A couple pieces of evidence to indicate the malaise in the Canadian oil sector.

First one was Pengrowth (TSX: PGF), who announced:

The Company’s $330 million Credit Facility (all amounts in Canadian dollars) is provided by a broad syndicate of domestic and international banks and had a scheduled maturity of September 30, 2019. The lenders have agreed to provide the Company with a 31 day extension of the maturity date under the Credit Facility to October 31, 2019 with a maximum facility draw of $180 million under the Credit Facility and a $5 million Excess Cash provision.

Holders of the Secured Notes have agreed to the extension of the Credit Facility and to a 31 day extension of the maturity date under the October Notes to November 18, 2019.

The Company will continue to operate its free cash flow positive business as usual. This short-term extension will allow the Company to continue to advance discussions with its lenders and noteholders with the objective of completing a long-term extension transaction. The mutual goal of Pengrowth and its senior debtholders is to negotiate a three year extension that allows the Company the flexibility to reduce its outstanding debt with the benefit of additional time and improved market conditions.

The Company believes it has made significant progress with its lenders and noteholders on a number of key areas in respect of the potential extension transaction, but there remain ongoing detailed discussions which require additional time. A transaction may result in dilution of the outstanding common shares of the Company (with an associated impact on the value of such shares) as part of any consideration provided to affected lenders and noteholders. There can be no assurance or guarantee that a long-term extension transaction will be agreed to or on what terms.

Pengrowth has CAD$57 million (denominated in foreign currency) in secured debt that is due on October 18, 2019 which has been extended a month as a result of the above release. They also have significant debt in 2020 and 2022, and also a line of credit which was set to expire on September 30, 2019. Current debt outstanding is $362 million, and non-current portion is $340 million.

The only way the company could pay the upcoming bond maturity is by the extension of its term facility, which of course the banks are unlikely to give without security, but the security has already been pledged to the noteholders. So this is a very sticky situation where both secured entities (noteholders and credit facility) have an incentive to pulling the pin to getting instant payment. Pengrowth also has covenants relating to the secured notes that they are likely to break imminently (even though they were relaxed in the past).

This is not likely to end very well for Pengrowth shareholders. The only wild card here is whether Seymour Schulich (who owns 159,400,000 shares of PGF or about 28.5% of the company) will be asked to put up a bunch more money to salvage his investment, which, needless to say, is seriously under water at the moment.

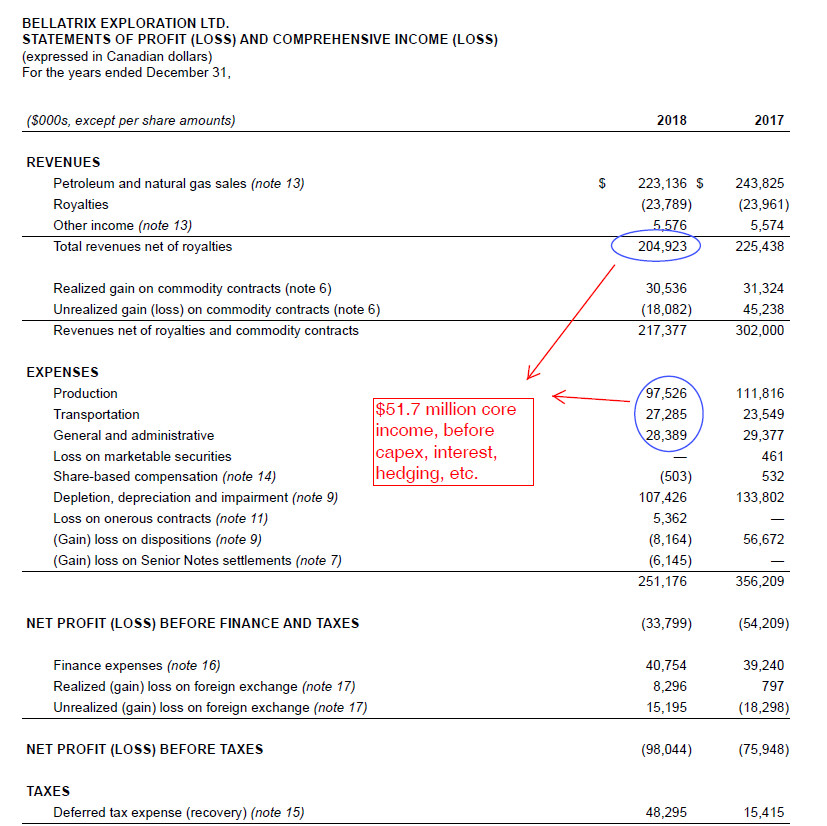

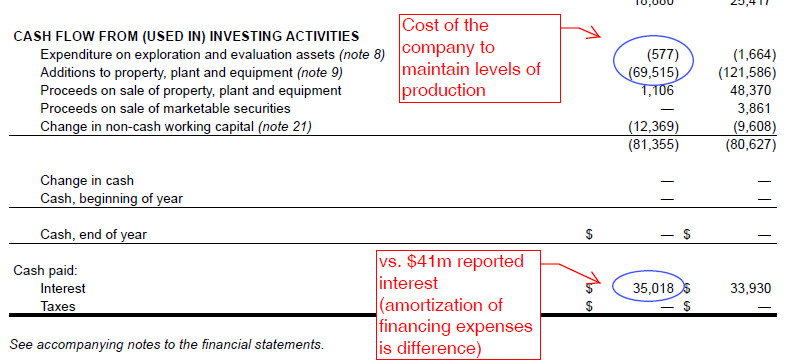

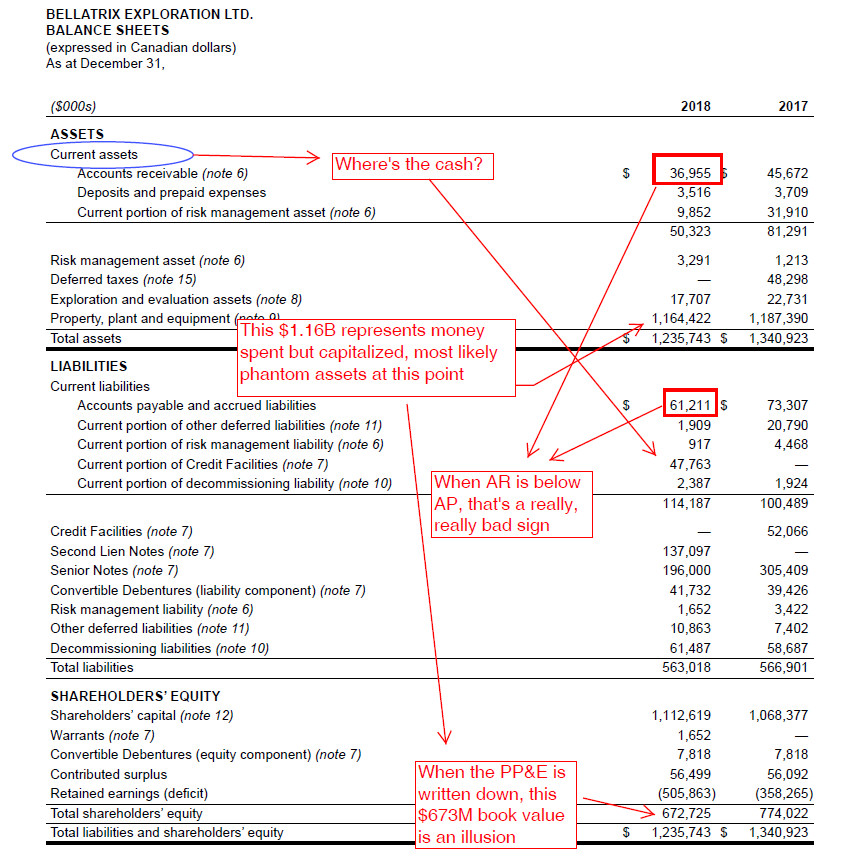

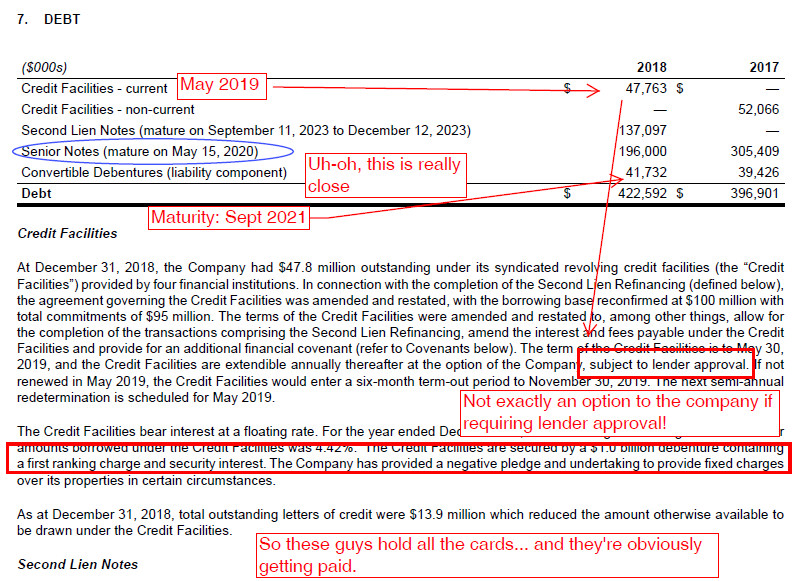

Second item: Bellatrix Exploration (TSX: BXE) went into CCAA today. Shareholders will probably get little out of it. While an energy company going into CCAA may not necessarily be unexpected news, the surprise here was that it took place after a recent capitalization (June 4, 2019). However, it is pretty clear in retrospect that the replacement of 4 of the 7 directors resulted in them changing gears and instead are representing the debtholders with this action.