Investing is a weird art in that you can be wrong with your theories but still end up ahead. The converse is true (although when you lose despite being correct, I must say it is a lot more annoying).

Ag Growth (TSX: AFN) announced they settled with their customers in regards to a three-year old incident involving an installation of a grain tower:

We are pleased to confirm that a mutual settlement agreement has been entered into with Fibreco that settles all matters between AGI and Fibreco relating to the Bin Incident. AGI expects to record an additional pre-tax charge of approximately $15.6 million in the second quarter of 2023 in connection with the Fibreco settlement, including insurance recoveries that will be received. We believe the settlement between AGI and Fibreco will help to facilitate the finalization of other insurance-related matters.

In the past March 31, 2023 quarterly report, the following paragraph is mentioned:

Over the period of 2019–2020, AGI entered into agreements to supply 35 large hopper bins for installation by third parties on two grain storage projects. In 2020, a bin at one of the customer facilities collapsed during commissioning, and legal claims related to the incident have been initiated against AGI. As at March 31, 2023, the warranty provision for remediation costs is $40.7 million [December 31, 2022 – $41.5 million], with $0.8 million of the provision having been utilized during the period.

… there is a long history of expenses associated with this incident, from Q2-2021:

Based on remediation work completed thus far, we have recorded an additional $7.5M to the previously disclosed $70M accrual. The increase is primarily the result of additional engineering, steel, and labour costs required to ensure a satisfactory product solution as well as additional legal costs. To-date, the Company has spent approximately $25M of the accrual.

… from Q4-2021:

As at the end of December 31, 2021, the Company has spent approximately $43.4 million of the $86.1 million total accrual, which was increased by $8.6 million in the quarter to reflect an updated view of the costs to resolve the issue.

So this whole debacle will have costed AFN about $100 million in total. Needless to say, for a company the size of AFN (generating $102 million in cash flows through operations in 2022) that is a huge amount – over $5/share!

So why is the stock up? Beats me!

It is not like I did not do any due diligence on this case – I went to Vancouver Supreme Court to dredge up the civil case files to see if I could get some colour on the incident. There were some interesting documents in the stack of papers in the file folder. A professional engineer apparently was way out of his depth with the design of the grain towers and I figured the blame would get pinned on his liability insurance (and hence AFN would be able to claim their own insurance against his), and I figured that I might as well hold the shares (instead of dumping it) for the inevitable (favourable to AFN) payout. Obviously I was out of my depth on this one since it is clear that AFN completely lost the case with this settlement where they have to take an additional $15.6 million charge.

Yet, the stock is still incredibly close to its all-time highs and 2023 looks to be a record year for the company. Go figure. It’s a little disturbing that I don’t have a clue what I’m doing with this one. Just reading the financial statements, they continue to have a lot of financial leverage but management has been making noise lately about actually paying down debt which would make everybody involved more comfortable.

It continues to be a huge investment despite how out of depth I am.

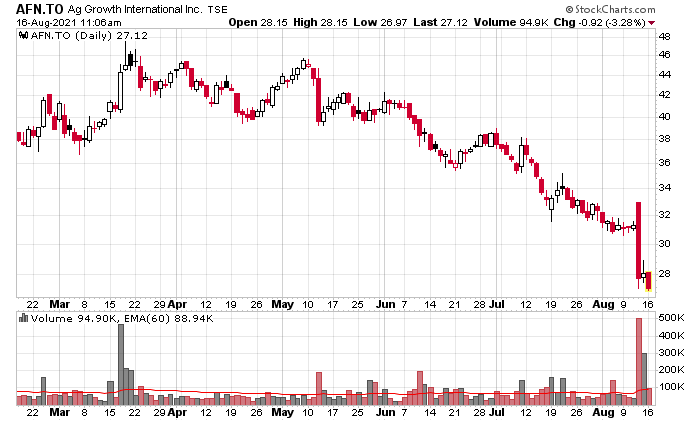

Ag Growth (TSX: AFN) used to be my largest portfolio component, but by virtue of depreciation and something else in the top 5 that has appreciated, is no longer. The company’s stock has taken a beating over the past 3 months:

The market was spooked by their Q1 (May 2021) announcement on their conference call regarding the pricing of steel (indeed, when looking at Stelco (TSX: STLC) you can see what they mean) – companies quote projects and their quotations typically remain open for 30 days, but this is like giving your customers a free one month call option on steel pricing, so they had to tighten this up. They said the high-cost backlog would cost them some margin in Q2 and Q3 but it would normalize in Q4 onwards.

In Q2, there was some margin degradation, and besides this, the quarter was reasonably decent. Sales up, gross profits up, margins slightly lower but this was to be expected. However, the killer payload was this line:

In 2021, two legal claims related to the bin collapse were initiated against the Company for a cumulative amount in excess of $190 million, one of which was received subsequent to the quarter ended June 30, 2021. The investigation into the cause of and responsibility for the collapse remains ongoing. The Company is in the process of assessing these claims and has a number of legal and contractual defenses to each claim. No further provisions have been recorded for these claims. The Company will fully and vigorously defend itself. In addition, the Company continues to believe that any financial impact will be partially offset by insurance coverage. AGI is working with insurance providers and external advisors to determine the extent of this cost offset. Insurance recoveries, if any, will be recorded when received.

I had a massive due diligence failure, especially considering one of these two events was within a car ride of where I am. Fibreco sued Ag Growth International and also the professional engineer that signed off on it, in BC Supreme Court on June 4, 2021. There was also a news article on the matter which I totally missed.

This is probably the biggest contributor to the stock getting tanked over the past quarter. $190 million is close to $10/share, but the larger impact is the balance sheet threat.

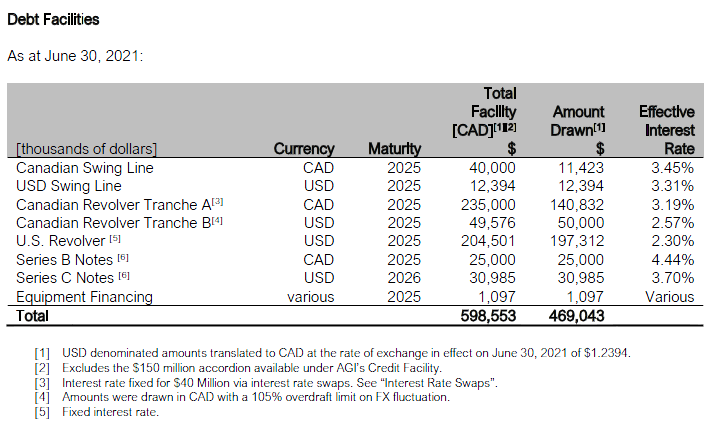

Ag Growth relies a lot on low cost debt capital to fund its operations. Given the nature of its business, their cash flows are relatively predictable and there is a seasonality with cash collections that require the usage of credit. Their debt structure is funded by unsecured debentures (AFN.DB.D, E, F, G and H) each of which is around $86 million in quantity. The unsecured debt is termed out, with D and E maturing in June and December 2022, while the rest of them are out in 2024 and 2026. They also have some tranches of first-in-line bank debt as follows:

Note that they all term out in 2025 and there is about $95 million of availability on the Canadian revolver and $29 million on the CDN swing line.

However, all-in-all, given there is a total of $900 million of debt between these two series ($430 million of unsecured, and $470 million of secured, roughly at an average weighted cost of around 3.9%), the company’s leverage position is quite extended. Tacking on another $190 million on top of that is a tall order. An increase in the cost of capital, needless to say, will be adverse for the equity holders (a 1% increase in capital cost is about 50 cents per share, pre-tax).

The risk has definitely increased due to the number of unanswered questions.

1. How much will insurance actually cover, especially in the event that AFN is found to be at-fault? What is the maximum coverage? (God forbid if the majority of it was self-insured).

2. When will these proceedings resolve themselves (typically it will be by settlement, but a trial would take a couple years to clear out undoubtedly)

3. (by far, the biggest factor of these three, in my opinion) Because AFN screwed up (whether it is their fault or not, doesn’t really matter at this point) building two grain towers, are there any other towers of like composition that are waiting to crumble down?

4. Will re-financing risk be a factor (specifically with AFN.DB.D, and E)?

Question number 3 could literally be a case of waiting for another time bomb to go off, in the form of another grain silo collapse. Another such event would tank the equity by 20% in a day. This is a sort of unknown-frequency, high severity event that elevates risk.

On the flip side, we have the following:

1. The market for AFN’s unsecured debt is still strong (trading just slightly above par at the moment across the entire term) although the whole point of doing this market analysis is to determine when the market is wrong! That said, if there is some debt distress, it isn’t being reflected in these prices;

2. The company, at least on a basis when grain towers aren’t imploding, should be able to generate around $45 million in cash this calendar year, and in a more normalized year, should be able to generate north of $100 million and de-leverage. This is…

3. … fueled by the fact that agricultural products have had their supply chains really disrupted and the demand for product should create demand for capital spending on agricultural equipment.

4. Lawsuits, especially in Canada, very frequently settle for below the “face value” on the claim.

My last comment is that there was some premium valuation in AFN on the basis of “Ag Tech”, but it appears that this bubble has popped with Farmer’s Edge (TSX: FDGE) cratering (it’s down 75% since its IPO and indeed closer to where it should be trading!). This part is healthy.

The current dividend, at 60 cents per share, or $11 million a year, is not particularly onerous to maintain, especially in the case of ‘normal’ business performance, which should be a lot higher than what they have been doing in the past.

If the overhang on the stock is purely on the basis of this lawsuit, the stock is at a price level where it is attractive. If there are more structural issues with the industry that AFN is in, then my original investment thesis was flawed. I do not believe this to be the case, but definitely the elevation of risk is reflected in the stock price. I’m not happy with this situation, nor am I happy about how it was presented in the past few quarters.

Ag Growth (TSX: AFN) sold off heavily today as a result of overall market weakness coupled with the markets not liking the fact that their costs are going to be increasing in the upcoming quarters due to the surge in steel pricing, coupled with a likely re-valuation of their technology platform. It’s not great having your top holding taking a haircut like this, but that’s how markets work – things go up and down, and this is also buffered by other things in my portfolio which take advantage of inflation.

They want me to flip my AFN shares in exchange for yet-to-be listed units in their fund, based off of the average trading price on June 1-3, at a par value of $10/unit.

I can only assume it was also offered to other securities they plan on holding in their fund (they list the prospective holdings on a one-pager, including companies such as Beyond Meat, Farmers Edge, Goodfood Market, Rogers Sugar, etc.).

I have stronger wording which I will not type in, but will state that this offer is highly unattractive for a few reasons. I’ll list a couple.

One is that right away, such an offering will involve a 4.5% payment to the agents, so effectively your $10 ‘value’ will be reduced to $9.55 immediately, plus another $500k in expenses associated with the offering (it costs legal fees to process partial tender requests such as these).

Assuming you were silly enough to go with it, the MER of the fund in question is 125bps.

I just shut off the prospectus from my computer screen before I wasted more mental space on it. But it was worthy of a post – who actually falls for these types of offers?

I don’t talk about IPOs very often, but this one caught my attention because of its presence in the agricultural space. Farmer’s Edge (TSX: FDGE) went public at an IPO price of $17/share, raising $125 million in gross proceeds ($117.5 net), and started trading on the TSX on March 3rd. Unlike many other technology IPOs, they have at a modest premium to their offering price:

There is a customary 30-day option by the underwriters to purchase more shares, which at the current market price of CAD$18.80 is likely to happen. I will assume so – the company will have 41.8 million shares outstanding if this happens.

Fairfax (TSX: FFH) owns 60% of the company after the offering and is the only 10%+ shareholder.

(Update March 8, 2021: The stock is now trading under CAD$17/share, that was quick… FFH will own 62% without the exercise of the over-allotment).

(Update March 9, 2021: Underwriters have exercised the over-allotment option – gross proceeds $143.8 million).

Company’s Operations

FDGE offers a package called FarmCommand. It is a piece of software which integrates with provided hardware (CanPlug) which facilitates a data conduit to the software relevant to measuring grain weight by location during a harvest. The software beams the information to the cloud using cellular data, and the software crunches the metrics and presents it to the end-user. Likewise, they also sell weather probes and soil moisture probes that can send data to the server (and this data can be used to make correlations at future times). Finally, they do have a soil sampling service that looks painfully manual and will test the soil for composition, using their own lab equipment. This information can be used later to suggest fertilizer solutions.

They use Google to store the data to the cloud, and Airbus to provide satellite imagery.

Revenues are obtained by selling farmers the FarmCommand package on a per-acre-per-year basis and also collecting such data to sell to crop insurance companies.

Relevant quotes:

FarmCommand is sold on a subscription basis, per acre per year, and is offered in five principal tiers. We focus on selling our $3.00 Smart package but offer price points starting at $1.50 for a basic Smart Imagery package, scaling to $6.00 for our comprehensive Smart VR package, with these list prices and packages varying marginally by geography. Our customers have historically subscribed to four-year contracts. Recently, we have introduced our Elite Grower program which allows our customers to trial our platform for free for up to one year before subscribing to a four-year contract.

…

Crop insurance partners form part of our go-to-market strategy and we expect them to sell our subscription products to their agriculture customers. Once our program is deployed on the farm by a crop insurance company, Farmers Edge will be able to provide reporting, analytics and predictive modeling to the crop insurance industry players on demand.

This reminds me of car insurance companies getting people to voluntarily put a device in their car dashboards for the purpose of insurance assessments. If you are a “safe” driver, as in you don’t drive that much and when you do, you drive at low speeds, then the insurance company will give you a discount. In reality, they will use this information to determine more accurate pricing, which is why there is a significant degree of selection bias with such offerings.

I also believe certain farm operations have proprietary methods that they would not want to disclose, which would work to the detriment of FDGE.

FDGE states they estimate at the end of Q4-2020, they have 23.4 million acres of subscribed farmland, and an estimated revenue of $45-47 million for 2020. 54% of this was Canada, 28% was USA, and 13% was Brazil, and the remaining 5% is Australia and Eastern Europe.

Keep in mind rough estimates are that Canada has 90 million acres of cropland, the USA has 250 million acres and Brazil 150 million. The total addressable market in these geographies assuming 100% penetration and the $3/acre package would be about $1.5 billion a year in revenues.

The company claims it adds value:

The ROI our solutions provide farmers vary by product and region. As additional examples, corn farms implementing our solutions earned farmers roughly $52 more per acre in Nebraska, and $36 more per acre in Kansas, compared to state averages, in 2019.

Clearly if this is the case and if they can establish this with better studies and have a proprietary advantage with their software to make it happen, then one can presume they can capture more margin than $3/acre.

In terms of competition, they list John Deere (NYSE: DE) and Bayer-Monsanto (OTC: BAYZF), but they allude to a “Point and regional solution providers” which is clearly referring to Ag Growth (TSX: AFN), but they are never named quite likely for the reason that they are the true competition.

Finances

The company has lost a lot of money over the past 3 full fiscal years. The “finance costs” is somewhat misleading as the company has been financed with debt before the IPO and this was equitized for the IPO.

In terms of raw EBITDA, and the accumulated non-capital loss for tax purposes (which is a rough proxy for true expense), we have:

2017: $53.8 million loss / $130 million

2018: $76.4 million loss / $199 million

2019: $74.2 million loss / $309 million

9 months in 2020: $42.4 million loss (annualized, $56.5 million) / tax NOLs not disclosed yet

This is also ignoring capital costs, which are not inconsiderable as the company has to get the hardware into the farmers’ hands (in addition to the installation) in order to do the data collection.

The company gave projections for 2020 and is expected to have burnt $52-56 million. Because of the renegotiation of the Google contract and the satellite imagery contract (which has been re-contracted to a subsidiary of Airbus), they are expected to save an annualized $15 million in costs (makes you wonder how they managed to negotiate the deals in the first place – this was not an inconsiderable cost savings).

The company has been mostly funded by Fairfax during inception. There are a couple other under-10% holders, one of which (Osmington Inc.) has the right to a board seat as long as they maintain at least 5% ownership.

After the IPO they will have converted all of their debt into equity, and have a pro-forma $106 million of cash on the balance sheet as of September 30, 2020 and the only significant debt being $6.5 million in future lease obligations.

They claim “break-even for Free Cash Flow in the medium term, assuming growth in Subscribed Acres remains consistent with the above expectations” (45-50% annually). Of course you will if you grow high-margin revenues at that rate! While achieving that percentage growth is indeed possible, the question remains whether they can do it profitably (it is difficult to make money giving out 1-year free trials and not cashing them into 4-year contracts), and the terminal growth rate of the business (it will not be 45-50% annually for a very long time, especially given the acreage penetration they have already achieved).

I’m not going to comment on the management suite or the board of directors, but I have reviewed them.

Some analysis on the software

There’s a lot of interesting information on how to use their product online. For instance here is one particular function within their FarmCommand software, but also as part of a series of instructional videos:

This competes with AGI’s Suretrack Compass software:

I’m finding this comparison between the two softwares to be interesting. AGI’s solutions are obviously vertically integrated with some of their products (their grain silos), while FDGE’s solutions are a horizontal turnkey solution. There is a lot of overlap. I would suspect that part of the reason why FDGE has spent a ridiculously large amount of money to date is to just get farmers aware of the software – they don’t have any inroads to the end-customers that a company like AFN or John Deere would have.

The other observation is that these Youtube videos that I linked to have views that are measured in the low hundreds. Almost nobody has watched these videos. There appears to be zero public awareness of agricultural software. If at some point these companies receive more eyeballs (heaven forbid if /r/WallStreetBets decided to hit it), there aren’t a lot of public companies in this space that would receive instant elevation to their valuations.

Consider that the weekend market capitalization for FDGE is $765 million – higher than Ag Growth’s $715 million (albeit, Ag Growth has a considerable amount of debt on their balance sheet, about $870 million), it makes one wonder how to reconcile the valuation differential. Is this attributed to FDGE as being some sort of “pure SaaS play in the Ag Space”, while Ag Growth is a much larger conglomerate (set to exceed a billion dollars in revenues), primarily concerned with the (relatively more boring) design and construction of grain towers and movers rather than having their own piece of software, which by all accounts does mostly what FDGE does?

I’m not interested in FDGE at current valuations, but I’ll watch it. If it turns out the current valuation of FDGE is “correct”, Ag Growth is incredibly undervalued.

Disclosure – I presently own shares in Ag Growth (posted here).

My thesis in Ag Growth International (TSX: AFN) was written in a very condensed form back in “we are all going to die of COVID” April, which seems like an eternity ago.

After reviewing AFN’s quarterly report, business is even better than I was thinking post-COVID. The stock price is now a closer reflection to where it will be going, i.e. still higher.

In fact, if I didn’t already have as high a position in this stock as I did (I took a fairly large position in early April and that has ballooned due to appreciation), I would be buying more.

Nearly nobody in retail-land follows this stock – the lack of commentary on places like Seeking Alpha or Stockhouse is comforting. I don’t see people on Robinhood flipping this stock around. Even after reporting what is unarguably a good quarterly report, the stock only traded a shade under 200k shares.

There are some related companies with somewhat less in the way of competitive advantages that are trading relatively cheaply as well, but business-wise AFN is in the sweet spot. I managed to get shares of one of these other related companies, but it was a ridiculously small position before their stock took off as well.