I will make a claim that companies that make “stuff in demand” will do reasonably OK in an inflationary environment, providing that they can actually price their contracts properly in anticipation of such inflation. The key operationally is that they need to be able to ensure their physical inputs, but also be able to retain their expertise and know-how in the staff – one of the huge competitive disadvantages that most Canadian cities have is that most people that actually do the work can’t afford to live at the wages being offered.

Part of my examination of industries producing “stuff in demand” involved a re-examination of New Flyer Industries (now rebranded NFI with the same TSX ticker symbol) and I have been eyeballing this one for many, many years. I’ve never owned it. They are one of the top (if not the top) manufacturer of busses in North America. Financially speaking, however, they have not been doing very well over the past few years. While one can claim that Covid-19 was an absolute killer for public transportation, the historical income statements show a huge varying history of income generation – with the peak being in 2017 (the stock was trading over $40 at this time and peaked around $50 in 2018). Just before Covid, however, the 2019 year reported net income, but the cash flow statement shows a company with working capital management issues, coupled with spending $327 million on an acquisition. 2019 ended with negative tangible equity of about $430 million and $1.2 billion in debt. NFI was sliding before Covid hit.

Post-Covid, they have really struggled to stay afloat, especially with their bank covenants.

On July 29, 2022, NFI renegotiated their debt covenants. Part of the new covenants was that they would earn a minimum adjusted EBITDA of $45 million after the 4th quarter. A few months later, they subsequently projected a NEGATIVE 40 to 60 million. It was less than three months since they re-negotiated their debt covenants and blew it, and not by a small amount either – they missed by a mile. The dividend was also cut to zero at this point (it should have never been paid out in the first place given their balance sheet situations).

Nearly half a year after that, they announced they were receiving short-term government bailout money from Export Development Canada (a Canadian crown operation) and the Government of Manitoba.

Much to my surprise on May 2023, they announced they reached an agreement with their creditors to raise equity financing, and also additional secured financing. Later that month they also issued more equity – both equity raises were deeply under the market price of NFI traded shares (CAD$8.25/share). The primary equity investor, Coliseum Capital Management, raised its effective stake in the company from 12% to 27%.

On July 25, 2023, they indicated that a $200 million tranche of Second Lien Debt includes “an annual coupon at the higher end of the previously disclosed expected range of 12% to 15%, payable semi-annually, with a maturity of 5 years.”. Today (August 16) when they announced their quarterly result, they raised another $50 million gross (5 million shares at $10.10/share, about a 15% discount to market) with a reduction in the Second Lien Debt to $180 million.

The August release stated “Based on the expected proceeds from the August Private Placement, NFI intends to lower the gross proceeds from its proposed second lien debt financing from $200 million to approximately $180 million. This is expected to generate annual interest savings of up to $2.9 million per annum.”

Pulling out my calculator, $2.9 million divided by $20 million gives an interest rate of 14.5%.

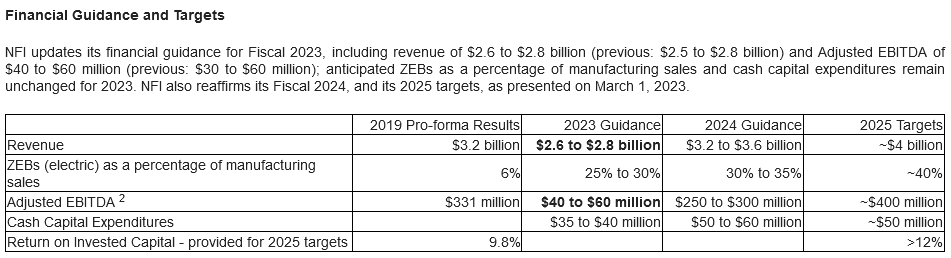

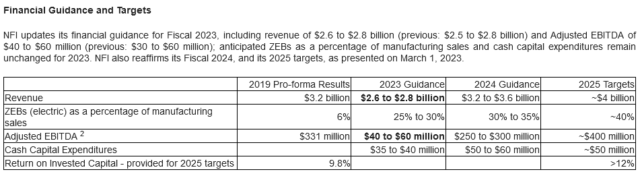

NFI also claimed the following in their release:

I am not sure how credible this guidance is, but going from $50 to $275 million in EBITDA in a year is quite a leap. Operationally, this company is effectively producing larger pure electric vehicles and should this not result in a Ford or GM-type valuation?

The big surprise to me, however, is how or why the stock is holding up so well despite this huge financial mess that has been going on over the past few years. Despite having nearly a billion dollars of debt further ahead in rank, the most junior tranche of debt, the 5% convertible debentures maturing January 2027 (TSX: NFI.DB) trade at around 82 cents, a 12% yield to maturity. The second quarter report had a negative $40 million free cash flow. All of this suggests that the equity is priced for absolute perfection. It is no wonder why the company is so eager to issue shares, even at a steep discount to market.