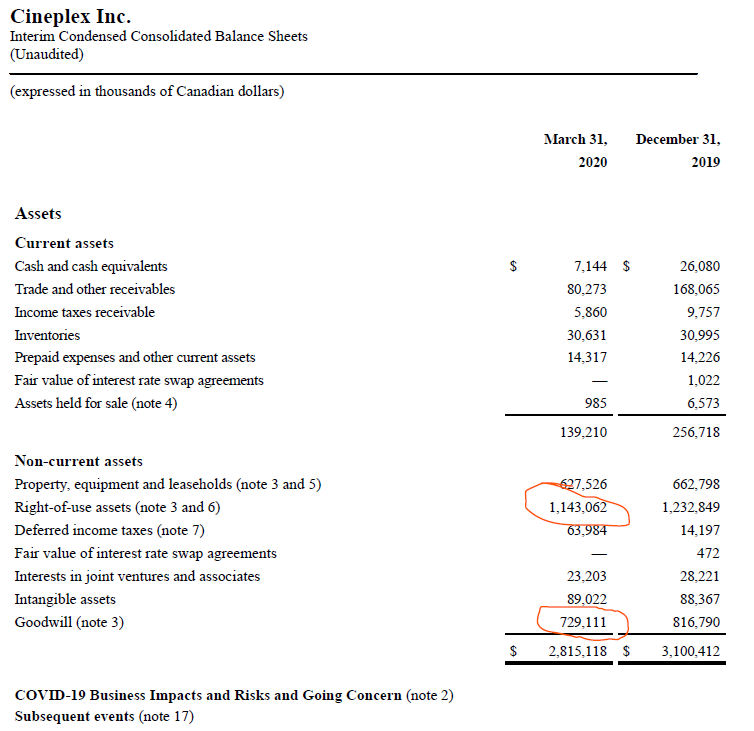

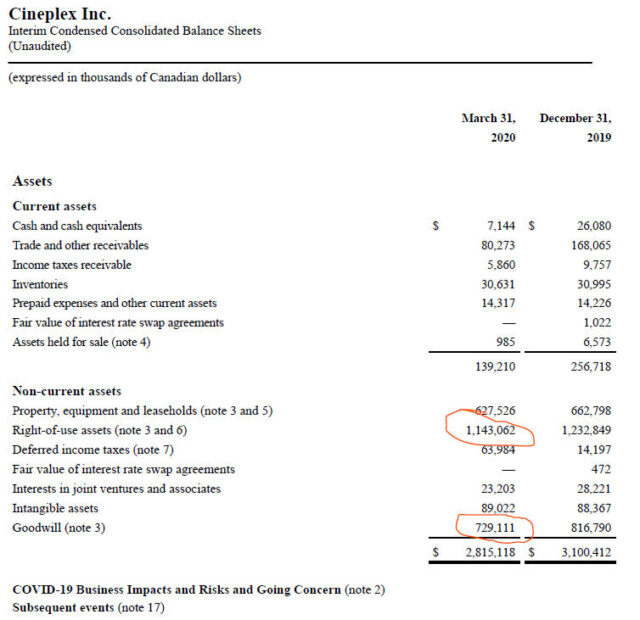

Balance sheet, assets:

The highlights here are little cash, coupled with a large amount of right-of-use assets (leases) which are worthless if you can’t perform business in them, and about $820 million in intangibles and goodwill. In relation to their $412 million of equity (below), this pulls them very deeply into a negative book value, which is generally my metric to value companies as a cash flow vehicle.

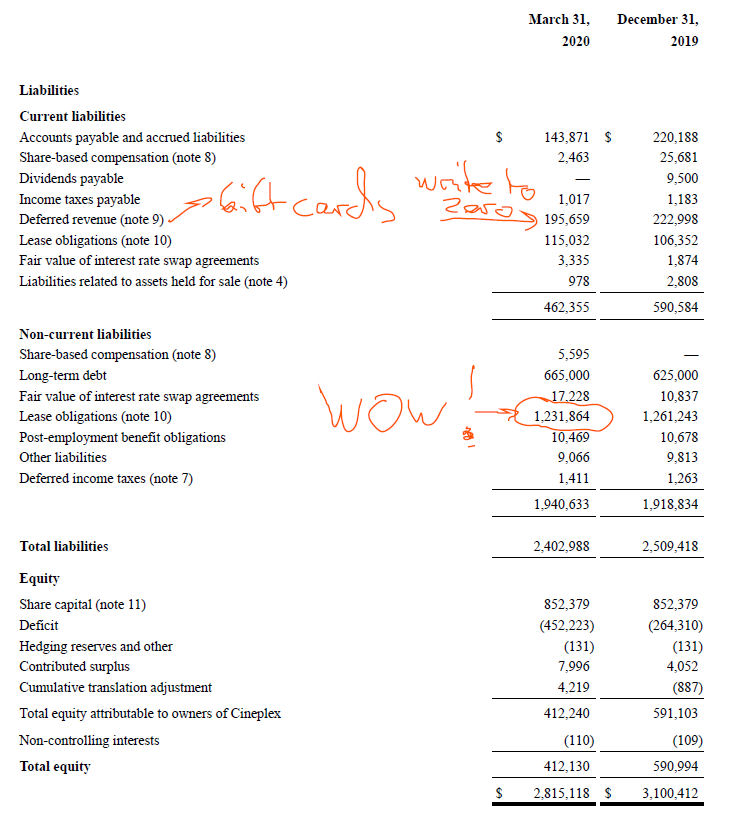

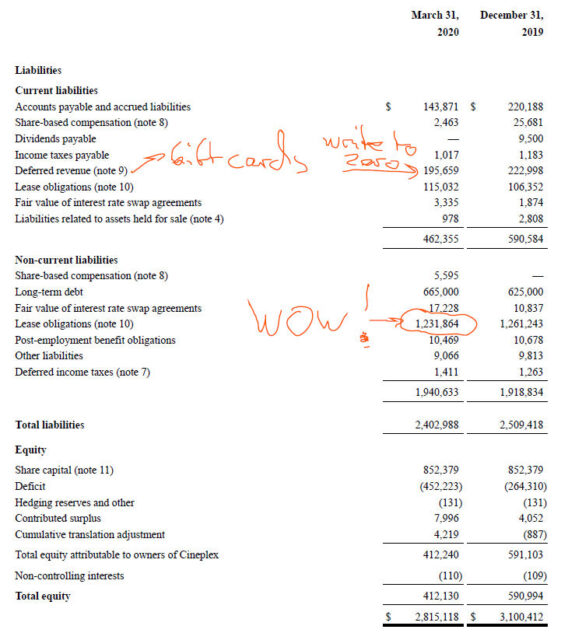

Balance sheet, liabilities plus equity:

There’s a few adjustments to be made here. One is that the “deferred revenues” is mostly unused gift cards, which means if you haven’t used them yet, this is where they are represented on the books. If the business isn’t operating, this “liability” virtually amounts to a zero cost equity injection by hapless consumers.

We see the discounted cost of lease obligations, for the first year it represents a $115 million outflow. This is a large number but it isn’t crushing. These leases are long-term in nature, which is the “WOW” $1.23 billion figure. Most of this is property and a tiny bit is equipment.

Finally, they do already have $665 million of debt on the books.

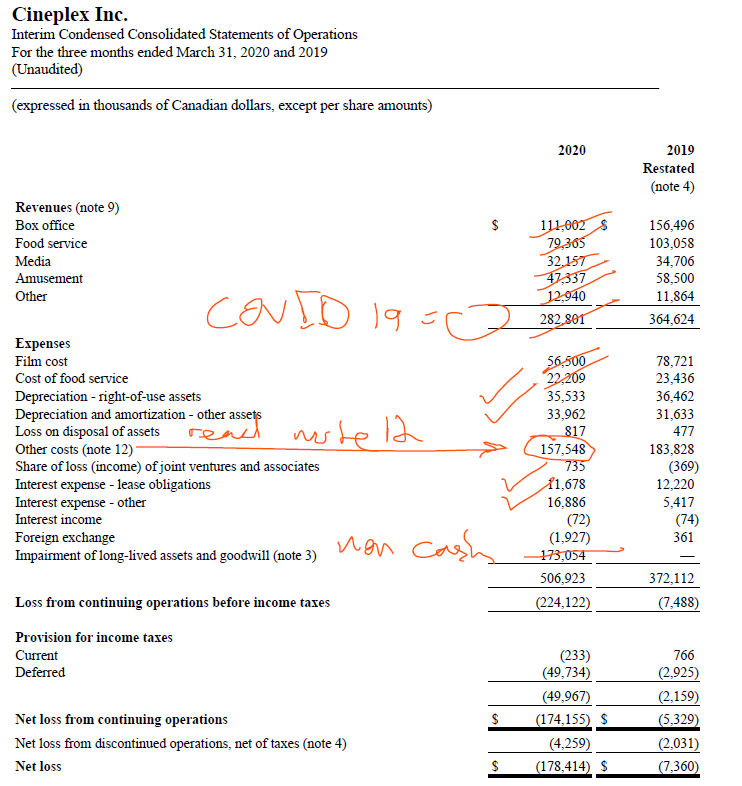

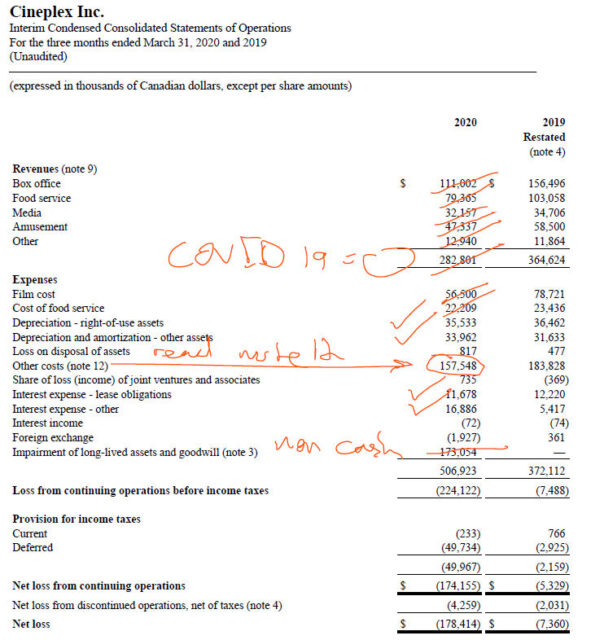

Income statement:

Note the industry is seasonal in nature, so taking one quarter and extrapolating it to the full year is not appropriate.

I work through the line items and I do not see much in the way of revenues when the business is closed due to COVID-19. I then try matching up the costs that would be reduced as a result of COVID, and most of this is the “Note 12”, and lease (depreciation of right-of-use assets) costs, coupled with depreciation of film rights, and financing expenses.

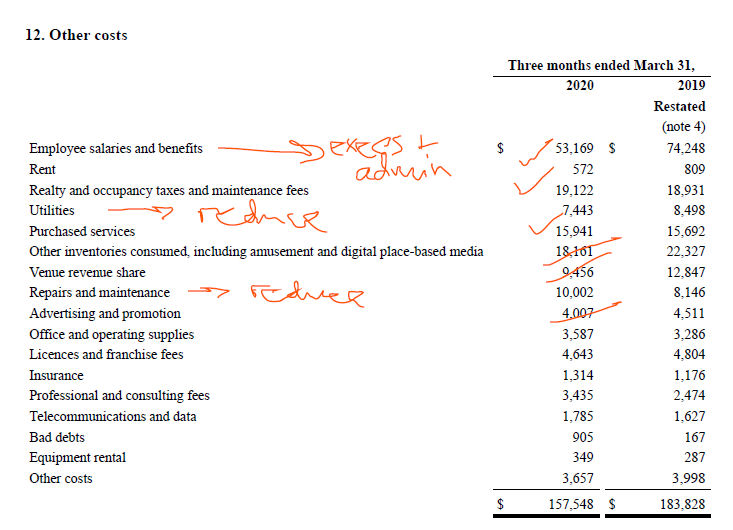

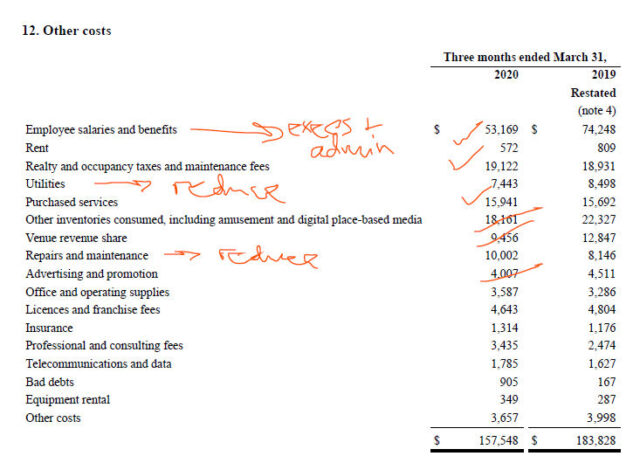

We look at this “Note 12” which represents a large expense:

Presumably the executives and administrative staff of the corporation are still employed, but the various people involved in box office operations (e.g. retail cashiers, cleaners, film technicians, etc.) are off on CERB. I don’t know what fraction of the $53 million are ‘baseline’ employment expenses. I’d guess they’d be able to shed about 80% of their employment expenses?

They will still have to pay realty fees, occupancy taxes, and so on.

Just as a very broad proxy, let’s say that Note 12 expenses can be reduced to $50 million a quarter.

So just as a ballpark figure, when incorporating lease expenses and financing expenses, the entity is burning about $100 million a quarter, very roughly, when it has zero revenues. They might have given some guidance in their last quarterly conference call (I have not paid attention).

The fact that they can raise $275 million, unsecured, and at such a low rate of interest I find amazing. Am I that seriously out to lunch on the valuation of Cineplex?

I haven’t even evaluated the question of whether people actually want to go back to movie theatres, but this is an age-old question that has predated COVID-19. I recall a posting back in August 2014 where I was wondering how the heck they were doing so well despite the internet age.