Why people would be long-term investors in this company’s common shares is beyond me. It is, however, a good speculation vehicle on government bailouts, of which I cashed in on about four years ago when the Liberals took control of government.

Bombardier common shares (TSX: BBD.B) are trading down 32% today on the news their quarterly results are not going to be as good as expected. In fact, this is somewhat of an understatement as they just threw everything bad into the release. Transportation is performing very badly, and a couple key quotations:

Consolidated free cash flow for the fourth quarter is estimated at approximately $1.0 billion, approximately $650 million lower than anticipated.

Oops.

While the A220 program continues to win in the marketplace and demonstrate its value to airlines, the latest indications of the financial plan from ACLP calls for additional cash investments to support production ramp-up, pushes out the break-even timeline, and generates a lower return over the life of the program. This may significantly impact the joint venture value. Bombardier will disclose the amount of any write-down when we complete our analysis and report our final fourth quarter and 2019 financial results.

The “call option” embedded in Bombardier’s disposal of its participation in the C-Series aircraft is increasingly looking like to come to a (metaphorical, not literal) zero. The agreement with Airbus required cash injections up to a ceiling and it looks like this threshold will be reached. While the minority stake Bombardier has will still have some value (especially as Airbus eventually gets around to selling the aircraft, which by all accounts, are superior) it isn’t anything like what they anticipated a decade ago when getting into the market, which is a real shame.

And on the issue of their capital structure (which is getting quite debt-heavy in relation to their cash flows):

The final step in our turnaround is to de-lever and solve our capital structure. We are actively pursuing alternatives that would allow us to accelerate our debt paydown.

Easier said than done. With their market cap under CAD$3 billion, any de-leveraging through common share issuances are going to be highly dilutive and not make too much of a dent on their US$9.3 billion debt (as of September 30, 2019). They are pursing asset sales to inject a billion into the balance sheet, but Bombardier is clearly running out of options. They’ve gotten rid of their commercial aircraft division, and 30% of their transportation division, so there isn’t much left. “solve our capital structure” is a code-word for a “light recapitalization”, which would explain the common stock tanking today.

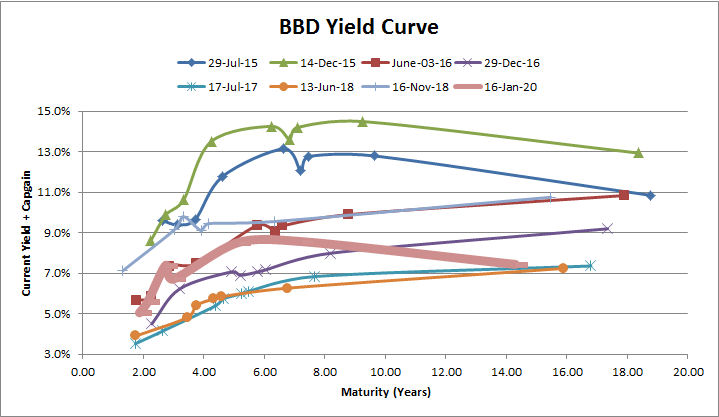

It has been awhile since I reviewed Bombardier’s debt maturity curve and I’ll show a snapshot of my trading console and also a yield-to-maturity graph that I have been keeping of the company. The thick line is the present yield to maturity of their debt and despite today’s news, doesn’t appear to be too catastrophic (yet):

Bombardier can still likely raise debt financing, albeit more expensive today than it was yesterday (when most of their bond issues were trading at above par).

The preferred shares (TSX: BBD.PR.B, BBD.PR.D) also took a dive, and are now trading at around an 11% yield for those that like to gamble. Just be warned that “alternatives to allow accelerating our debt paydown” might include the suspension of preferred share dividends (suffice to say, this would likely result in lower prices for the preferred shares). An interesting gamble for yield chasers!