I last covered Aimia (TSX: AIM) last September and things have progressed from bad to just outright hilarious (unless if you’re a shareholder).

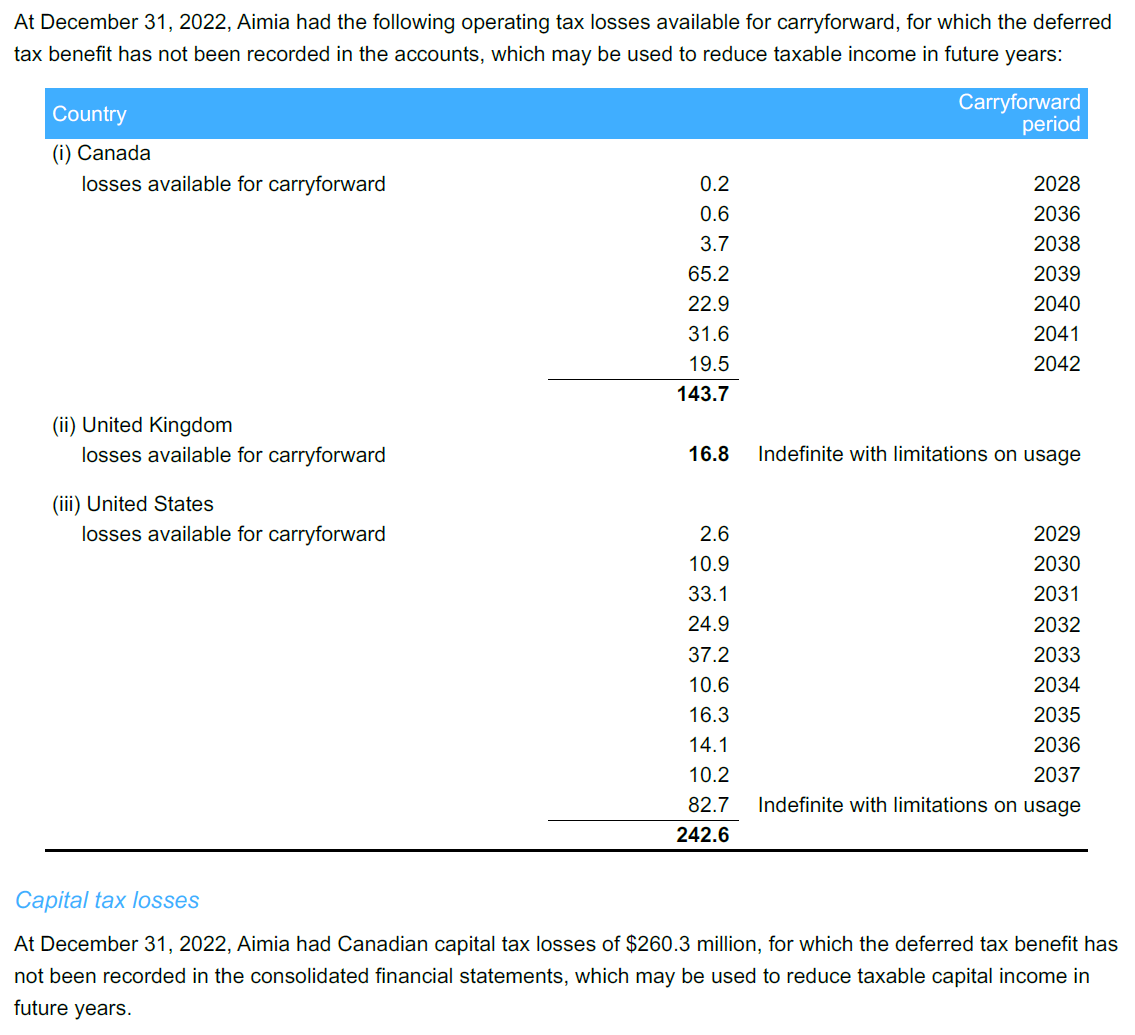

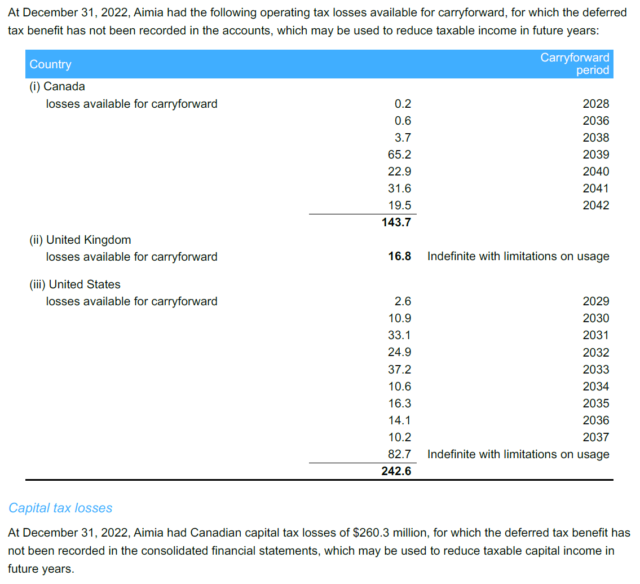

Aimia had raised nearly half a billion in cash from the disposition of one of their legacy business units, leaving their balance sheet relatively open for investment. The company’s stated objective was to invest such proceeds in such a manner that could utilize their extensive tax losses, neatly summarized by this page on their last annual report:

What does the corporation do instead?

Two headlines:

a) January 31, 2023: AIMIA TO ACQUIRE TUFROPES FOR $249.6 MILLION

Aimia Inc. (TSX: AIM), a holding company focused on long-term global investments, has announced today that it has signed definitive agreements to acquire all of the issued and outstanding shares of Tufropes Pvt Ltd. as well as certain business undertakings of India Nets (together referred to as “Tufropes” or the “Company”). Aimia will pay a purchase price of $249.6 million (1) on a cash-free and debt-free basis

…

A family-owned business founded in 1992, Tufropes is expected to achieve annual revenue of approximately $130 million (1) for the fiscal year ending March 31, 2023 , and industry-leading EBITDA margins of 18%.

b) March 6, 2023: AIMIA ANNOUNCES ACQUISITION OF BOZZETTO GROUP FOR $328 MILLION

The purchase price will be based on an enterprise value of approximately $328 million (1) . It is anticipated that the acquisition will be financed with a combination of cash and debt, with an expected level of debt of around 3x Adjusted EBITDA, or approximately $135 million . Bozzetto achieved annual revenue of approximately $326 million (1)(2) and Adjusted EBITDA of $47 million (1)(2) with an Adjusted EBITDA margin of 14.5% (2) for the fiscal year ended December 31, 2022 , with higher than 80% free-cash flow conversion (3).

Quick analysis

Acquisition (a) invests $250 million for [$130*18%?] $23.4 EBITDA margins. Assume no “I” and a combined TDA of 40% and that leaves $14 million net income. Tufropes is an Indian corporation.

Acquisition (b) invests $193 million cash ($328-$135) for an “adjusted” EBITDA of $47 million. Let’s ignore “adjustments”, and apply an “I” of $135*7%, and according to the press release, claims a “free cash flow conversion of 80%” which miraculously assumes that a multi-country specialty chemical business has little in the way of capital investment requirements. Somehow, I don’t think so. Looking at Chemtrade, for example, we have 43% of their 2022 EBITDA going to capital and lease and cash taxes. But they are a trust structure, so I would suspect that Bozzetto would be paying more than 50% of adjusted EBITDA on this, but let’s round to half and you get $23 million. Bozzetto is an Italian company.

Add these up, you get about $37 million on a $443 million cash investment or an 8.3% leveraged return. Not only that, but it is an incredibly tax inefficient way of utilizing the tax losses.

These guys could have bought CNQ and would likely do a lot better and gone through less headaches than dealing with jurisdictional headaches like the ones they’re entering in now!

Follow-through soap opera

Over the past half year, a Saudi-run capital corporation, Mithaq Capital, has acquired 19.9% of the common stock. Understandably they’re not happy with how present board management has handled the investment portfolio.

Aimia is holding their annual general meeting on April 18.

Mithaq released on April 6:

Mithaq is disappointed with recent events and has lost confidence in the Board and management. Mithaq believes that it would be in the best interests of Aimia to reconstitute the board and will vote against the re-election of David Rosenkrantz (Chair), Philip Mittleman , Michael Lehmann , Karen Basian , Kristen M. Dickey , Linda S. Habgood , Jon Mattson and Jordan G. Teramo to the Board at the Meeting.

The reasons underlying Mithaq’s decision to vote against the re-election of the Board include concerns previously raised with Aimia regarding capital allocation decisions relating to acquisitions.

Aimia management quickly rebuked and claimed it is taking action to “protect the integrity of the market”:

Over the past month, Aimia has been investigating the misuse of confidential information belonging to the Company and one of its affiliates. The misuse involved an insider who was a former member of the Company’s board of directors and a senior officer of the affiliate in breach of his legal obligations. The investigation also uncovered what Aimia believes to be undisclosed joint actor conduct relating to the acquisition and voting of Aimia securities.

Upon uncovering this misconduct, Aimia’s affiliate recently terminated the insider and Aimia reported its concerns about breaches of securities legislation to the relevant securities regulatory authority. The Company is considering all legal options available to it to protect shareholders and the integrity of the market.

Mithaq filed an official proxy statement on SEDAR (April 10, 2023) and there are many gems in there, but this one in particular was interesting:

Aimia’s current operating expense at the head office level is at an approximate C$15 million annual run rate, which is a grossly inappropriate set-up for an investment holding company of Aimia’s size. In addition to this, by bringing Paladin into the recently announced acquisitions, Aimia shareholders will be paying a 2% annual management fee and a 20% performance fee.

This makes the old corporate headquarters at the former Pinetree Capital (pre-2016, the current entity is parsimoniously run) look spartan by comparison.

Aimia on April 11:

Mithaq and its joint actors seek to control Aimia out of self interest

…

Aimia believes that these statements were made in furtherance of a self-interested attempt by Mithaq and its joint actors to acquire control of Aimia’s cash for the purpose of investing in the securities of poorly performing public companies held by Mithaq.

Of course there’s self-interest! They own 19.9% of the company. It indeed is quite ironic that one of the poorly performing public companies held by Mithaq is Aimia itself!

I am sure there will be more theatrics between now and the April 18th AGM. I do not expect a sane shareholder would vote in the incumbent board, but some shareholder votes in the past have surprised me!

In terms of how Aimia’s stock is doing, their preferred shares are trading at roughly a 9.5% reset yield. Definitely not enough compensation for risk in my books.

Also, if Mithaq is successful in taking over Aimia’s board, they have the unenviable task to undo the capital damage that has occurred. Basically they’d be taking over when the family silverware has already been ransacked.