The winner of the Genworth MI auction (presumably there were multiple interested partners) was Brookfield Business Partners LP (TSX: BBU.UN) at CAD$48.86 per share, for 57% of Genworth MI shares. Brookfield Asset Management owns about 80% of Brookfield Business Partners. I’m not going to dissect more of Brookfield’s capital structure or even the LP unit, but suffice to say, they have the assets to consummate the transaction, assuming they receive regulatory approval.

The transaction, if approved, will close sometime in the first half of 2020 and apparently will receive regulatory approval by the end of 2019. I had speculated earlier that Genworth would not receive more than CAD$55/share for the unit (and my initial opinion was CAD$50) and this appears to be right on the mark. Genworth MI’s stated book value was $47.17 at the end of Q2-2019, so Brookfield is paying a very modest premium over book.

Here’s the interest part of the release:

Brookfield Business Partners has also agreed, between now and the closing of the transaction, to provide Genworth Financial, Inc. with a bridge loan of up to US$850 million that is intended to be repaid from proceeds of the sale of its interest in Genworth Canada.

Genworth Financial has some solvency matters to deal with.

The other logistical matter for Genworth MI is that they share services with Genworth Financial for some business operations. This will have to be carved out and transitioned over with the takeover. In addition, it is not clear whether the senior staff of Genworth MI will go back to Genworth Financial, or whether they will stay with the MI subsidiary. When businesses are acquired like this, there is always an element of disruption, if not handled carefully!

As for the other 43% of Genworth MI, currently Brookfield indicated they do not wish to repurchase it:

Given the short time frame available to complete this transaction, Brookfield Business Partners has no current intention to make an offer for the balance of the outstanding Shares. Brookfield Business Partners may in the future consider the appropriateness of such an offer after discussion with Genworth Canada’s shareholders and other stakeholders.

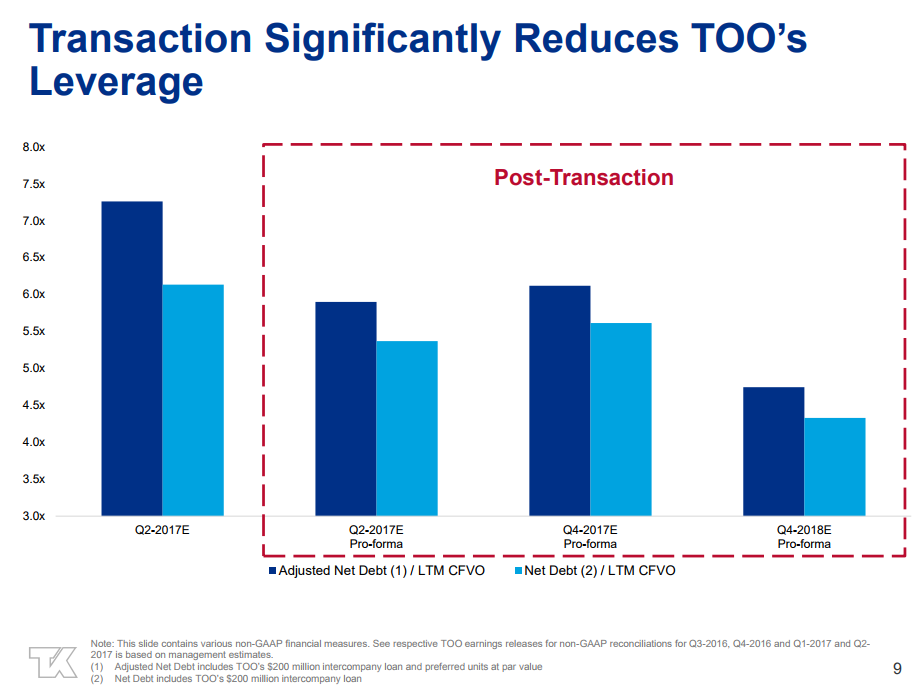

This may happen if Genworth MI starts to trade significantly under CAD$48.86. One needs to look no further than the treatment of minority shareholders of Teekay Offshore (NYSE: TOO) which are currently receiving a lowball offer for their shares.

I would suspect very limited upside for the capital value of Genworth MI shares at current market prices.