I posted about it the oil situation earlier, and here are some ramifications: Interactive Brokers took a $88 million hit on client margin accounts on oil futures:

Several Interactive Brokers LLC (“IBLLC”) customers held long positions in these CME and ICE Europe contracts, and as a result they incurred losses in excess of the equity in their accounts. IBLLC has fulfilled the firm’s required variation margin settlements with the respective clearinghouses on behalf of its customers. As a result, the Company has recognized an aggregate provisionary loss of approximately $88 million.

Other financial institutions and/or funds were probably cleaned out on this transaction as well.

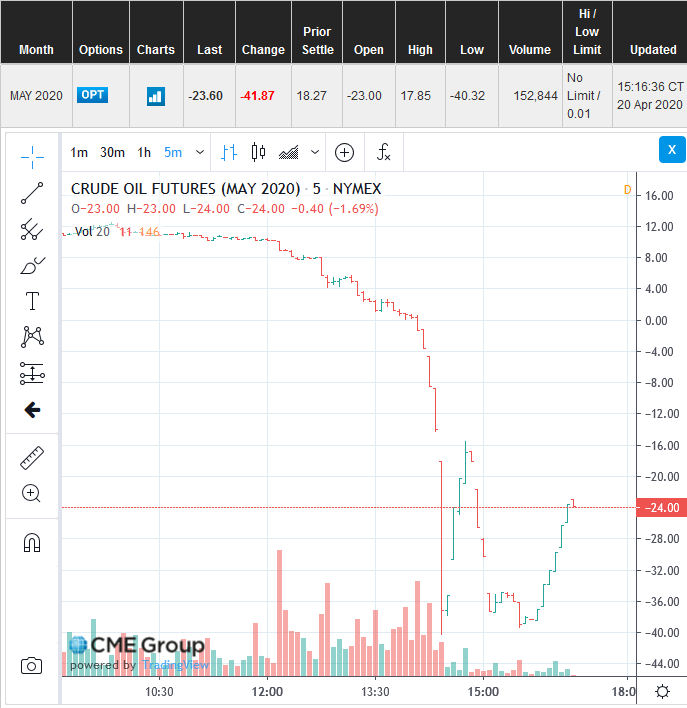

Anybody investing in the USO ETF (US Oil) is actually investing in a combination of the two front month futures contracts (retail is crazy to use this ETF as an oil instrument – if they really feel like ‘safely’ speculating on oil, better to put some money in XOM, COP, or if they insist on Canada, SU or CNQ). At the time of the May 2020 contract calamity, USO had zero exposure (they already rolled over to June), but today there was visibly obvious trading action on the charts that are classic liquidation trade signs:

Whenever you see “V” type charts, especially sharp ones that you see here, this is most likely due to a function of margin trading and customers getting cleared out en-masse – a cascade of market sell orders in the accounts with insufficient equity. Conversely if you’re bright enough to put some layered orders on the buy side (and have sufficient fortitude to not catch the absolute bottom since you have no idea when the forced selling will end) you can make huge profits in a very short period of time.

Needless to say the negative oil prices on the May 2020 contract (coupled with some rumours of Supreme Leader Kim) has increased the perception of market volatility and risk, and I have been nimble enough to reduce risk and get out of the way of any potential blowups of this magnitude. The net result of this is that a whole bunch of oil producers are going to go belly up and this will drastically reduce the supply going forward, probably at a higher rate than the decrease in demand exhibited to date.

Now my next question is: Are banks the next to drop? They are ultimately backstopped by central banks, but I deeply suspect they are in more trouble than it may seem. People looking for “safe dividends” in Canadian financial banks should be very, very cautious right now. It’s very difficult to predict how much of their lending will go belly up.